|

Drinks:  1. Coffee. It is so much cheaper to brew it at home  1. Water. After drinking water from a tap for much of my formative years, I was gobsmacked when the beverage companies convinced a whole society of people that they should pay for it in a bottle. That was quite a feat of marketing as far as I’m concerned. Guess what folks, it’s still available from your kitchen sink! Get a reusable bottle for when you go out.  1. Soft drinks. Terrible for your teeth and your health and your waistline.  1. Fruit drinks. Might seem like they are healthier than soda but they really aren’t. It is still a sugary liquid. Even the ones made from “100% fruit juice” are just the sugar of the fruit without the benefits of all the fiber that you would be getting from eating that actual fruit. Eat the fruit!  1. Tea. I do drink tea on a daily basis, but made from my own tea bags at home, or sometimes even from herbs (lemon herb) from my garden. And (don’t get all judgy now) I reuse the teabags several times before I am done with them.  Alcoholic beverages. Rather than going to happy hour and spending upwards of $5 per drink (often way upwards), buy the ingredients and have a cocktail hour at each other’s houses. It is way cheaper and just as fun. When you go out to dinner if you must have a drink, at least limit yourself to one.I only drink water (and tea)… from my kitchen tap. It’s free and it’s much healthier.  Oh, well, full disclosure (I am human), I do enjoy an occasional cocktail… at home, or at a friend's house. And, yes I do often order a drink on the (rare) occasion that I go out to dinner (but never more than one). I have never really added it up, but I’m sure I’ve saved a ton of money just by not buying drinks over the course of my lifetime. And I don’t feel like I “missed out” on a thing by living this way. Try it. You may be surprised by how much money you can save with just this one change in your spending habits!  Here's to a bright future!

0 Comments

I know I am dating myself here, but back when I was a wee lass, Halloween was a simple holiday, simply for kids. And when I say simple I mean that a few weeks before October 31st, we kids, (not our parents) would start thinking about what we wanted to dress up as for Halloween. Then we would scrounge our closets and other parts of the house for things we could use to accomplish our goal. There were usually things like cardboard boxes, tin foil, old clothes of our parents, yarn, fabric scraps and other such items involved. If our parents went all out and bought us a costume, it would be this thing that came in a 12” x 12” box consisting of a flimsy cover-up with a picture on it to represent what we were supposed to be and a cheap mask with a rubber band in the back to hold it on, like this:   These are way more ambitious homemade costumes than we ever came up with. LOL! Very clever! On Halloween day itself we would rush home from school, put our costume on and head out with an old sheet or grocery bag to go around the neighborhood trick or treating. We would be home by dinner to review, organize, and trade our loot and that was it. Halloween over. As for decorations, maybe we would have a few cardboard cutouts of pumpkins, or bats, or ghosts, that we would tape on to our door or windows. And these we saved and used year after year. Oh, and the adults did not celebrate at all. They were not really involved other than to help us with our costume, if we asked, and buy and give out the candy for the trick-or-treaters. Fast forward to today and it (like almost every other holiday, and so many things in our society) has become a multibillion dollar industry that goes on for an entire season.  Now I know I am sounding rather curmudgeonly here and don’t get me wrong I am not against people having fun for Halloween, adults included. I am just saying that if you are in debt, or not saving enough, it would be prudent on your part to reign in the holiday spending. Even my own (frugal) family has gotten into the spirit. When my kids were little we began hosting a spooky bonfire party each year at this time, adults included, which even though my kids are all adults now, we still often continue to this day. As I said we held our annual Halloween event, but I never went crazy with the spending. Since I knew it would be happening I kept it in mind all year long when I was shopping at yard sales and thrift shops. And I would take a look for clearance sales in the stores in the days after Halloween. And, of course, I would save things and use them year after year. I would also pad the decorations with things I had around the house, such as many candles in jars. Even Christmas lights can work for a spooky effect. I would recycle old halloween costumes into creepy scarecrows strategically placed around the yard. My kids would often put together a haunted house or trail, also cleverly using whatever household things they could find. For instance, one year “Dr. Ner’do well’s” lab contained body parts in jars, A cauliflower for the brain, grapes for eyeballs, chicken bones for fingers, etc.    We also invited everyone to come prepared with their favorite scary story to tell as we sat around the fire. Free frights and chills for everyone!  So I think you can see what I’m getting at here. I don’t think we will ever be getting back to that simple sweet Halloween of my childhood years but there are still many ways to get into the spirit and have tons of spooky holiday fun, adults included, without giving up your hard earned money. A little imagination can go a long way towards making your piggy bank happy and still making your Halloween spooktacular!  The author and a friend in our homemade costumes at last years bonfire party.  Happy Frugal Halloween!

