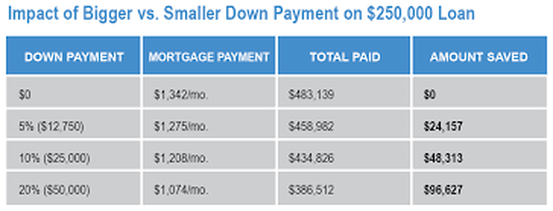

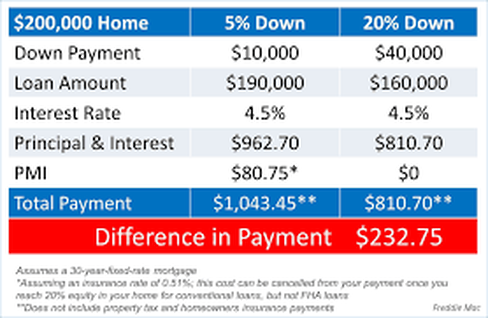

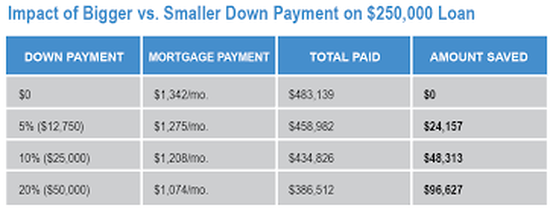

Someone I know recently bought a house and my 24-year-old son was asking me about the details. His number one question being “How do people save up that much for a down payment?” As I answered his questions it got me to thinking that I never addressed this topic in these blogs, so here goes:  How do you know when you are ready to buy a house? Well some people think it’s just a matter of saving up that down payment, but really a lot more preparedness needs to go into it. First of all, how settled are you? Many young people move around quite a lot for job changes or other purposes so even if they are very lucky enough to have that down payment at such a young age, it is not necessarily the best time to be putting down roots into home ownership just yet.   Unless you are sure that you will be staying put for at least the next five years, buying a house is rarely a smart move financially. You will sink a lot of money into the act of buying the house (in closing costs, realtors fees, inspections, lawyer’s fees, etc.)  Then once you buy there is the cost of moving in, and often on top of that people will do some work to the house to make it more to their liking. And there is even the inevitable furnishing and decorating, especially if you are starting from “scratch” with nothing.  And if you have put down a small down payment, you will typically not be gaining much equity in the house for the first few years, at least, as most of these initial payments are going to the interest on the mortgage. It is not until the principle starts to go down a little that the mortgage payments will start to chip away at that principle. And of course it also depends on the housing market. Your house could go up in value, giving you more equity but there is also the possibility that it could go down in value and put you in a situation of being “upside down” on your mortgage. That is actually owing more on it than the house is worth. This is what happened to all those people when the housing bubble burst in 2008.   So with all that said, it will take a while before you will get enough principle back when you sell to offset the costs you put in when buying it. If you sell too soon you will not only not gain any money on the sale you could very well come out in the negative for your years of home ownership. If this is the case you would have actually have been better off to continue renting and saving your money. Next, other than that down payment you have saved up, how is your financial situation? Do you have any debts? If you do, it is very smart to pay them off before embarking on your homeownership journey. Do you have an emergency fund (of three to six month’s expenses) saved aside? I would recommend at least six month’s during this transition into home ownership as you never know what can happen. Is your job secure? You don’t want to take on all this extra monthly expense only to be caught high and dry with a loss of income. This type of scenario sends people scrambling and can result in a disastrous situation.  Even if your job is secure, you have a good down payment saved up and you know you will be staying put, have you crunched the numbers to see of you can afford the cost of homeownership? A common mistake people make is this line of thinking. “I am paying X (say $1,500 per month) on my rent so I might as well be paying that amount on a mortgage and actually owning my own home.” The trouble with that is that you must consider all the other costs of owning. Some things that were covered by your landlord before are now your responsibility. Have you thought about taxes, homeowners insurance, (PMI if you have a small down payment), electricity, heat, TV, internet, water, rubbish removal, etc.?  And in addition to all those fixed expenses, if the house is yours, you are now responsible for the upkeep. And no matter what great shape that house was in when you bought it, something always needs attention. Sometimes it seems barely a month goes by without an unexpected household expense. Even non-household expenses can derail you if you are “living on the edge”, just making all your monthly bills without a penny to spare. This is why it is so important to have that emergency fund set up before you move in.  Now what about that down payment? I just mentioned PMI in the previous paragraph. What is that that? If you put less than a 20% down payment then you have to pay Private Mortgage Insurance. And although you are responsible for these premiums this insurance does nothing to protect you. It is to protect the bank from losing the money they lent you should you default on your payments.    So, this brings us to my son’s question. How much of a down payment should you put down and how do you save up that kind of money? The answer to the first question is as much as possible, at the very least 20% (to avoid that PMI) If it’s home ownership you are after (and not living in a bank-owned house that you are paying dearly for (in interest payments) you should set your sights on the biggest chunk of money you can plop down.  Another way to keep your down payment at a higher percentage of the cost of the house is to buy a less expensive house. This way that same down payment you have saved is now a larger percent of the total cost. You can always move into bigger house (or expand the one you are in) down the line should the need arise and your finances improve. Here’s a dirty little secret the banks don’t want you to know. They will approve you of a mortgage that is really out of a comfortable price range for you. Why? Because they are really not interested in how comfortable you are making the payments. They are just looking to get the biggest mortgage for themselves (the more you borrow, the more interest payments they will get). So buy a house that you are comfortable with (monthly payment wise), not what the bank approves you for, and ideally this monthly payment should be no more that ¼ of your monthly income. And one more thing on the subject of mortgages. The bank will automatically default to a 30-year-mortgage, but you are much better off to get a 15-year. The quicker you can get that house paid off, the less total interest you will pay on it. You can save yourself many thousands of dollars (even hundreds of thousands) by just doing this one thing.  Now to Jesse’s question of how to save up for that mortgage. The same way I recommend you save up for anything else. Make it automatic! Open up an online account and set up automatic monthly payments going into it. Take the total amount you want to save and divide it by the months until you want to have the money. If you want to save up a $75,000 down payment in four years that would mean you need to save about $1,500 per month. *See Easy Peasy Make it Automatic  If your timeline for savings is actually more than five years then you might want to consider investing (all or part of) the money into a low cost (relatively safe) mutual fund (such as an S&P 500). Putting those payments away each month will also help you to be living below your income and able to make all those extra expenses when you do move into that house. Owning your own home is the American Dream. It is a great feeling to live in a house of your very own and can also be a real plus to your total financial picture if you are indeed prepared for it, but please make sure you are fully ready before taking the plunge or it has the potential for turning into a nightmare. Do it right and make it your dream come true!  Best of luck to you if you are looking to embark on this exciting new chapter of your story. Wishing you a bright future in your own home sweet home!

0 Comments

|

Archives

June 2022

Categories

All

|

RSS Feed

RSS Feed