Well, it’s windfall season, and many people are looking forward to a double bonus this year. Not only might you be getting a tax refund, but that third stimulus check may be heading your way at the very same time! The big question is “What do we do with it?” Of course, there are any number of things you can do, and a lot of what you do may ultimately depend on your personality. Are you a spender or a saver?  The great irony here is that the very people who might need to be saving that money (because they have a history of spending) are the ones who may choose to spend it, whereas the natural savers (who are already in good financial stead due to that character trait) are likely to save this money too. So let’s have a run down here on what you should be doing with the money, depending on your individual financial circumstance at the current time. Here is an easy-peasy priority list that you can run down anytime a big fat windfall check comes your way that will give you the best bang for your buck in getting ahead with your finances (which hopefully is your ultimate goal here): 1. Are you current with your bills? If you are not, then this is what you need to use this money for. If this is a struggle for you then it will have to go to your most dire needs, and that’s that. My heart goes out to you during this trying time and I hope as this crisis gets better your situation will improve accordingly.  2. Do you have any debt? Then, by all means, pay it off (or at least down). Start with your smallest debt and pay them off smallest to largest until you have used up all the money. Bonus! Maybe this head start will give you the incentive you need to get serious about continuing on to pay the rest off.  3. Do you have an emergency fund (of three-to-six months-worth of expenses) saved up? If not, put it towards that. Put this in a separate account away from your everyday saving/checking accounts. And again, maybe this will be incentive to keep going and fully fund it! Plenty of people found out this year just how important it is to have one!  4. Do you have any big financial goals you are working to save up for? (a car, education, a wedding, a house, a home repair, or improvement project, a vacation, etc.)? Put it toward that. Open up an online bank account (separate from your everyday account), put the money in there and set up automatic monthly payments going into it to continue funding it until you reach your goal. If this goal is a more long-term savings goal (more than five years away) then you might want to buy a mutual fund to make your deposits into for a greater rate of return on your money. You can do this by opening up a discount brokerage account (such as in Fidelity).  5. Do you have a mortgage? Pay that down (or off!). You do not want to get to retirement age with a mortgage still hanging around your neck. And the faster you can pay it off before retirement the more time you will have to save even more money towards that golden retirement nest-egg! And the less interest you will pay on it in the long run!  6. Retirement. If you are good on all of the above then there is nothing wrong with adding this money to your retirement account, or starting a new one. I know, I didn’t give any “spending” options in this list, but hey, I’m a budget coach. We teach people how to save their money. So, I guess if you are on nice solid financial ground on all fronts and you want to take this money and spend it on something then what can I say? But whatever you do, please put the money to good use. If you really don’t need it at all, maybe you could donate it to those that really do.  This prioritization schedule can be applied to all windfall money that comes into your life at any time for whatever reason. It is very easy to go down the list, see where you are with your finances and know exactly what to do with it.  I hope this helps! As always, wishing you all a very bright financial future!

0 Comments

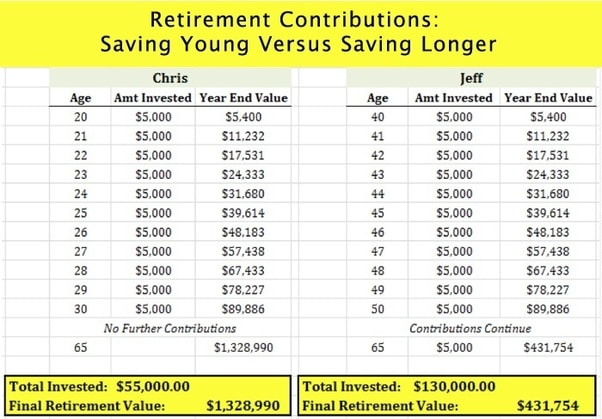

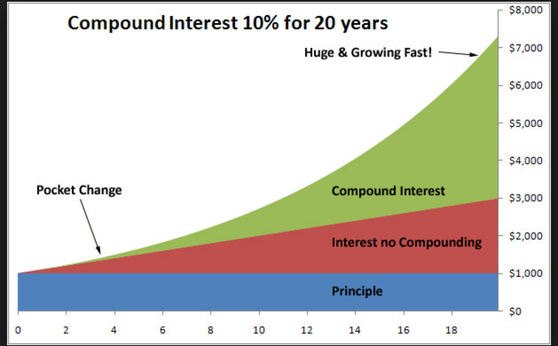

I’ve seen or heard this question posted in many different ways throughout the years, the gist of it being that one needs to make a fundamental decision between enjoying their life or saving for the future. I’ve heard the argument that you must “live” for today because you could be hit by a bus tomorrow. Young people have screamed YOYO! (Did I just coin that?), as in, “You’re Only Young Once”. They maintain that they must spend and “live” for today while they are young enough to enjoy it.  But I don’t see it as a black and white, either/or situation: Save OR have fun. I believe that if you are wise with your money you can do both. Saving your money does not mean that you have to be a miserly scrooge sitting in your lonely attic counting your money and never having any fun. In fact, with a little planning and wise money management you can easily have a very pleasurable life and also save for your future at the same time.  