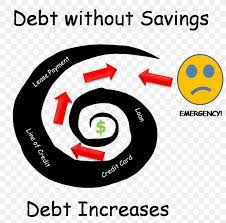

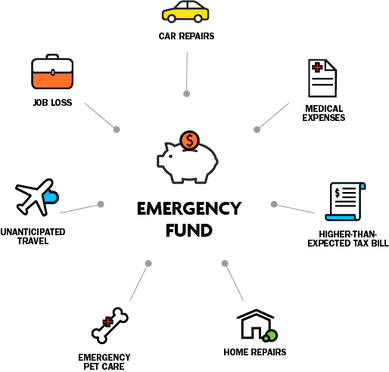

An emergency fund is like an immune system for your financial health. We have germs circulating all around our environment, but if they try to attack us our immune system springs into action to protect us and keep us healthy. If we do not have a healthy, robust immune system those same viruses and bacteria can wreak havoc, make us very sick and possibly even kill us.  And that is what your emergency fund does for your financial health. There are financial “disasters” lurking everywhere around us, just waiting to happen (an appliance goes on the fritz, the roof springs a leak, your car breaks down, your computer dies, you lose your job, etc.) If you do not have that healthy emergency fund to cover the expense, it will derail your finances, can force you to reach for the credit card (or take out a loan), and put you in debt.  Now you are scrambling to not only cover your regular monthly expenses but also to pay back that debt and paying interest on top of that. You can see how, without an emergency fund, one setback can lead you down into a negative financial spiral that can take a very long time to climb out from.  If you do have an emergency fund, you simply use that money to cover your expense and continue on. No panic, no interest payments to deal with. And if your budget already included a small amount going into your emergency fund each month, not even any difference to your monthly expenditures.  So, hopefully, this illustrates to you just how important an emergency fund is to your financial health!  Best of luck to you for creating your own healthy financial situation that can lead you to a very bright future  For how to save up an emergency fund and more on emergency funds see What are Your Emergency Fund Questions?

