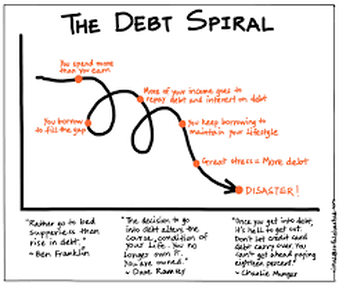

There is a law of physics that you’ve all heard of that states that an object in motion tends to stay in motion. Well, I’ve observed that it is the same with most people’s finances. Once people get going in a certain direction with their money, they tend to remain on it until something happens to change it.   This motion can be in either direction. Once people begin to live beyond their means and start to accumulate debt, that downward spiral into debt begins to snowball, making it very difficult to get off the ride. But the good news is that, conversely, if people can start to move the needle in the opposite direction and start to save money instead of accumulating debt, this too can have a snowball effect and the more you save, well, the more you save! Being in debt becomes a perpetuating cycle for the very reason that you are in debt. When all your money is going towards your credit card and other debt payments, there is never any money to use whenever something comes up. And this too goes on the card. You can see (or maybe know firsthand) how this could go on and on. On the other hand, if you have money saved, you not only easily pay for any financial emergency or need that comes your way, and avoid paying interest payments, but you can also take advantage of strategies that can grow your money even further.  The most obvious of these opportunities would be the ability to invest your money. Now instead of paying out interest you have the ability to turn it around and have that interest work for you. And thus the snowball grows (in a good direction!)  When you have a cushion of money beneath you, you no longer have to approach life from a position of desperation. Desperate people need to resort to desperate measures to keep themselves afloat. Think of those insidious payday loans, with their ungodly interest rates.  Desperate people do not have the money to maintain their possessions (I.e., cars, appliances, roof, etc.) or even their health, and often end up paying much more in the long run for car repairs, home repairs, or even worse, a health crisis because they were unable to keep up with the maintenance required.  Of course, the key is to turn this trajectory around to be moving in a positive direction. The hard part is the turning. It does take a lot of work and sacrifice to get a debt situation under control. But once you push through and make it to the other side the rewards are immense. Now you can relax and let that money work for you. The very interest you were fighting now becomes your friend. It’s a great feeling.  I hope I can inspire you to begin to move your needle in the right direction. I will be here cheering you on the whole way! If you need any specific strategies to help get you going, take a look through some of my other blogs for some tips and tricks that might work for you. If you need more personal help, feel free to contact me for a one-on-one appointment.  Wishing you all the best in snowballing your way to a better and brighter future!