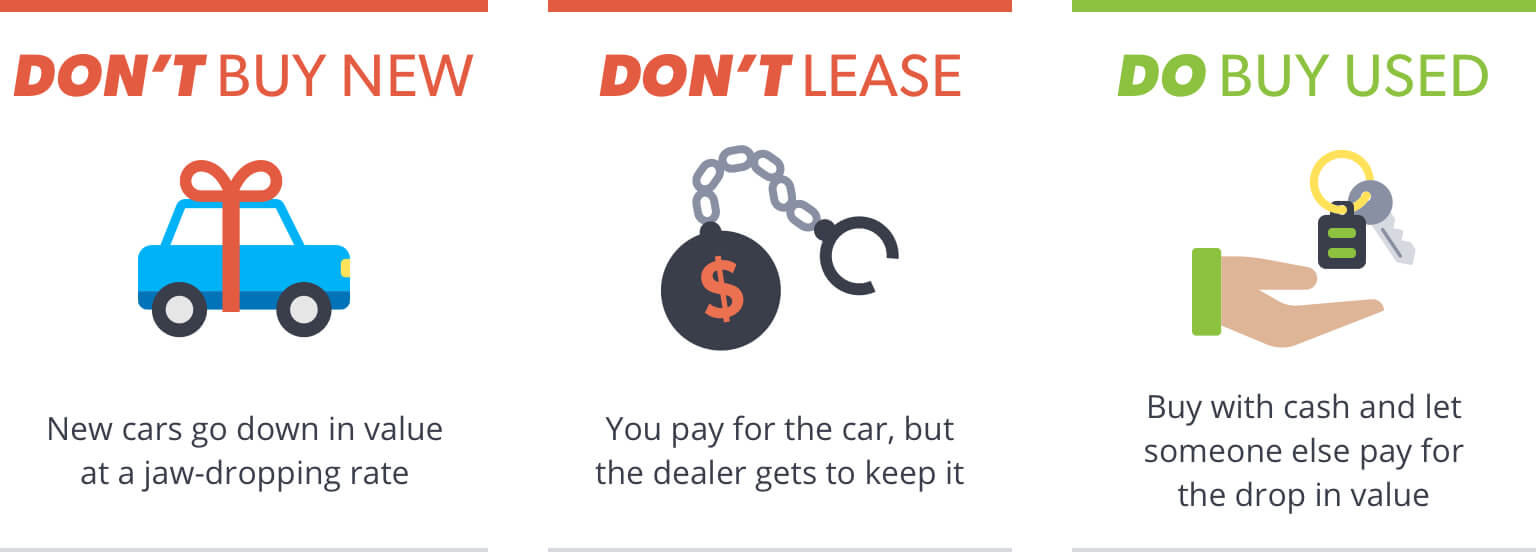

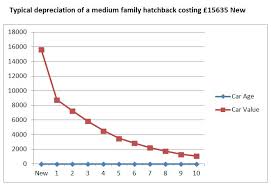

Since I am currently in the market for a “new” car, I thought I would share with you how I do not nor have I ever had a car loan. It’s quite simple if you start from the beginning but wherever you are in your auto ownership journey you can start at this moment and work your way up and out of car loans for good.  What’s wrong with car loans you say… isn’t financing a car the “American way"? Who doesn’t have a car loan? Well I don’t, for one, and I would wager a guess that every “Millionaire Next Door” doesn’t either. And yes, you’re right it has become the “American way” but which Americans are benefiting from that? Hint: It’s not you, the proud recipient of the car loan. It is the almighty bank (or sometimes the car dealerships) that are winning in this drive-now, pay-later arrangement. And the amazing thing is that they have you hoodwinked into believing that they are doing you a favor by getting you into the best car they can for low money down and easy monthly payments. Wow! What a nice guy… NOT! Believe me, car dealers are not in the business of doing you a favor. The only thing they are interested in is their own bottom line. The biggest best car they can sell you lines their own pockets, and getting you to take a loan from them (instead of the bank) is just more icing on the cake. And if you have ever been car shopping lately you will notice that they (subtly or maybe not so subtly) will start touting the glories of leasing a car. This is like taking a car loan on steroids (for them). Think about it. You pay a down payment (maybe $1,000) and then “easy” monthly payments of $299/month, and at the end of the three-year lease you are out $11,764 and you own absolutely nothing! You can now either give the car back and start all over again or pay some exorbitant fee (on top of the almost $12,000 you’ve already paid) to now own the car. You could have bought a (used) car for $11,764 three years ago and still had plenty of life left to it for years to come. And if you financed your car, let’s look at one example of how much you are actually paying for that car by the end of the loan period: If you take out a loan for $25,000 at 4.5% for a 60-month term, your monthly payments will be $570 and at the end of the term you would have paid out $27,364. A total of $2,364 lining the pockets of whoever held your loan. Nice! … For them. How do you feel about giving them all that “free” money? Would you like an extra two thousand in your bank account? But, you tell me, “I don’t have the money to just purchase a car outright.” Well, I can tell you that on a modest income I have never taken out a car loan to buy a car. How did I do it? Well, I bought my very first car for cash and from that point forward I was saving the money (that most people are paying out for car loans) to purchase my next car for cash. Most of the cars were used, at least a few years old, but I did make the mistake of purchasing two of them brand new (all for cash). No loans. If you can afford car payments you can afford to save up for a car!  Now I have instructed my kids to follow my principles. They each saved up for their first car (with a little help from me at times) and bought them (used) for cash. Then I told them to pretend (like many of their peers) that they have car payments, but pay them to themselves. And now through the magic of online bank accounts it was easy for them to set up a “car account” with $200 or $300 a month being automatically deposited into it from their checking account. And with that very modest “car payment,” if they take good care of the cars they have, in 10 years-time they will have between $24,000 and $36,000 towards the (cash) purchase of their next car. And even more than that, really, because instead of paying interest to a car loan, they are making interest on their bank account. It may be only 2% at the moment, but it sure beats paying out at 4% or more! But if you haven’t done that from the beginning and you are currently saddled with a car loan, then the best thing you can do is keep the car after your loan is up for as long as you can, and here’s the important thing: Keep paying those monthly car payments but pay them to yourself so that when you are ready for your next car you will have a chunk of change sitting there for your purchase.  