0 Comments

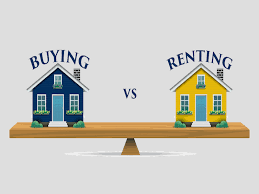

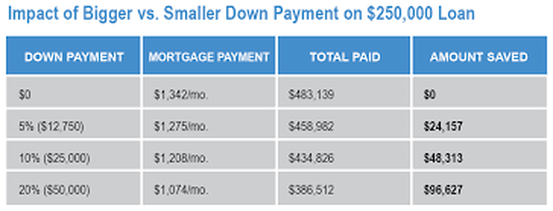

Well, it’s windfall season, and many people are looking forward to a double bonus this year. Not only might you be getting a tax refund, but that third stimulus check may be heading your way at the very same time! The big question is “What do we do with it?” Of course, there are any number of things you can do, and a lot of what you do may ultimately depend on your personality. Are you a spender or a saver?  The great irony here is that the very people who might need to be saving that money (because they have a history of spending) are the ones who may choose to spend it, whereas the natural savers (who are already in good financial stead due to that character trait) are likely to save this money too. So let’s have a run down here on what you should be doing with the money, depending on your individual financial circumstance at the current time. Here is an easy-peasy priority list that you can run down anytime a big fat windfall check comes your way that will give you the best bang for your buck in getting ahead with your finances (which hopefully is your ultimate goal here): 1. Are you current with your bills? If you are not, then this is what you need to use this money for. If this is a struggle for you then it will have to go to your most dire needs, and that’s that. My heart goes out to you during this trying time and I hope as this crisis gets better your situation will improve accordingly.  2. Do you have any debt? Then, by all means, pay it off (or at least down). Start with your smallest debt and pay them off smallest to largest until you have used up all the money. Bonus! Maybe this head start will give you the incentive you need to get serious about continuing on to pay the rest off.  3. Do you have an emergency fund (of three-to-six months-worth of expenses) saved up? If not, put it towards that. Put this in a separate account away from your everyday saving/checking accounts. And again, maybe this will be incentive to keep going and fully fund it! Plenty of people found out this year just how important it is to have one!  4. Do you have any big financial goals you are working to save up for? (a car, education, a wedding, a house, a home repair, or improvement project, a vacation, etc.)? Put it toward that. Open up an online bank account (separate from your everyday account), put the money in there and set up automatic monthly payments going into it to continue funding it until you reach your goal. If this goal is a more long-term savings goal (more than five years away) then you might want to buy a mutual fund to make your deposits into for a greater rate of return on your money. You can do this by opening up a discount brokerage account (such as in Fidelity).  5. Do you have a mortgage? Pay that down (or off!). You do not want to get to retirement age with a mortgage still hanging around your neck. And the faster you can pay it off before retirement the more time you will have to save even more money towards that golden retirement nest-egg! And the less interest you will pay on it in the long run!  6. Retirement. If you are good on all of the above then there is nothing wrong with adding this money to your retirement account, or starting a new one. I know, I didn’t give any “spending” options in this list, but hey, I’m a budget coach. We teach people how to save their money. So, I guess if you are on nice solid financial ground on all fronts and you want to take this money and spend it on something then what can I say? But whatever you do, please put the money to good use. If you really don’t need it at all, maybe you could donate it to those that really do.  This prioritization schedule can be applied to all windfall money that comes into your life at any time for whatever reason. It is very easy to go down the list, see where you are with your finances and know exactly what to do with it.  I hope this helps! As always, wishing you all a very bright financial future!   Sometimes there is just something to be said for boiling it all down into a nutshell and that is just what I have decided to do in this blog. This is pretty much says it all in seven easy-to-follow rules. The best time to start living these rules is from the minute you start that very first job. That is the time to set up good habits that will keep your finances healthy and thriving for your entire life and ultimately lead you on the path to that beautiful dream of financial freedom!  If you know anybody who is just starting out here is the perfect gift for them. Just print these rules out for them and you will have changed the trajectory of their life forever.  1. Always live below your income level (and be saving for retirement and goals). 2. Always be saving at least 15% of your income into your retirement account(s). 3. Always have an emergency fund set up of at least 3–6 months' worth of spending. Your Emergency Fund questions 4. Keep track of all your spending. Know where your money is going! 5. Learn to distinguish wants-vs-needs. Many things that we think of as needs are actually wants. Don’t buy wants if you can’t afford them. 6. Never buy anything on credit (including cars). No Loan Auto Ownership. Save up and pay for things with cash. One exception to this would be a mortgage on a house but put a hefty downpayment down. Get a 15 yr fixed rate mortgage and pay it off ASAP. 7. Pay yourself first! Put your savings on Automatic Pilot. Set up an online bank account (or a few) to save up for your future needs. It’s better if you can have a separate one for each goal (i.e the car account, the wedding account, the vacation account, etc.) Set up automatic payments going into them each month from your checking or savings account. You really can’t go wrong if you live by these simple rules. They're not that hard to do! Wishing you all a very bright future!   Someone I know recently bought a house and my 24-year-old son was asking me about the details. His number one question being “How do people save up that much for a down payment?” As I answered his questions it got me to thinking that I never addressed this topic in these blogs, so here goes:  How do you know when you are ready to buy a house? Well some people think it’s just a matter of saving up that down payment, but really a lot more preparedness needs to go into it. First of all, how settled are you? Many young people move around quite a lot for job changes or other purposes so even if they are very lucky enough to have that down payment at such a young age, it is not necessarily the best time to be putting down roots into home ownership just yet.   Unless you are sure that you will be staying put for at least the next five years, buying a house is rarely a smart move financially. You will sink a lot of money into the act of buying the house (in closing costs, realtors fees, inspections, lawyer’s fees, etc.)  Then once you buy there is the cost of moving in, and often on top of that people will do some work to the house to make it more to their liking. And there is even the inevitable furnishing and decorating, especially if you are starting from “scratch” with nothing.  