0 Comments

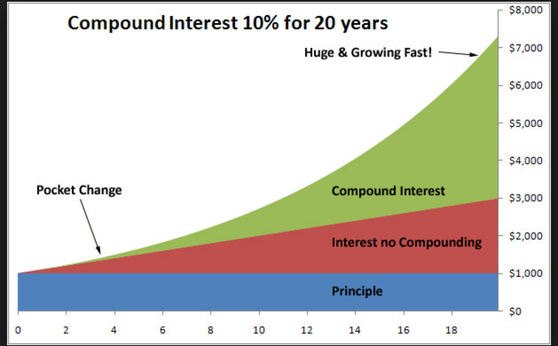

Many people tend to view the holidays as a time of abundance and exuberant gift giving. They equate the season with bountiful shopping and lavish piles of gifts. And while I understand the spirit of generosity and kindness that this custom represents and originates from I can’t help but feel that it has lost something through the years as it has been taken to the extreme.  Of course, being the frugalista that I am, I first must note that, for one thing, it “inspires” (forces?) people to spend beyond their means. So many people today are going into debt for the sake of (the societal pressure to create) a lavish holiday. Do you regret the bills in your mailbox come January? Are you able to pay them off? You can read more in my December 2018 blog about how to have a festive holiday without the debt hangover.  But it goes even beyond the new year regrets. How does this excessive holiday feel to you? Most people report feeling frazzled and stressed out and overwhelmed trying to pull it off. So then, what is the point of it all? Is it for the children? Well, I can tell you right now that children’s happiness not only is not dependent on how many gifts they receive, but is, in fact, negatively impacted by over abundance. They are actually more appreciative of a few well thought-out gifts than a mountain of “stuff." And what message are you sending them with all this “generosity?" Does the word “spoiled” have any meaning to you?   So, if you are currently wrung out by all the stress and overindulgence of the past month, and you are dreading facing those bills in the mailbox come January, it may be time to consider another way next year. Just try it. I think you will be pleasantly surprised.    Wishing you all joy, peace, and contentment at the holidays and always   Perhaps you have heard there is currently an epidemic of people in our country crippled under outrageous student loan debt. Some people are heading into retirement and still struggling to pay off their college loans. This is completely unnecessary. Don't end up like this!  I recently gave a talk at the local community center about the smart way to go about planning with your kids for their college so that they can get a degree with as little as possible, or better yet, no debt, and I realized that this is a subject that I have yet to address in this blog space. I would like to start off by saying that all four of my children have college degrees, one with a PhD, and not one of them has ever taken out a college loan. I don’t say this to brag, but rather to illustrate my point that it can be done and it’s not even that difficult to do. But you have to have the right mindset. And my kids did not even all follow the same “formula” to achieve this, but each found their own way to achieve their degree with no loans bogging them down at graduation time. When I say the right mindset, I mean to go into the college years with a clearheaded view of the objective, which is to obtain a college degree that will help launch you into a decent paying career. Some people have taken to making too big a deal about the “college experience” and to this I say it is only four years out of a young person’s life and not worth going into crushing debt for many years to come for some perfect college adventure or “high end” degree. You can pay a reasonable price for that degree and still have a good experience and some good times and you will have the rest of your life for adventures as well. So here are some things to consider when planning for those college years that can help in obtaining that debt-free degree:  #1. Keep the scales balanced – Be realistic in your approach to college. Do not go deeply into debt for a degree that will not lead to a lucrative career. Remember you are paying for a service. Keep your R.O.I. (Return On Investment) in mind. Make it your objective to avoid debt if at all possible #2. Getting ready for college - Get good grades - Earn college credits. Take AP courses and/or college courses at a reciprocal college during your high school years if your school offers them. - Get involved, follow a passion (do not just do a “checklist” of things to beef up your resume) - Give to your community in a meaningful way in line with your own interests and ideals. - Start looking for scholarships in sophomore year. Start applying in junior and senior year. - Look at both local scholarships and online scholarships.  #3. College Choice: - Be realistic. Go where you can afford! - Community college for the first two years - State schools - Only go to a private school if you get a very good scholarship (to bring it down to at or below state school tuition). Make sure that scholarship is guaranteed for the entire two or four years. - Do not get caught up in the prestige of a college name. After your first job or two it’s not really going to matter anymore where you attended college. It’s your job performance that will stand for itself. #4. Choose a practical major: - Do some research as to your options - What kind of jobs are available in that field? - What kind of salary can you expect to make? #5. Scholarships: - Apply to as many as possible - Use these websites to find online scholarships: Fastweb, or Niche.com. There are many more. - Ask the individual colleges about them. One of my sons applied for a scholarship that the young tour guide happened to mention on a college visit and won a four year full scholarship to that school! - Fill out the FASFA (some scholarships are tied to it) - Keep applying for scholarships even when you are in college  #6. Work! - While in high school - Over summers - While in college - Be entrepreneurial! Rather than work an hourly wage job (such as a cashier or flipping burgers) work for yourself. Even things like babysitting, dog walking, mowing lawns, or tutoring, tend to be more lucrative. If you have a special talent, use it. Give music lessons, make something to sell, help people with their websites. These types of jobs often pay more than the hourly wage jobs. - Be an RA after your freshman year ,#7. Housing: - Live at home if possible. One of my kids lived at home and commuted to two years of community college and then another two