The one equation that people need to let go of is “Spending Money = Fun.” There may be some correlation to that sometimes, but it is certainly not a given. You can spend lots of money on something and have a terrible time, and even more importantly it is very possible to have a great time spending no money at all. I’m sure you can think of several examples of both these facts in your own life. Let’s start with the young (my newly coined YOYO philosophy). Yes, they can certainly save and also have fun. First of all, they have one huge advantage in their favor… the magic of compound interest. The fact is if you start saving (investing) early you will only need to save a fraction of your own money in order to build up a very tidy nest egg for retirement. Most of the money in your IRA at retirement will be growth on the returns you accrued through the years (not the money you actually put in). Pretty neat trick, huh?  With a little prioritizing and forethought young folks can also be saving for their other more near-future needs/wants (a car, a house, a wedding, et.) by putting those savings on automatic pilot and just living on what’s left. The prioritizing comes in as you make the conscious decision to forego (instant pleasure X) which is not really adding a great deal of joy to your life in order to save up for that something that will bring you great pleasure indeed.  The one joy that seems to be mentioned a lot is traveling. And here is where the young have another distinct advantage. They can travel for practically nothing, staying in youth hostels, or other low cost accommodations. There are even many temporary internship/job opportunities overseas that can allow them to see the world while sometimes even making a little money. The possibilities of low-cost travel are only limited by the imagination for the young (or young at heart). Google “traveling on next to nothing” and see what you come up with. I read a great memoir on the subject a while back called “No Baggage – A Minimalist Tale of Love and Wandering” by Clara Bensen.  What about if you are not young? I see people of all ages squandering their money on daily instant gratification pleasures without even realizing that they are doing it. Once, when I was telling some friends about a trip to Singapore that I had just returned from, somebody asked me “I don’t understand. You can’t afford cable TV, but you can afford a trip to Singapore?” My answer to that is you can afford anything (within reason, of course), but you can’t afford everything. I chose to forgo all those channels at $150/month in order to save my money for something better. I even found a way to get TV for free (an old fashioned roof antenna). I also put my frugal skills to use to make the trip possible without breaking the piggybank.   If fun is your priority, then go ahead and have it! Have as much as you want. Live! Take advantage of all that free fun that is out there for the taking. If there is some kind of fun that you must have money for, then just look at your spending habits and give something up that does not bring as much joy and save up for what you want.   I see absolutely no reason why you can’t do both. Save and have fun! After all, you only live once!  Wishing you a happy life today and a bright future tomorrow!   I have been talking in this space for years now with tips about how to save money and especially lately, of course, with so many people feeling the financial pinch of this Covid lockdown, saving money has become crucial. But someone posed the very legitimate question of where exactly they should be putting their savings. Some people just keep it in their regular (everyday) checking or savings account. That is not a good idea, and I will l explain why.  You (should) have more than one savings goal for your money, and keeping it in a lump sum actually tricks the mind into thinking you have more money than you do. And for some people this makes it very tempting to spend it. This is the other reason to keep it separate from your everyday money. Once you break it down into the various needs you have for your money you get a more realistic picture of how much you have and how much you still need to save.  Here is a breakdown of some goals you might have and where you should be putting the money for them: #1 Retirement: This can be a 401k or other workplace IRA account, or an IRA you have set up for yourself. At least 15–20% of your income should be going into that. Within that 401k or IRA, the money should be invested, of course. Low cost (index fund) mutual funds are fine. If you want to get fancier than that it is entirely up to you.  #2 An emergency fund: This is especially important in these uncertain times we are going through. If you don’t have a fully-funded emergency fund (at least 3–6 months-worth of expenses), money should be going into this each month. In fact, during this time you might want to beef this up even more. When you reach the 3–6-month goal (or more) then just leave that sitting in a separate account for when you need it. This should be a liquid readily accessible account (not invested).  ,#3 A car fund: Most people own a car and should always be saving towards the next one (paying car payments to yourself) so that you never have to finance one. Get off that car payment carousel! This will save you untold amounts of interest payments thrown away to the bank during the course of your lifetime. If you have no need for a car, then obviously this one does not apply to you,  #4 Other savings goals: I recommend you separate them out into separate accounts. This is anything else you are saving for, a wedding, down-payment on a house, home repairs, trip, kids college, etc.  