And if you have put down a small down payment, you will typically not be gaining much equity in the house for the first few years, at least, as most of these initial payments are going to the interest on the mortgage. It is not until the principle starts to go down a little that the mortgage payments will start to chip away at that principle. And of course it also depends on the housing market. Your house could go up in value, giving you more equity but there is also the possibility that it could go down in value and put you in a situation of being “upside down” on your mortgage. That is actually owing more on it than the house is worth. This is what happened to all those people when the housing bubble burst in 2008.   So with all that said, it will take a while before you will get enough principle back when you sell to offset the costs you put in when buying it. If you sell too soon you will not only not gain any money on the sale you could very well come out in the negative for your years of home ownership. If this is the case you would have actually have been better off to continue renting and saving your money. Next, other than that down payment you have saved up, how is your financial situation? Do you have any debts? If you do, it is very smart to pay them off before embarking on your homeownership journey. Do you have an emergency fund (of three to six month’s expenses) saved aside? I would recommend at least six month’s during this transition into home ownership as you never know what can happen. Is your job secure? You don’t want to take on all this extra monthly expense only to be caught high and dry with a loss of income. This type of scenario sends people scrambling and can result in a disastrous situation.  Even if your job is secure, you have a good down payment saved up and you know you will be staying put, have you crunched the numbers to see of you can afford the cost of homeownership? A common mistake people make is this line of thinking. “I am paying X (say $1,500 per month) on my rent so I might as well be paying that amount on a mortgage and actually owning my own home.” The trouble with that is that you must consider all the other costs of owning. Some things that were covered by your landlord before are now your responsibility. Have you thought about taxes, homeowners insurance, (PMI if you have a small down payment), electricity, heat, TV, internet, water, rubbish removal, etc.?  And in addition to all those fixed expenses, if the house is yours, you are now responsible for the upkeep. And no matter what great shape that house was in when you bought it, something always needs attention. Sometimes it seems barely a month goes by without an unexpected household expense. Even non-household expenses can derail you if you are “living on the edge”, just making all your monthly bills without a penny to spare. This is why it is so important to have that emergency fund set up before you move in.  Now what about that down payment? I just mentioned PMI in the previous paragraph. What is that that? If you put less than a 20% down payment then you have to pay Private Mortgage Insurance. And although you are responsible for these premiums this insurance does nothing to protect you. It is to protect the bank from losing the money they lent you should you default on your payments.    So, this brings us to my son’s question. How much of a down payment should you put down and how do you save up that kind of money? The answer to the first question is as much as possible, at the very least 20% (to avoid that PMI) If it’s home ownership you are after (and not living in a bank-owned house that you are paying dearly for (in interest payments) you should set your sights on the biggest chunk of money you can plop down.  Another way to keep your down payment at a higher percentage of the cost of the house is to buy a less expensive house. This way that same down payment you have saved is now a larger percent of the total cost. You can always move into bigger house (or expand the one you are in) down the line should the need arise and your finances improve. Here’s a dirty little secret the banks don’t want you to know. They will approve you of a mortgage that is really out of a comfortable price range for you. Why? Because they are really not interested in how comfortable you are making the payments. They are just looking to get the biggest mortgage for themselves (the more you borrow, the more interest payments they will get). So buy a house that you are comfortable with (monthly payment wise), not what the bank approves you for, and ideally this monthly payment should be no more that ¼ of your monthly income. And one more thing on the subject of mortgages. The bank will automatically default to a 30-year-mortgage, but you are much better off to get a 15-year. The quicker you can get that house paid off, the less total interest you will pay on it. You can save yourself many thousands of dollars (even hundreds of thousands) by just doing this one thing.  Now to Jesse’s question of how to save up for that mortgage. The same way I recommend you save up for anything else. Make it automatic! Open up an online account and set up automatic monthly payments going into it. Take the total amount you want to save and divide it by the months until you want to have the money. If you want to save up a $75,000 down payment in four years that would mean you need to save about $1,500 per month. *See Easy Peasy Make it Automatic  If your timeline for savings is actually more than five years then you might want to consider investing (all or part of) the money into a low cost (relatively safe) mutual fund (such as an S&P 500). Putting those payments away each month will also help you to be living below your income and able to make all those extra expenses when you do move into that house. Owning your own home is the American Dream. It is a great feeling to live in a house of your very own and can also be a real plus to your total financial picture if you are indeed prepared for it, but please make sure you are fully ready before taking the plunge or it has the potential for turning into a nightmare. Do it right and make it your dream come true!  Best of luck to you if you are looking to embark on this exciting new chapter of your story. Wishing you a bright future in your own home sweet home!   I have been talking in this space for years now with tips about how to save money and especially lately, of course, with so many people feeling the financial pinch of this Covid lockdown, saving money has become crucial. But someone posed the very legitimate question of where exactly they should be putting their savings. Some people just keep it in their regular (everyday) checking or savings account. That is not a good idea, and I will l explain why.  You (should) have more than one savings goal for your money, and keeping it in a lump sum actually tricks the mind into thinking you have more money than you do. And for some people this makes it very tempting to spend it. This is the other reason to keep it separate from your everyday money. Once you break it down into the various needs you have for your money you get a more realistic picture of how much you have and how much you still need to save.  