years at a local state school, all the while working at a grocery store and paid off the tuition as he went along. - Take all expenses into account if considering off-campus living (utilities, food shopping, transportation, etc..) - As for transportation, seriously consider not having a car through the college years, especially if you are going away to college. Most colleges have a decent mass transit system to get around the area. None of my kids that went away to college had their own car during those years and they got by just fine. - Embrace minimalism! Do not go crazy shopping for college housing “stuff”. If you look like this heading off to college, you spent too much:  #8. Food: - Meal plan-vs-grocery shopping? Carefully consider which would work the best for you and be the least expensive option. - If you take the meal plan, use it! Don’t pay for food not eaten. Every meal you paid for but did not eat is wasted money! - Limit eating out and take-out. - Cook your own food Brew your own coffee Drink water (get a reusable water bottle)  #9. Books - Do not buy college text books at full price. Use websites like “Chegg” and “Bookfinder” to buy used books or rent them. You can also download them (sometimes for free) on sites like the Google ebookstore. You can double your savings by sharing them with a friend taking the same class. #10. Graduate on time! - Do not take extra semesters to graduate, paying more for your degree than necessary. This is especially important If you are taking out any loans for your education. - In fact, try to graduate a year, or at least a semester early if you can. This is especially feasible if you have transferred college credits (i.e. AP courses) from high school.  Have a Bright (debt-free) Future!   Having spoken with a few millennials lately, including one young lady who was very motivated to get started on the right financial footing, (this is not always the case with the young people I encounter), I thought I’d devote this blog entry to those just starting out on their lives’ journey. This is the stuff that I wish somebody had told me when I was just starting out. I figured it out along the way, but it would have been nice to know it all from the beginning. And some people, unfortunately, just never do figure it out for themselves. Would I have listened? Who knows? But, as they say, if I knew then what I know now, and followed the advice I am about to impart to you, I would very easily be a multi-millionaire by now. And you can be too. Anyone can do it.  Often I find myself very frustrated that young adults, who have the most to gain from learning to be smart with their finances, can be the most resistant to hearing (and following) it. And the sad thing is that if they don’t do it now, although they can still do alright whenever they decide to start, they can never make up for that lost time and the money they could have made by investing early. The magic of all those years of compound interest can never be regained.   So, without further ado, in a nutshell, here are my most salient tips for millennials: #1. The golden rule of finance: Always, Always, Always Live Below Your Means! Start out that way and get used to it. As your income increases you can increase your lifestyle, but always stay below what you are making. 15% of your income should going into your retirement fund at all times.  #2. The other golden rule of finance: Pay Yourself First! You will be paying out a lot of your hard earned money to other people and businesses in your lifetime (your landlord, the mortgage bank, electric company, insurance companies, gas company, food producers, goods manufacturers, health care providers, etc., etc., etc.,…..), but don’t give all your money away to other people or you will have nothing to show for it. Always be keeping something for yourself… up front, before any of your money goes out to anyone else.  #3. Make it Automatic Set up that money to go into your retirement account (401k or Roth IRA) and your other savings (goal) accounts straight out of every paycheck before you even see the money. Out of sight, out of mind.  #4. Keep track of your expenses Set up a system so that you know exactly how much you are spending, every day, every month, every year, and on what. You can do this by hand (simply writing it down) by computer (i.e. your own spread sheet) or with a website (such as mint.com)  #5 Prioritize your budget: Spend your money on what is most important to YOU First comes dire needs, housing, food, transportation, etc. Then prioritize the rest according to your income and needs. Wants come last, and only if you can afford them. Think carefully about wants-vs-needs. Do you really want to sabotage your future goals for some frivolous indulgences today?  #6 Plan for your goals Write them down and save for them systematically (how much do you need to save and when do you want it?). Do you want to get an education? Plan a wedding? Buy a house? Buy a car? Go on a vacation? Always be saving for your future purchases so that you will… (see #7)  #7 Never borrow money! (AKA buy things on credit) Don’t get into the interest paying trap. It is a slippery slope once you start on the debt quagmire. This includes education (student loans), cars (car loans), and those insidious credit cards. Always save up and pay for things in cash. If you don’t have the money, you can’t afford it. The only possible exception to this is buying a house. But even here, if you can manage to save up and pay cash that would be awesome. People do it. I did it for my second house (after I paid the first off by ten years). Certainly aim to put down as large a down-payment as you can and take out a 15-year mortgage. Then (pre)pay that down as quickly as possible. And don’t buy a more expensive house than you can afford. Though the lending banks will pre-approve you for a much bigger mortgage than you can comfortably afford, don't fall for it.  It’s really as easy as following these 7 very simple rules and you will be set for life. It’s not rocket science. Anyone can do it, at any income level. Stick with this lifestyle and you will go from millennial to millionaire, a very bright future indeed!  Which one are you? Hopefully in the green!  You can do it!!