For most of these savings I recommend you open up an online bank account (or more than one) and then set up automatic payments going into them (from your regular checking/saving account), calculating how much you will need for that goal and the amount of time you have to save for it. I suggest this for two reasons. One, the online banks have a slightly higher interest rate than brick and mortar’s do, and two, they are (at least psychologically) less accessible (out of sight/out of mind), so you will be less tempted to dip into them. And labeling them with a certain goal makes them more “off limits” to impulse spending too.  One more thing. If any of these goals is on a long-range timeline (you will not be needing this money for at least five years or longer), then you might consider buying a (low-cost index fund) mutual fund to be putting that money into for better returns. Since the market is volatile by nature, I would not recommend doing this for any shorter range goals as you risk losing (some of) your money. But for longer range goals, it is a pretty safe bet that, with the usual returns on the stock market, you are likely to do better with this money than putting it into a savings account.  So now you have an exact blueprint of where and how to save your money. Just plug in your particular goals and you can have the whole thing set up in one afternoon. And the beauty of this automatic savings is once it’s done you never have to think about it again. All you have to do is tweak it from time to time as your goals change (and/or are met). You can just get on with your life and stop stressing about money. And that’s what this whole money saving business that I’ve been teaching you is all about! 😀 A peaceful stress-free life!  Wishing you a bright, stress-free, peaceful life of savings!   It’s May Flowers month, so I would like to take this month’s blog to look on the brighter side. We began this quarantine journey during the raw March winds when we too were raw and reeling from the shock of what was happening. Many people experienced a job loss or at least a reduction in pay. We could barely wrap our brains around what was happening. All we could do was retreat to our homes, as we were told to do, and try to make sense of it all.  We remained hunkered down through the rains of April, for the most part even unable to get outside much in the soggy world out there. As the temperatures plummeted out there so did our investments, and often our spirits. Things looked pretty bleak. All we could do was take stock of where we were financially and in every other way. For those of us who still had jobs it was just a matter of staying afloat and ignoring the stock market plunge (as we are always told to do), and stay the course. For those struggling with income loss it was a matter of prioritizing and taking care of the most pressing needs (shelter and food). The rest would have to be figured out eventually.  “But Victoria”, I can hear you saying now, “I thought this was going to be a silver linings message?” Ok, well now it’s May. The month of flowers. We are still home, but the initial shock has worn off a little. Those that have lost income have hopefully figured out a way to get their most important needs met. Maybe they are getting unemployment, SNAP benefits, food from a food bank, their stimulus check, or help from other sources. The rest of us are learning to live at home, creating new routines, keeping ourselves busy and occupied.  But the real May flowers are going to be what we take away for having gone through this. For many this time has given us somewhat of a wake-up call. We were hurrying along through life without even thinking about where all our money and time were going. This has given us time to pause, and think, and live a different way, whether we wanted to or not. Many are surprised to see how little they are spending now that they are forced to stay home, unable to go to restaurants, coffee shops, stores, bars, movies, concerts, etc., etc. Some never paid attention to how much all that was really costing them. And some are finding that they actually can lead a pretty good life without all that spending. Perhaps they will rethink it when life returns to normal. So that’s a silver lining. Forced savings helps you discover a different way.  Some people were caught short with no savings to help get them through a time of no income. It’s a hard lesson to learn for sure, but a lesson learned nonetheless. In either case being at home gives you the time to step back and examine the way you have been living, where your money has been going and to make some changes moving forward. What was once an abstract notion “I know I should be saving up for an emergency fund” becomes stark reality, and hopefully, brings about positive change for the future. A silver lining!  