And why do I say I made the “mistake” of buying a few of my cars brand new? Because the depreciation curve is enormous in the first year or two of car ownership and the bulk of that depreciation takes place in the first 5 minutes of car ownership. The minute you drive that sparkly new car off the lot you have dropped a couple of thou off its resale value. Ouch!! Let someone else take that depreciation (thanks first car owner!). Save yourself a couple of thousand dollars and buy a car that’s at least a year or two old.  So, now I will head out to the dealerships. You can buy a car from an individual for less money, but I like the assurance of having the dealer in case something goes wonky with the car a short time after I buy it. And even though I am paying cash I will still keep in mind that (friendly as they are) the dealer is not my friend. I will do my homework and check out any cars I am considering online, for any issues and the prevailing price for that year’s model. You can try Kelly Blue Book or Edmunds for this info. Then I am prepared to bargain (with the mysterious “manager” in the back, that my dealer will be consulting). I may walk away from the deal two or three times before I am satisfied that I am getting a rock bottom price. Of course the dealer has to make some money on the deal. I don’t begrudge him that. I just want to feel that I got a fair deal. Wish me luck as I head out in search of my next set of wheels and I hope you too will someday enjoy the joys of owning your own set of wheels without those pesky loans dragging you down.   Ah Amore! The month of love. Hallmark, Brachs, Godiva, florists, and all fine jewelry stores, even those romantic getaways and restaurants are eagerly awaiting it! How much do you love your sweetie? Open up your wallet and show them! The ads make it abundantly clear. As James Taylor crooned, “Shower the people you love with love. Show them the way that you feel.” In our society of commercialism, stuff and abundance, it’s just another occasion to sucker you in to buy even more. This one carries a particular guilt trip. If you love your honey how can you not show them through valuable merchandise? What kind of a heartless cad are you?  And, of course, Hallmark, et al, went beyond just your particular heartthrob to include the whole dang family in the celebration. From the kiddies all exchanging valentines in school (which, through the years, went from homemade hearts to purchased cards to candy and treats), to cards and gifts made for every one of your beloved family members. Don’t leave anyone out! And just a card (which now can run upwards of $7)? No way! What about the candy? The flowers? The stuffed animals? The jewelry? Showing everyone in your family that you love them can run a pretty good chunk of change! So … my challenge to you is this: Why do we have to spend all this money (mostly on crap that will someday become part of the landfill) to “prove” to our families that we love them? Just because Hallmark told us to? Because companies want to make money selling us their products?  Where does it all end? It escalates year after year, holiday after holiday. The only place it can end is with you and me. We must all realize that how much you spend on a person does not equal how much you love them, especially when what you spend on them is for meaningless junk. If you are married or in a committed relationship with someone, you should be working together to make the most of your money, live below your means and save. Work together to make the holiday special. Make a special meal together, go on a sunset stroll somewhere, watch a romantic movie at home (free from the library!) Surprise your spouse with a heart-shaped cake you baked. A heartfelt letter written to them about how much you love them and why would certainly be more appreciated than something some greeting card writer came up with.    