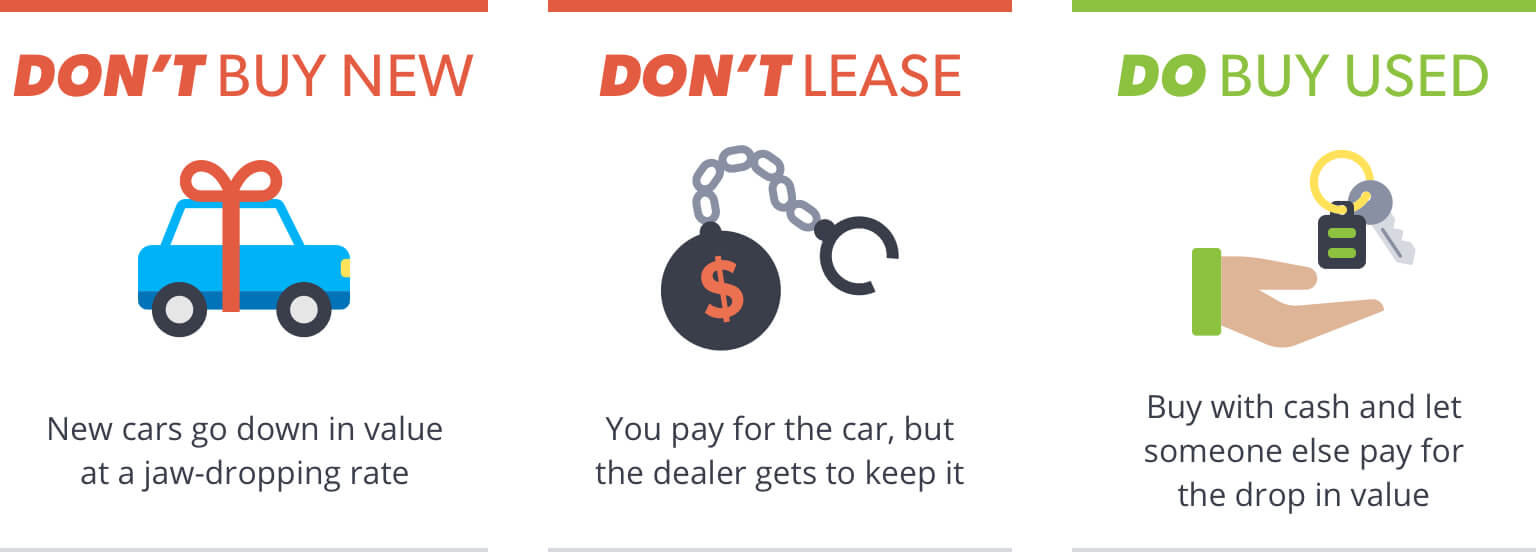

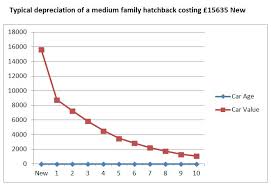

Since I am currently in the market for a “new” car, I thought I would share with you how I do not nor have I ever had a car loan. It’s quite simple if you start from the beginning but wherever you are in your auto ownership journey you can start at this moment and work your way up and out of car loans for good.  What’s wrong with car loans you say… isn’t financing a car the “American way"? Who doesn’t have a car loan? Well I don’t, for one, and I would wager a guess that every “Millionaire Next Door” doesn’t either. And yes, you’re right it has become the “American way” but which Americans are benefiting from that? Hint: It’s not you, the proud recipient of the car loan. It is the almighty bank (or sometimes the car dealerships) that are winning in this drive-now, pay-later arrangement. And the amazing thing is that they have you hoodwinked into believing that they are doing you a favor by getting you into the best car they can for low money down and easy monthly payments. Wow! What a nice guy… NOT! Believe me, car dealers are not in the business of doing you a favor. The only thing they are interested in is their own bottom line. The biggest best car they can sell you lines their own pockets, and getting you to take a loan from them (instead of the bank) is just more icing on the cake. And if you have ever been car shopping lately you will notice that they (subtly or maybe not so subtly) will start touting the glories of leasing a car. This is like taking a car loan on steroids (for them). Think about it. You pay a down payment (maybe $1,000) and then “easy” monthly payments of $299/month, and at the end of the three-year lease you are out $11,764 and you own absolutely nothing! You can now either give the car back and start all over again or pay some exorbitant fee (on top of the almost $12,000 you’ve already paid) to now own the car. You could have bought a (used) car for $11,764 three years ago and still had plenty of life left to it for years to come. And if you financed your car, let’s look at one example of how much you are actually paying for that car by the end of the loan period: If you take out a loan for $25,000 at 4.5% for a 60-month term, your monthly payments will be $570 and at the end of the term you would have paid out $27,364. A total of $2,364 lining the pockets of whoever held your loan. Nice! … For them. How do you feel about giving them all that “free” money? Would you like an extra two thousand in your bank account? But, you tell me, “I don’t have the money to just purchase a car outright.” Well, I can tell you that on a modest income I have never taken out a car loan to buy a car. How did I do it? Well, I bought my very first car for cash and from that point forward I was saving the money (that most people are paying out for car loans) to purchase my next car for cash. Most of the cars were used, at least a few years old, but I did make the mistake of purchasing two of them brand new (all for cash). No loans. If you can afford car payments you can afford to save up for a car!  Now I have instructed my kids to follow my principles. They each saved up for their first car (with a little help from me at times) and bought them (used) for cash. Then I told them to pretend (like many of their peers) that they have car payments, but pay them to themselves. And now through the magic of online bank accounts it was easy for them to set up a “car account” with $200 or $300 a month being automatically deposited into it from their checking account. And with that very modest “car payment,” if they take good care of the cars they have, in 10 years-time they will have between $24,000 and $36,000 towards the (cash) purchase of their next car. And even more than that, really, because instead of paying interest to a car loan, they are making interest on their bank account. It may be only 2% at the moment, but it sure beats paying out at 4% or more! But if you haven’t done that from the beginning and you are currently saddled with a car loan, then the best thing you can do is keep the car after your loan is up for as long as you can, and here’s the important thing: Keep paying those monthly car payments but pay them to yourself so that when you are ready for your next car you will have a chunk of change sitting there for your purchase.  And why do I say I made the “mistake” of buying a few of my cars brand new? Because the depreciation curve is enormous in the first year or two of car ownership and the bulk of that depreciation takes place in the first 5 minutes of car ownership. The minute you drive that sparkly new car off the lot you have dropped a couple of thou off its resale value. Ouch!! Let someone else take that depreciation (thanks first car owner!). Save yourself a couple of thousand dollars and buy a car that’s at least a year or two old.  