The silver linings go beyond all that though. As usual when we go through tough times, it brings out the goodness in people. Acts of kindness and generosity abound. It is heartwarming to hear the stories of people going above and beyond for their neighbors, friends and people they don’t even know.  And staying at home has given us a chance to live at a different pace, to stop all the rushing about and really spend time with each other in ways we rarely do when life is going full tilt. We have been playing board games, making meals and baking together, even just talking and going for long walks together. Some people have reconnected with old hobbies that they never had time for when life was in full swing. Knitting, gardening, painting, playing an instrument... All that is the best silver lining of all as far as I am concerned. If you know me at all, in person or from my writing, you know that I have long championed the slower, simpler, frugal lifestyle that has now become a forced reality for many.     I would like to think that some of this will stick, that at least some people will come away from all this with a new perspective. Priorities will shift. People will slow down just a little. Spend more time home with their families and less money on needless frivolities. I think that would be the biggest silver lining of all. A beautiful May flower indeed!   Now if only something would come along to force us to reduce our screen time… Wishing you all a bright and beautiful flowery future!    Have you been caught short with a sudden loss of income? Or even a reduction of income, at least temporarily? Times like this can turn your world upside down. Your priorities become putting food on the table and keeping a roof over your head. It’s hard to think beyond that and you may never have experienced anything like this before. It’s hard to believe but not so long ago, historically, this was how most people lived throughout most of their lives on a daily basis. In the 1800’s this was how many people struggled through life. They lived a very frugal existence without even thinking about it. It’s just what they had to do to survive, but then came industrialization and things began to change. People could feel more secure in their daily lives.  The Great Depression brought it all back. Food insecurity and the daily scramble just to survive. Frugal living was once again the norm. There have been a few more lean times, WW II, and a few lesser stock market downfalls that have shaken people’s financial worlds… but with no real lasting effect (on people's behavior), and now this...  Most people who came through the Great Depression tended to continue to feel that insecurity and lived the rest of their lives in a frugal manner. Their children were raised in that manner, and learned frugality to some extent. But now we have gotten too far away for it to have any real impact on the way we live now, and we all live a much richer lifestyle than those people of yore.  So, this coronavirus situation and the financial repercussions has really come as quite a shock, and is leaving many people at a loss as to how to proceed from here. It all depends on your own personal situation. If you still have a paycheck coming in, then the worst of it is psychological, the fear, and stress of dealing with our new upside down world. But if you can stay calm and just hunker down and get through this it will all be ok in the end. If you have investments you have obviously seen them drop, but don’t panic. Sit tight and they will rise again. That is just how the stock market works  If you have experienced loss of income and you don’t have an emergency fund, then just concentrate on your most pressing needs at the moment to get through this. You need a roof over your head (and the recent rent/mortgage freeze will take care of that for the time being) and you need food. If you really can’t afford even that then there are charities and agencies to help you with free food right now. And you can apply for food stamps as well (unemployment too). Beyond that don’t worry about your monthly bills. Contact your loan and credit card companies. They all know the situation and will hopefully defer them for now. The same for any medical bills you are paying. Luckily heat season is over, so that's one less thing to worry about. If you can’t pay your electric bill contact the company. Insurance companies must give you a grace period right now as per the CARE act. That takes care of your monthly bills for the time being.  When your stimulus check comes in, prioritize it for the best possible use. If you need it to live on, then put it in your checking account and use it for your most dire immediate needs. If you are not going to need the money for your current emergency situation, then it is a good idea to use it to pay down your debt and/or put it aside for an emergency fund if you don’t have one. Put this in a separate bank account that you don’t ordinarily access, such as setting up an account in an online bank.  