Here is a breakdown of some goals you might have and where you should be putting the money for them: #1 Retirement: This can be a 401k or other workplace IRA account, or an IRA you have set up for yourself. At least 15–20% of your income should be going into that. Within that 401k or IRA, the money should be invested, of course. Low cost (index fund) mutual funds are fine. If you want to get fancier than that it is entirely up to you.  #2 An emergency fund: This is especially important in these uncertain times we are going through. If you don’t have a fully-funded emergency fund (at least 3–6 months-worth of expenses), money should be going into this each month. In fact, during this time you might want to beef this up even more. When you reach the 3–6-month goal (or more) then just leave that sitting in a separate account for when you need it. This should be a liquid readily accessible account (not invested).  ,#3 A car fund: Most people own a car and should always be saving towards the next one (paying car payments to yourself) so that you never have to finance one. Get off that car payment carousel! This will save you untold amounts of interest payments thrown away to the bank during the course of your lifetime. If you have no need for a car, then obviously this one does not apply to you,  #4 Other savings goals: I recommend you separate them out into separate accounts. This is anything else you are saving for, a wedding, down-payment on a house, home repairs, trip, kids college, etc.  For most of these savings I recommend you open up an online bank account (or more than one) and then set up automatic payments going into them (from your regular checking/saving account), calculating how much you will need for that goal and the amount of time you have to save for it. I suggest this for two reasons. One, the online banks have a slightly higher interest rate than brick and mortar’s do, and two, they are (at least psychologically) less accessible (out of sight/out of mind), so you will be less tempted to dip into them. And labeling them with a certain goal makes them more “off limits” to impulse spending too.  One more thing. If any of these goals is on a long-range timeline (you will not be needing this money for at least five years or longer), then you might consider buying a (low-cost index fund) mutual fund to be putting that money into for better returns. Since the market is volatile by nature, I would not recommend doing this for any shorter range goals as you risk losing (some of) your money. But for longer range goals, it is a pretty safe bet that, with the usual returns on the stock market, you are likely to do better with this money than putting it into a savings account.  So now you have an exact blueprint of where and how to save your money. Just plug in your particular goals and you can have the whole thing set up in one afternoon. And the beauty of this automatic savings is once it’s done you never have to think about it again. All you have to do is tweak it from time to time as your goals change (and/or are met). You can just get on with your life and stop stressing about money. And that’s what this whole money saving business that I’ve been teaching you is all about! 😀 A peaceful stress-free life!  Wishing you a bright, stress-free, peaceful life of savings!   This strange lockdown we have found ourselves in and the resultant loss or decrease in income has left many people to ponder their financial situation and ways they have been managing their money up until this point. As I mentioned in the previous blogs, some people are just now waking up to the need for setting money aside for times such as this. The idea of the emergency fund has resurfaced into people’s consciousness, and the term is being batted around quite a bit of late. So I thought I would dedicate this space to the topic.  First of all, what is an emergency fund, and why do we need one? The general consensus is that we should have about 3-6-months-worth of living expenses put aside, that is there to be used strictly for emergencies only. This money is best kept in an online bank account (slightly better interest rate) and completely separate from your everyday checking/savings accounts. The exact amount in there is up to you. If your income is very variable or otherwise unstable, then the larger amount (6 months) would be advised. Some people prefer to have even more than 6-months-worth if their income is very unstable, or they are very risk averse, or prefer more of a cushion. Everyone, no matter how stable they think their income is, should have at least 3 months at the bare minimum, because no matter how good things are going for you right now, “s#@t” happens!  The purpose of having that fund is to keep your finances from being derailed when the unexpected happens. If you have that cushion put aside you can just dip in, pay that medical bill, or home repair or live on it through a job loss and get right back on track where you left off without throwing your whole finances into a tizzy. And even more importantly you won’t be forced to reach into your wallet for the credit card and put yourself into debt over the situation.  Someone posed the question to me recently: “How do I determine when to take money out of my emergency fund?.” An excellent question, and that is why I chose to address it in this month’s blog. The bottom line is this, the more you budget for the unexpected, the less you will ever have to dip into your emergency fund. It’s as simple as that. So how do you determine when you really do need to break that piggy bank?  Before dipping into the emergency fund you should ask yourself: “Do I really need to use this money right now?” Do you have some time to save up the money that you need, and get by without it for a while. Can you get by without whatever the expenditure is altogether? “Is this something I really need to buy?” Can you borrow something (at least while you save up)? Can you make do without it in some other way? “Is buying this thing right now really necessary?” Maybe it’s not the “need” you think it is, but more of a “want”. “Is this purchase right now really worth the sacrifice it will take to replenish my emergency account?” “If I don’t spend the money right now on this emergency will this situation cost me more money in the long run?” (i.e. a car or house repair that will get worse if left unfixed). In that case, by all means, do it.  And after you have dipped into your emergency fund consider if this expense is something you should be adding to your monthly budget so that you are prepared for this type of emergency in the future (I.e. beefing up your “car repair” or “home repair” fund, or adding a new category to cover whatever the expense was).  Ideally, if you have budgeted for every possible “unexpected” expense that may come your way, your emergency fund becomes just a big fat luxurious cushion for you to sit on and enjoy the security of. Wouldn’t that be a nice feeling!  Wishing you a bright secure future!