So, now I will head out to the dealerships. You can buy a car from an individual for less money, but I like the assurance of having the dealer in case something goes wonky with the car a short time after I buy it. And even though I am paying cash I will still keep in mind that (friendly as they are) the dealer is not my friend. I will do my homework and check out any cars I am considering online, for any issues and the prevailing price for that year’s model. You can try Kelly Blue Book or Edmunds for this info. Then I am prepared to bargain (with the mysterious “manager” in the back, that my dealer will be consulting). I may walk away from the deal two or three times before I am satisfied that I am getting a rock bottom price. Of course the dealer has to make some money on the deal. I don’t begrudge him that. I just want to feel that I got a fair deal. Wish me luck as I head out in search of my next set of wheels and I hope you too will someday enjoy the joys of owning your own set of wheels without those pesky loans dragging you down.   This is the priority based budget. And it is a great tool to use to help you realize just what your priorities are and exactly where you want your money to go (and, maybe even more importantly, not to go). I could look at where your money is going and give you an idea of where you might be able to trim the fat and the things that I would not “waste” my money on, but at the end of the day it is your money to choose to spend as you will. Of course if you are looking to save money you cannot “choose” to keep spending on all the things you have been spending it on. This is where the priority based budget comes in as a tool to help you with that decision making process. The concept is very simple. You start with the most important things that you want your money to go for. And here we are not talking about the things you “want” the most. We are talking about your most basic needs. You also start with the amount of money you bring in for the month. As you list each expenditure you subtract that amount from your monthly income. So you would start with things like housing (rent or mortgage, and property taxes if applicable), food, electricity, water, heat, insurance, and then continue down the list to “lesser” but necessary to your life expenditures. And as you do this you continue to subtract from your monthly income. By the time you get to the bottom, depending on what your income is you should be getting to your “want” items in order of which things you want the most. When you get down to zero on the other side you are done. You can’t (or I guess I should say shouldn’t) spend money that is not coming in, because this is, of course, what leads to debt. Everyone has different priorities and what would be a frivolous expenditure in my eyes may be a very important source of joy and happiness for you. But the bottom line (zero) is the bottom line no matter what your circumstances are. You cannot go beyond that and this is what forces you to examine what your spending priorities are.  If your money is very tight, you may not even get past the “needs” at the top of the budget. There is no room for “wants” at all. If this is the case you will need to examine how you can increase your income. You can temporarily take on a second job, but you will also need to come up with a more permanent solution to your income dilemma. Can you ask for a raise? Look for a better job in your field? Should you try a different line of work? Get additional education? You need to come up with a plan of action, and start taking the necessary steps to get there. If you have debt, then paying that off should go right after your basic needs are met. If you do not have debt, then you are in a position to start saving and that savings should be at the top of your line items. Retirement savings being at the top, followed by other savings goals. i.e. a wedding, a house, kids (or your own) education, a car, vacation, home improvements, etc. This is the concept of “Pay yourself first” and it works! This way you have all your life goals covered by the time you get down to the bottom of the budget to those everyday “wants”. I have included some budget worksheets that you can use to create your own Priority Based Budget. One has categories to give you some guidelines (but feel free to change them according to your own priorities). And some samples to help you see how it's done: Sample 1. Sample 2. The other is left blank for you to fill in as you see fit. And more samples: Sample 3. Sample 4 The lefthand column of both of them is for you to start with your monthly income and then subtract as you make your way down your list of spending priorities until you get to zero at the bottom... money gone... budget done! You must of course (if you are sensible and want to get ahead with your money) include your saving goals as part of your monthly budget and also things that you will not necessarily spend money on every month, but that you will do so from time to time (like car or home repairs).  