And finally, now that you are stuck at home, if you never want to feel the bottom drop out from you again (financially), it is a good time to re-examine your spending habits. Take a good look at what you have been spending money on. Write down some savings goals. (Hint: one of them should be to save up an emergency fund.) Is your spending keeping you from your future goals? Are you robbing yourself of financial security and a decent future by giving in to reckless, unnecessary spending today? Do you ever want to find yourself in a scary financial situation like this again?  Now is the time, while you have the time, to think about what your priorities are and make a budget to reflect them. Now you have time together at home to discuss your goals and dreams for the future with your loved ones. This could be a turning point in your life. Make the most of a bad situation and turn it around to work for you. You can do it!  Wishing you all safety and good health! And a bright Future!   Having spoken with a few millennials lately, including one young lady who was very motivated to get started on the right financial footing, (this is not always the case with the young people I encounter), I thought I’d devote this blog entry to those just starting out on their lives’ journey. This is the stuff that I wish somebody had told me when I was just starting out. I figured it out along the way, but it would have been nice to know it all from the beginning. And some people, unfortunately, just never do figure it out for themselves. Would I have listened? Who knows? But, as they say, if I knew then what I know now, and followed the advice I am about to impart to you, I would very easily be a multi-millionaire by now. And you can be too. Anyone can do it.  Often I find myself very frustrated that young adults, who have the most to gain from learning to be smart with their finances, can be the most resistant to hearing (and following) it. And the sad thing is that if they don’t do it now, although they can still do alright whenever they decide to start, they can never make up for that lost time and the money they could have made by investing early. The magic of all those years of compound interest can never be regained.   So, without further ado, in a nutshell, here are my most salient tips for millennials: #1. The golden rule of finance: Always, Always, Always Live Below Your Means! Start out that way and get used to it. As your income increases you can increase your lifestyle, but always stay below what you are making. 15% of your income should going into your retirement fund at all times.  #2. The other golden rule of finance: Pay Yourself First! You will be paying out a lot of your hard earned money to other people and businesses in your lifetime (your landlord, the mortgage bank, electric company, insurance companies, gas company, food producers, goods manufacturers, health care providers, etc., etc., etc.,…..), but don’t give all your money away to other people or you will have nothing to show for it. Always be keeping something for yourself… up front, before any of your money goes out to anyone else.  #3. Make it Automatic Set up that money to go into your retirement account (401k or Roth IRA) and your other savings (goal) accounts straight out of every paycheck before you even see the money. Out of sight, out of mind.  #4. Keep track of your expenses Set up a system so that you know exactly how much you are spending, every day, every month, every year, and on what. You can do this by hand (simply writing it down) by computer (i.e. your own spread sheet) or with a website (such as mint.com)  #5 Prioritize your budget: Spend your money on what is most important to YOU First comes dire needs, housing, food, transportation, etc. Then prioritize the rest according to your income and needs. Wants come last, and only if you can afford them. Think carefully about wants-vs-needs. Do you really want to sabotage your future goals for some frivolous indulgences today?  #6 Plan for your goals Write them down and save for them systematically (how much do you need to save and when do you want it?). Do you want to get an education? Plan a wedding? Buy a house? Buy a car? Go on a vacation? Always be saving for your future purchases so that you will… (see #7)  #7 Never borrow money! (AKA buy things on credit) Don’t get into the interest paying trap. It is a slippery slope once you start on the debt quagmire. This includes education (student loans), cars (car loans), and those insidious credit cards. Always save up and pay for things in cash. If you don’t have the money, you can’t afford it. The only possible exception to this is buying a house. But even here, if you can manage to save up and pay cash that would be awesome. People do it. I did it for my second house (after I paid the first off by ten years). Certainly aim to put down as large a down-payment as you can and take out a 15-year mortgage. Then (pre)pay that down as quickly as possible. And don’t buy a more expensive house than you can afford. Though the lending banks will pre-approve you for a much bigger mortgage than you can comfortably afford, don't fall for it.  It’s really as easy as following these 7 very simple rules and you will be set for life. It’s not rocket science. Anyone can do it, at any income level. Stick with this lifestyle and you will go from millennial to millionaire, a very bright future indeed!  Which one are you? Hopefully in the green!  You can do it!!