There is panic all around us. What should we be doing to keep ourselves and our loved ones safe? How long will this last? What supplies do we need? Do we have enough toilet paper? Sometimes we can be blindsided by what life throws at us. The best way to be prepared for the unexpected is to, well, be prepared.  In the case of a new disease coming your way, you are in a much better position to deal with it if you have been living a good healthy life up until that point, eating good fresh whole foods, getting proper rest and exercise, maintaining a healthy weight, etc.. If you have been living this way, chances are you have a much better immune system to fight off the infection. But if you have been eating a poor diet, are out of shape and overweight, leading to possible chronic conditions, can you suddenly start living a healthy lifestyle and expect to have the same healthy immunity as the infection invades your community?  Obviously you would have had to been building up that immunity and living a healthy lifestyle for quite some time for it to be effective for you now. I guess you are getting the idea of where this is leading to. The way we live our everyday financial lives also has a big impact on how well we are prepared for whatever life may throw our way.   Perhaps this coronavirus has directly (or even indirectly) affected your income. Are you financially prepared to weather the storm? Times like this bring home just how important it is to live below your means (when you have means) and constantly be putting money away for the lean times (or that big “lean time” in your future, otherwise known as retirement).  If your ordinary life includes having no debt, having a good emergency fund put aside, and saving on a regular basis, then you are much less likely to feel panic and upheaval when you come to a bump in the road. The more “padding” you have the less you will feel those bumps. Things that are a (financial) crisis to the ill prepared are merely blips to those that have the money to deal with them and move on.    If you see the sense in this and would like to shift from a living-on-the-edge (paycheck to paycheck) lifestyle there are many actions that you can begin to take to shift to a saving way of life. If you don’t know where to start I have many blogs on various aspects of money saving strategies that you can implement. Right now, while you are likely sequestered at home, might be the best time to finally sit down and take a good look at your financial situation and take control. Here are just a few that you might find particularly helpful: New Year Savings Resolutions Would You Love to Save More Money? Spring Clean Your Finances Strengthen Your Frugal Muscle, Lighten Your Stress Easy Peasy Savings, Make it Automatic Saving Money Every Day The Perks, Pluses, and Payoffs of Prioritizing My Message to Millennials Ready, Set, Goal! Money Saving Grocery tips from your “Auntie” Victoria And if you scroll through the rest of the blogs, you may find some more that apply to your particular situation and needs. If you need further individual help feel free to contact me at (845) 758-0250, or brightfuture2budgt4.gmail.com for a personal appointment.  Wishing you all the best for staying healthy now and moving toward a healthy financial future.