Once you finish with this exercise you will have a clear black and white picture of where your money is going according to your own life’s plan. You are on top of your money. You are in control. And that’s a pretty darn good feeling! Congratulations!   Tis the season …for exuberance, generosity and joyful abandonment. It’s so very festive and fun, but oh so easy to get carried away with it all. And temptations to spend are everywhere you look. Deep discounts! Drastically reduced! Prices slashed! The more you buy the more you save! …. Or do you? It certainly doesn’t seem like it when the bills roll in come January … right around the time when you’re making those New Year’s resolutions, it seems. You know, the ones about getting on a budget and stopping the overspending? So, what are some strategies that you can employ to obtain that simple peaceful holiday season and reign in the excess spending? The first thing you can do is pare down those lists. Of people to buy for, indulgences, activities, and, of course, presents to buy. Well, now is the time to stop and think about that. Take a deep breath, have a cup of tea and sit down and contemplate a quieter, simpler, less hectic holiday season. One that you won’t regret when the new year rolls around. One that you’re not paying for until next August. Does that thought bring you joy? Do you feel your blood pressure dropping already?  Sometimes the amount of people we exchange with can become out of hand. What starts out as a nice gesture one year, exchanging with this friend or that relative eventually morphs into a yearly obligation. You may be surprised to find that the other person in this exchange feels the same way and is more than happy to drop the yearly gift swap. Talk to them. Often we also have auxiliary people in our lives to favor with a gift, from teachers to work-related people to babysitters and hairdressers, etc. Many times these people are also swamped with all those many little gifts at holiday time, and though the thought is appreciated they would rather not deal with the deluge. Sometimes a kind and heartfelt note of appreciation is most welcome. If you feel you must give something, make up a big batch of your holiday specialty (cookies, candy, fudge, whatever) and parcel a little out to each of the people in your life that you need to thank. One and done. And edibles are often more appreciated than extra objects to clutter up their lives. Besides paring down the list of people that you exchange with, it is also a good idea to pare down the amount of gifts exchanged. This especially applies our beloved and cherished little offspring. I know it can be so fun to spoil them and see their happy faces when they open that pile of gifts, but is it worth going into debt for? And is it really good for them in the grand scheme of things?  ‘ Have you ever noticed that the more gifts children get the less they are actually appreciated? If they open, open, open more and more gifts the presents themselves become secondary to the act of tearing into the innumerable presents. Is this greedy abandonment really the kind of “happiness” you want for your child? Just a few thoughtful gifts might instill a more genuine thankfulness in your child. My last gift giving tip comes too late for this Christmas, but is certainly something you can start for next Christmas. That is to prepare for the holidays all year, both in your spending and your buying. The old fashioned “envelope system” works great here. Just deposit a little bit out of each paycheck and let that be your holiday budget for next year. Pay cash for your presents and other holiday expenses, and when the money’s gone it’s gone. No more spending. And no credit card bills to fret over in January. You can also spread out your buying for the entire year. Look for those after-Christmas sales. Take advantage of clearance sales throughput the year. And one of my favorites, yard sales and thrift shops. I used to pick up gifts for my kids (often still in the box