Do you need a vacation? And can you afford one? Well those are two very different questions. The answer to question one? Hmmm . . . need? I would say in Maslow’s hierarchy of needs it would be pretty low down on the list. But do you want a vacation? Well, that’s an entirely different question! As for the second question, the simple answer is if you have the money to pay for it upfront (and are not taking this money from a more pressing need), then you can afford it. If you need to finance the cost, then no, you cannot afford it. So what can you do to make it more affordable? Ahhh… well that’s where I come in! A thoughtfully planned out vacation does not have to break the piggy bank. If you are aware of your budget up front, which you are, since you have put the money aside for it, there are many tricks and tips you can use to keep it affordable. If you are going to whip out the plastic to book it and then again all through the trip you can easily lose track of how much your spending is racking up to. Once the vacation is over, is that one week of relaxation worth the stress of having to pay it off until the next round of big spending at the holidays?  So, that said, you will start by planning a vacation that you can realistically afford. The purpose of vacation time is to relax and enjoy yourself. Personally I find that life is more relaxing and enjoyable when I staying in control of my expenses and living below my means. I think you will too. Here are some step by step tips to make any vacation more enjoyable and affordable, starting with planning and throughout the days of your trip.  ,Planning: Of course the first step is to be realistic about what kind of vacation you can afford on your budget. If you have $2,000 to spend, you are not going on a six week trip around the world. But can you do something fun on a smaller budget? Absolutely!! Take a little time to think about your priorities? What is the best thing about vacation time for you? Sightseeing? Beach time? Activities? Relaxation? Time with the kids? You may not be able to do everything, but you should be able to hit a few of your priority choices. Half the fun of a vacation is actually in the planning stages. Talk about your vacation dreams with the people you will be vacationing with. Have fun with it! Which of them might you be able to actuate on your next vacation? While you’re at it, daydream about future vacations. There is great pleasure to be had in just the dreaming alone!  Accommodations: The time to book is as early as possible, again keeping your budget in mind. If you can’t afford a motel, camping might be the way to go. If you can’t afford to travel, keep it close to home. See if you can lock in a good deal as early as the summer before. Keep your eye out for specials. There are so many travel and discount websites now, you just have to go to your favorites and watch for them. If it is feasible, try to find something with a kitchen to save on meal expenses. Or you can try a house swap, or hostel. Don’t forget to check out Airbnb for some offbeat affordable options. If you are very flexible about where and when you go (retirees for instance) here is where you may be able to snag some great last-minute deals if you keep watching!  Transportation: Again, keeping the budget in mind. If money is tight this is not the year to be flying off somewhere. Keep it closer to home. If you have a little more leeway, then maybe this year you can take it further afield. Don’t feel you need to fly away to get away. Remember, some people are flying to wherever you live to “get away.” Again, starting at least 6 months out, keep your eye on the flights. When you see a good deal, book it. Don’t wait to see if there are last-minute specials. The airlines don’t really do that anymore and you may very well end up paying more for a last-minute flight. There are also apps and websites that will alert you to a drop in price, and some airlines will send you a refund for the difference. You can save some money by flying on any day except Friday or Sunday, the two most expensive days to fly. And also by booking at less than optimal times and flights that have layovers. Remember to watch for add-on expenses (checking in luggage, etc.) The best thing to do is learn to pack very light. One carry-on bag and you’re done. I’ve done this on several two week trips with no problem whatsoever. You don’t need a lot! You can wear things over and over with no dire consequences. If you are driving, remember to factor gas prices into your budget, also tolls and parking expenses. If you are renting a vehicle get the smallest (cheapest) vehicle you can make do with (it will also be more fuel efficient). It may be a good idea to just go with mass transit at your destination if you can.   Meals: Here, as I have alluded to earlier, the more you can avoid eating out the better. It’s great to have a place with a kitchen. But even if you don’t, always bring a cooler to keep stocked on meal options. Try to get a room that includes free breakfast. Eat up on that!! This way a light lunch will do. Keep things in your room for that. Sandwich bread, peanut butter (or other “fillings”), fruit, yogurt, cheese, crackers, nuts, etc. Don’t forget to bring your water bottle. Now you can eat in your room or take your lunch out on the road for a picnic wherever you go for the day. Dinner does not have to be a fancy affair every night. A quick deli meal or some tacos will do. Also remember to share meals if you go somewhere with big servings (or bring a “doggie bag” home for the next night’s dinner). And for the adults, try not to go out for “drinks” every night. You can have “cocktail hour” on your balcony sometimes, with a bottle of wine (or cocktail ingredients) brought from home (or purchased locally)  Activities: These can run the gamut, from those pricey theme park vacations or expensive activities to a (free) hike in the woods or making s’mores around the campfire. You should “limit” yourself to what your budget dictates. Why do I put limit in quotations? Because there are so many beautiful experiences you can have for free that I hardly think this is a limiting factor. It fact I might argue here that the best things in life are truly free! Get the local papers and look up free events in the area. Bring along (or rent) bikes, boats, balls, rackets, etc., etc. Bring board games for those rainy days. The things that bring joy to you and your family are the fun and pleasure of spending time together. You cannot buy relaxation or happiness.

