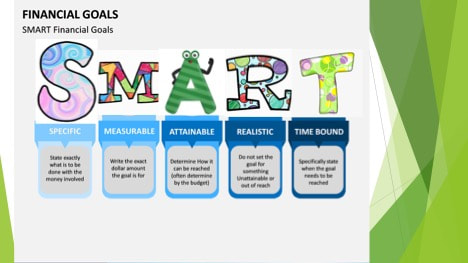

January is, of course, traditionally the time when we make resolutions, and unfortunately the time we also traditionally break them. Why is that? Well …change is hard. We are ultimately creatures of habit and a resolution by its very nature requires change. And we would much prefer going along in our daily lives doing the same things in the same ways as we have always done them. So, regrettably our resolutions go by the wayside … and life goes on… and we feel bad.  Instead of setting resolutions this year, how about setting some goals for yourself? “What’s the difference?” I can hear you asking. While a resolution tends to be somewhat vague (“I want to lose weight”), if you are setting them the proper way, a goal is more specific. And to help you make them specific the genius gurus that be, have come up with this cute little moniker: S.M.A.R.T.  So, taking the example of losing weight, we would say that I want to lose 20 pounds (specific) by April (time bound) and I will do this by losing 2 pounds per week (measurable). This goal would be both attainable and realistic. Saying you wanted to lose 100 pounds by April would be very unrealistic. And setting the mini goal (of two pounds per week) makes it easier to work towards. You can now just concentrate on those two pounds per week, rather than the bigger (more daunting) 20 pounds by April. You can even set up a reward system for yourself every week if you make your 2 pound goal (get a message, your nails done, watch your favorite movie, whatever…)  Now, let’s translate this into a money goal. Rather than a vague “I want to save more money this year”, try “I want to save $2,000 by the end of the year”. Now you can break this down into how much you would need to save each month ($167), and per week ($38), and even per day ($5.48). Once broken down this way, it is easily manageable. What can you give up that is currently costing you $5.48 per day, or $38 per week? And much easier to monitor your progress. You can easily see if you are on track. It is helpful to make a chart for yourself.  To be even more specific make a plan for where you are going to put this saved money (perhaps open up a separate savings account for it). And it should be earmarked for a specific purpose (a vacation, new furniture, a new computer…). Or it can be an account that you will continue to add $2,000 (or more) into each year going forward (toward your emergency fund, or a house, or a car…). Now you are not just making vague resolutions, you are setting goals the SMART way. It is a specific amount (broken down into even more specific “mini” goals), it is realistic and attainable, and certainly measurable. And you can continue to manage your progress throughout the year (and give yourself little mini rewards if you need them).  When you set your goals in this very definitive way, you are now shooting towards something very precise, and keeping that goal in mind it is now easier to “give up” whatever you need to do in order to achieve your goal. You are not just making your own coffee in the morning to “save money”, you are saving up for that computer, or furniture, or car or house. It gives you more of an incentive to make the sacrifice. (In the weight loss scenario given earlier, it makes it easier to give up that one of two things that are contributing to your weight gain and swap them out for healthier options, just to make that 2 pounds weight loss for the week).   So try setting yourself some S.M.A.R.T goals this year instead of those nebulous resolutions and see if you don’t stick to them this time around.  Best of luck to you for a bright and prosperous New Year!

0 Comments

I am so excited to welcome you to my new webpage and get started on a money saving journey with my readers. This blog will be chock full of tips and strategies each month that you can use to set and achieve any and all of your financial goals from the short term to long term to the ultimate of a secure, happy, well-funded retirement and even a legacy to leave to your heirs. The new year is traditionally a time of getting started so this is the perfect time to take a look at where you stand right now with your finances and what goals you would like to achieve this year and beyond. No matter where you are at present the best time to get started on improving your financial status is right now! Before you can begin to set goals it is important to know where you are right now. Set aside some time to take a look at where your money is going. Write out an expense sheet. Include all your expenses big and small, from your fixed expenses (rent/mortgage, insurance, cable, phone, etc.) to your more variable expenses (food, heat, gas, clothing, entertainment, etc.). And don’t forget the occasional expenses (school supplies, Christmas, vacations, car repairs, etc.), as well as all those little expenses that you hardly think about (your morning coffee to-go, vending machine treats, lunches out, beauty products, etc.). If you are not in the habit of noting all your expenses, it may take some time to remember them all. I suggest getting a little notebook to record what you spend money on each day at least for a month. (Even I still do this on a daily basis.) You can use this worksheet I've made to complete this step.  In the meantime, take stock of any debt you have. Write down all of your debts including the full amount owed and the interest rates. Add them up to get your total owed. If you have assets, good for you! Take note of them too. Money in the bank? 401k (403b)?, Any investments? And write down what your income is, including all sources; Your (and your spouse’s) salary, child support, SS payments, rental income, extra side jobs, etc. Now that you have a clear picture of where you stand, you can plan your goals. Let me give you a little hint here. Your first goal should be to pay those debts down! No debts? Great! Is there something you want to save up for to buy this year? Do you have a bigger purchase in mind that might take a few years to save up for? (a new car or down payment on a house?) Do you want to save up for education? (yours or your kids). And then of course there is the ultimate goal, that nice comfortable retirement nest-egg! For the smaller goals it is simply a matter of dividing the total needed by the months you have until you need the money. Then you know the exact amount you need to put away each month to achieve it. For that ultimate big retirement reward, slow and steady wins the race. The earlier you start the better off you will be. This should be an automatic amount taken right off the top, before you even see it. Of course a job 401k will do this for you, but if you don’t have access to one you can set up your own retirement account and have automatic deductions going straight into it from your checking or savings account each month. I know this is a lot to contemplate all at once, but for now just take this month to take stock of your expenses and debts, and think about what goals you might have for your money and I will lead you through the rest of it step by step as the year progresses. When you do it step by step you will see how easy it can actually be to turn your finances around. We will start to talk next month about just how to budget your expenses and find the money to put aside for all those goals. ` Stick with me and you too can have a bright future!  |

Archives

June 2022

Categories

All

|

RSS Feed

RSS Feed