or with tags on) all summer at yard sales and my Christmas shopping was almost done (for dirt cheap) by October except for a few requested items to round out the list. This works especially well with smaller kids who are not as particular as older kids can get. You can sometimes score presents for the adults on your list this way too (keep them in mind when you look around). So, yes, Virginia (or whatever your name is), you can have a joyous holiday season without going into debt for it. In fact, I might venture to say that you can have an even more joyous and peaceful holiday when you keep it simple and take this time to relax and enjoy yourself with your family and friends without all that frenzied spending. Give it a try. You have nothing to lose and lots to gain! Wishing you all a warm and wonderful holiday and a peaceful and prosperous new year!   I am so excited to welcome you to my new webpage and get started on a money saving journey with my readers. This blog will be chock full of tips and strategies each month that you can use to set and achieve any and all of your financial goals from the short term to long term to the ultimate of a secure, happy, well-funded retirement and even a legacy to leave to your heirs. The new year is traditionally a time of getting started so this is the perfect time to take a look at where you stand right now with your finances and what goals you would like to achieve this year and beyond. No matter where you are at present the best time to get started on improving your financial status is right now! Before you can begin to set goals it is important to know where you are right now. Set aside some time to take a look at where your money is going. Write out an expense sheet. Include all your expenses big and small, from your fixed expenses (rent/mortgage, insurance, cable, phone, etc.) to your more variable expenses (food, heat, gas, clothing, entertainment, etc.). And don’t forget the occasional expenses (school supplies, Christmas, vacations, car repairs, etc.), as well as all those little expenses that you hardly think about (your morning coffee to-go, vending machine treats, lunches out, beauty products, etc.). If you are not in the habit of noting all your expenses, it may take some time to remember them all. I suggest getting a little notebook to record what you spend money on each day at least for a month. (Even I still do this on a daily basis.) You can use this worksheet I've made to complete this step.  In the meantime, take stock of any debt you have. Write down all of your debts including the full amount owed and the interest rates. Add them up to get your total owed. If you have assets, good for you! Take note of them too. Money in the bank? 401k (403b)?, Any investments? And write down what your income is, including all sources; Your (and your spouse’s) salary, child support, SS payments, rental income, extra side jobs, etc. Now that you have a clear picture of where you stand, you can plan your goals. Let me give you a little hint here. Your first goal should be to pay those debts down! No debts? Great! Is there something you want to save up for to buy this year? Do you have a bigger purchase in mind that might take a few years to save up for? (a new car or down payment on a house?) Do you want to save up for education? (yours or your kids). And then of course there is the ultimate goal, that nice comfortable retirement nest-egg! For the smaller goals it is simply a matter of dividing the total needed by the months you have until you need the money. Then you know the exact amount you need to put away each month to achieve it. For that ultimate big retirement reward, slow and steady wins the race. The earlier you start the better off you will be. This should be an automatic amount taken right off the top, before you even see it. Of course a job 401k will do this for you, but if you don’t have access to one you can set up your own retirement account and have automatic deductions going straight into it from your checking or savings account each month. I know this is a lot to contemplate all at once, but for now just take this month to take stock of your expenses and debts, and think about what goals you might have for your money and I will lead you through the rest of it step by step as the year progresses. When you do it step by step you will see how easy it can actually be to turn your finances around. We will start to talk next month about just how to budget your expenses and find the money to put aside for all those goals. ` Stick with me and you too can have a bright future! |

Archives

June 2022

Categories

All

|

RSS Feed

RSS Feed