If you can’t afford a vacation, you can’t afford a vacation, but you can still enjoy yourself and share good times and laughter with your family and friends. And whatever your vacation budget is you can still have a quality vacation and make memories to last a lifetime for you and your family. It’s all up to you!   This is the priority based budget. And it is a great tool to use to help you realize just what your priorities are and exactly where you want your money to go (and, maybe even more importantly, not to go). I could look at where your money is going and give you an idea of where you might be able to trim the fat and the things that I would not “waste” my money on, but at the end of the day it is your money to choose to spend as you will. Of course if you are looking to save money you cannot “choose” to keep spending on all the things you have been spending it on. This is where the priority based budget comes in as a tool to help you with that decision making process. The concept is very simple. You start with the most important things that you want your money to go for. And here we are not talking about the things you “want” the most. We are talking about your most basic needs. You also start with the amount of money you bring in for the month. As you list each expenditure you subtract that amount from your monthly income. So you would start with things like housing (rent or mortgage, and property taxes if applicable), food, electricity, water, heat, insurance, and then continue down the list to “lesser” but necessary to your life expenditures. And as you do this you continue to subtract from your monthly income. By the time you get to the bottom, depending on what your income is you should be getting to your “want” items in order of which things you want the most. When you get down to zero on the other side you are done. You can’t (or I guess I should say shouldn’t) spend money that is not coming in, because this is, of course, what leads to debt. Everyone has different priorities and what would be a frivolous expenditure in my eyes may be a very important source of joy and happiness for you. But the bottom line (zero) is the bottom line no matter what your circumstances are. You cannot go beyond that and this is what forces you to examine what your spending priorities are.  If your money is very tight, you may not even get past the “needs” at the top of the budget. There is no room for “wants” at all. If this is the case you will need to examine how you can increase your income. You can temporarily take on a second job, but you will also need to come up with a more permanent solution to your income dilemma. Can you ask for a raise? Look for a better job in your field? Should you try a different line of work? Get additional education? You need to come up with a plan of action, and start taking the necessary steps to get there. If you have debt, then paying that off should go right after your basic needs are met. If you do not have debt, then you are in a position to start saving and that savings should be at the top of your line items. Retirement savings being at the top, followed by other savings goals. i.e. a wedding, a house, kids (or your own) education, a car, vacation, home improvements, etc. This is the concept of “Pay yourself first” and it works! This way you have all your life goals covered by the time you get down to the bottom of the budget to those everyday “wants”. I have included some budget worksheets that you can use to create your own Priority Based Budget. One has categories to give you some guidelines (but feel free to change them according to your own priorities). And some samples to help you see how it's done: Sample 1. Sample 2. The other is left blank for you to fill in as you see fit. And more samples: Sample 3. Sample 4 The lefthand column of both of them is for you to start with your monthly income and then subtract as you make your way down your list of spending priorities until you get to zero at the bottom... money gone... budget done! You must of course (if you are sensible and want to get ahead with your money) include your saving goals as part of your monthly budget and also things that you will not necessarily spend money on every month, but that you will do so from time to time (like car or home repairs).  Once you finish with this exercise you will have a clear black and white picture of where your money is going according to your own life’s plan. You are on top of your money. You are in control. And that’s a pretty darn good feeling! Congratulations!   Living in such a materialistic society as we do, it can be hard to even detangle oneself from the mindset of constantly wanting and buying more and more stuff. We have been bombarded with ads from a very early age, from every possible media, telling us why we “need” this that and the other thing. We are told how each of these items will make our lives easier, fuller, more fun, etc., etc. Just the very act of “shopping” has become a leisure time activity in and of itself. We are trained to always want the bigger and better next thing. We compare ourselves to others based on if our stuff is as good, new, and shiny as theirs. We never reach the point of satisfaction because there is always that next best new thing coming out that we have to have, as evidenced by the lines for the newest model iPhone. Really??! Is it that much better than the previous model that you have to waste precious hours of your life waiting on line to have it a few hours (or even days or weeks) earlier than you would have been able to get it otherwise? To me, that represents the epitome of how deeply this materialistic mindset is entrenched in us.   