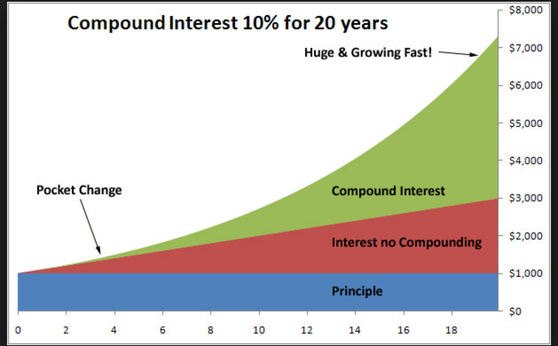

Having spoken with a few millennials lately, including one young lady who was very motivated to get started on the right financial footing, (this is not always the case with the young people I encounter), I thought I’d devote this blog entry to those just starting out on their lives’ journey. This is the stuff that I wish somebody had told me when I was just starting out. I figured it out along the way, but it would have been nice to know it all from the beginning. And some people, unfortunately, just never do figure it out for themselves. Would I have listened? Who knows? But, as they say, if I knew then what I know now, and followed the advice I am about to impart to you, I would very easily be a multi-millionaire by now. And you can be too. Anyone can do it.  Often I find myself very frustrated that young adults, who have the most to gain from learning to be smart with their finances, can be the most resistant to hearing (and following) it. And the sad thing is that if they don’t do it now, although they can still do alright whenever they decide to start, they can never make up for that lost time and the money they could have made by investing early. The magic of all those years of compound interest can never be regained.   So, without further ado, in a nutshell, here are my most salient tips for millennials: #1. The golden rule of finance: Always, Always, Always Live Below Your Means! Start out that way and get used to it. As your income increases you can increase your lifestyle, but always stay below what you are making. 15% of your income should going into your retirement fund at all times.  #2. The other golden rule of finance: Pay Yourself First! You will be paying out a lot of your hard earned money to other people and businesses in your lifetime (your landlord, the mortgage bank, electric company, insurance companies, gas company, food producers, goods manufacturers, health care providers, etc., etc., etc.,…..), but don’t give all your money away to other people or you will have nothing to show for it. Always be keeping something for yourself… up front, before any of your money goes out to anyone else.  #3. Make it Automatic Set up that money to go into your retirement account (401k or Roth IRA) and your other savings (goal) accounts straight out of every paycheck before you even see the money. Out of sight, out of mind.  #4. Keep track of your expenses Set up a system so that you know exactly how much you are spending, every day, every month, every year, and on what. You can do this by hand (simply writing it down) by computer (i.e. your own spread sheet) or with a website (such as mint.com)  #5 Prioritize your budget: Spend your money on what is most important to YOU First comes dire needs, housing, food, transportation, etc. Then prioritize the rest according to your income and needs. Wants come last, and only if you can afford them. Think carefully about wants-vs-needs. Do you really want to sabotage your future goals for some frivolous indulgences today?  #6 Plan for your goals Write them down and save for them systematically (how much do you need to save and when do you want it?). Do you want to get an education? Plan a wedding? Buy a house? Buy a car? Go on a vacation? Always be saving for your future purchases so that you will… (see #7)  #7 Never borrow money! (AKA buy things on credit) Don’t get into the interest paying trap. It is a slippery slope once you start on the debt quagmire. This includes education (student loans), cars (car loans), and those insidious credit cards. Always save up and pay for things in cash. If you don’t have the money, you can’t afford it. The only possible exception to this is buying a house. But even here, if you can manage to save up and pay cash that would be awesome. People do it. I did it for my second house (after I paid the first off by ten years). Certainly aim to put down as large a down-payment as you can and take out a 15-year mortgage. Then (pre)pay that down as quickly as possible. And don’t buy a more expensive house than you can afford. Though the lending banks will pre-approve you for a much bigger mortgage than you can comfortably afford, don't fall for it.  It’s really as easy as following these 7 very simple rules and you will be set for life. It’s not rocket science. Anyone can do it, at any income level. Stick with this lifestyle and you will go from millennial to millionaire, a very bright future indeed!  Which one are you? Hopefully in the green!  You can do it!!

You’ve all heard the expression “April flowers bring May Flowers” I’m sure. But what does it mean? Well in its literal sense of course, we need the rains of early spring to give us those beautiful flowers to enjoy in May. But what is the deeper meaning of the phrase beyond that? When we say it we are talking about how we are willing to put up with some less desirable weather in April because we know it is necessary so that we may delight in the lovely blooms that follow. But we can also apply the phrase to other situations in life. Very often it is easier to endure a less than pleasant circumstance because we know it is essential for something better to come. The financial guru Dave Ramsey has a great saying “Live like no one else so you can live (and give) like no one else later on.” In other words, if you have a future financial goal in mind you will be willing to make the sacrifices that it takes right now in order to attain them. You appreciate the showers because you know they will result in a richness of flowers.  Are you a grasshopper or an ant? The grasshopper will ignore the future and just live for today only to be surprised when winter comes and he has nothing put aside to get him through the cold snowy months. Meanwhile, the ant has been working throughout the summer to build up a stash to sustain her throughout those food barren months. Does this mean that the ant has no fun while he is preparing for the future? Absolutely not! There are a great many ways that that little ant can have fun while also taking the time to put those resources away for that rainy day. But the wise little ant always keeps in mind that winter is coming and does what she needs to do to be prepared.  So, yes, enjoy yourself for today. There are any number of ways that you can enjoy life for very little cost or for free. But if you are a wise little ant you will always be stocking up for the future so that (unlike that silly irresponsible grasshopper) when the future comes you will have an abundance to enjoy and your winter will be more like a gorgeous phantasmagorical riot of spring blossoms. Because you, my little friend, prepared for it.  |

Archives

June 2022

Categories

All

|

RSS Feed

RSS Feed