And once we get that new thing, how long does the satisfied happy feeling last? Not long apparently as evidenced by all the stuff put out at garage sales (many with tags still on), not to mention Craigslist, eBay, and even worse, into the ever-growing landfills. It is the thrill of the acquisition that is being sought. Once we actually own the thing the joy fades pretty quickly. This just sets us up for wanting more to experience that “high of the buy” once again. As you can see with this type of scenario one can never be truly satisfied and happy. Would you like to get off this unsatisfying and frustrating carousel? I know I do and I make a very concentrated effort in my life to buck the system. It can be hard to do when you are literally surrounded by it, but the better you get at recognizing the pattern and fighting to control being sucked in by it, the happier (not to mention less stressed and richer) you can be. It is when you get out of the “more and better stuff” mindset you truly start to appreciate the things that you have. And ironically the less stuff you have the more you appreciate it. And even more ironically the less you pay for each item the more you appreciate it. I take great satisfaction in having acquired an item for free or very inexpensively that has given me much use or added beauty to my life. The less I spend on something the more I appreciate it, because not only do I appreciate the thing itself, I am also appreciative that it did not take my hard earned money away from me. This can be especially true of items that we tend to collect a lot of, such as clothes. It feels much better to have a few shirts that you really like and enjoy wearing than to have your closets and drawers stuffed with them, many of which you don’t even wear. And if you spent a lot of money on those shirts that you don’t even wear that can make you feel worse. As they say, “Less is more”. It really is true! I take great pleasure in buying a shirt that I really like at a thrift shop for a few bucks (or even better if someone has given it to me for free) and I feel that pleasure each time I wear the shirt. The fact that our world is bombarded with stuff and we can go out to stores filled with it and buy, buy, buy, and now even at home we are bombarded with the urge to buy, buy, buy on our computers leaves us in a state of wanting constant instant gratification. All we have to do is have a thought of wanting something and it can be ours at the swipe of a credit card or click of a button. But has this made us any happier? I would venture to say no. What it has done is deprive us of the joy of waiting for our pleasure. For it is in that anticipation of pleasure that our excitement builds up. If we have to wait for something, then we appreciate it so much more when we finally do get it. Instant gratification has effectively deprived us of that very pleasure. Some people think of trying to live below their means as a painful way to live. They view it as deprivation. But it is all in the mindset of how you approach it. I find that living below my means gives me more pleasure than living the life of constant instant gratification through buying more and more stuff. It is a less stressful, slower, more satisfying way to live. It allows you to savor pleasure more deeply rather than to be constantly looking to acquire the next best thing. I urge you to give the joy of slow acquisition a try. You will be surprised how much pleasure not spending money can bring you. Your life will be less stressful, more peaceful and richer than ever before, I promise!   Did you spring clean your finances? Were you able to take a good look at your expenditures and trim some of the fat out of your monthly expenses? If you have done this successfully, I bet you are feeling pretty light right now. In fact, you are probably walking around with a spring in your step! It’s amazing how good lightening up your budget can make you feel! Before people start on this process they actually tend to think that putting themselves on a tighter budget will make them feel weighed down and restricted, but once they get started they realize that it actually has quite the opposite effect. And once you have pushed past those first steps, you will find not only does it feel surprisingly good, but it gets easier. And not only does it get easier, but you get better at it. That frugal muscle begins to awaken and gain strength. And, by golly, not only is saving money not a chore, but it begins to become fun! You will start to examine each expenditure in a new light. You will find yourself looking for more ways to save. How can you cut back even further? Once you come out of that fog or never-ending consumerism your brain chemistry will begin to change. You will no longer take your satisfaction from acquiring more and more stuff and making all those daily instant pleasure purchases, but rather in the feeling of pride and contentment that you are living a full life without needing to spend money like that. As you gain control over your finances, get out from under that heavy debt, and begin to see your savings grow, you will delight in the peace of mind that your new frugal lifestyle has brought you. “Stuff” is no match for this joyful feeling of gratification. This will strengthen your resolve to save even more. Once you get the “snowball” going in the right direction there’s no stopping you! Who wants to go back to being buried under that avalanche of debt and stress.? You are free! Now you will stop and think about each purchase with what I call the Super Sliding Scale of Savings. It goes something like this:

The more times you can make it all the way to step 6, the better off you will be and the happier and more content you will become. So keep on flexing that frugal muscle! You will continue to grow stronger financially and lighter in your outlook and step. Here’s to financial fitness!  |

Archives

June 2022

Categories

All

|

RSS Feed

RSS Feed