And as for the kiddos, yes you can shower them with gifts. In fact, you can shower them with gifts for all of the many Hallmark gift giving occasions that have sprung up throughout the calendar year, but what exactly are you teaching them? What are you creating? Perhaps you might want to think about what kind of adults you would like to raise them to be. What kind of expectations are you setting up for them? If you really feel you must note the occasion, how about making some heart shaped cookies and having fun frosting them together? Keep it simple. Resist the impulse to go overboard. That impulse is what got us into this overspending mode in the first place.  Yes, Amore! Love is a many splendored thing. We should tell our love ones that we love them, not just in February but always. And finding special ways to show them that we love them is a very sweet thing to do. Little love notes and special surprises are always cherished and appreciated, and go a long way towards keeping the love alive. But the danger comes in equating how much we spend, especially on things dictated to us by outside forces and advertising, with how much we love them. Make love, not debt!   Tis the season …for exuberance, generosity and joyful abandonment. It’s so very festive and fun, but oh so easy to get carried away with it all. And temptations to spend are everywhere you look. Deep discounts! Drastically reduced! Prices slashed! The more you buy the more you save! …. Or do you? It certainly doesn’t seem like it when the bills roll in come January … right around the time when you’re making those New Year’s resolutions, it seems. You know, the ones about getting on a budget and stopping the overspending? So, what are some strategies that you can employ to obtain that simple peaceful holiday season and reign in the excess spending? The first thing you can do is pare down those lists. Of people to buy for, indulgences, activities, and, of course, presents to buy. Well, now is the time to stop and think about that. Take a deep breath, have a cup of tea and sit down and contemplate a quieter, simpler, less hectic holiday season. One that you won’t regret when the new year rolls around. One that you’re not paying for until next August. Does that thought bring you joy? Do you feel your blood pressure dropping already?  Sometimes the amount of people we exchange with can become out of hand. What starts out as a nice gesture one year, exchanging with this friend or that relative eventually morphs into a yearly obligation. You may be surprised to find that the other person in this exchange feels the same way and is more than happy to drop the yearly gift swap. Talk to them. Often we also have auxiliary people in our lives to favor with a gift, from teachers to work-related people to babysitters and hairdressers, etc. Many times these people are also swamped with all those many little gifts at holiday time, and though the thought is appreciated they would rather not deal with the deluge. Sometimes a kind and heartfelt note of appreciation is most welcome. If you feel you must give something, make up a big batch of your holiday specialty (cookies, candy, fudge, whatever) and parcel a little out to each of the people in your life that you need to thank. One and done. And edibles are often more appreciated than extra objects to clutter up their lives. Besides paring down the list of people that you exchange with, it is also a good idea to pare down the amount of gifts exchanged. This especially applies our beloved and cherished little offspring. I know it can be so fun to spoil them and see their happy faces when they open that pile of gifts, but is it worth going into debt for? And is it really good for them in the grand scheme of things?  ‘ Have you ever noticed that the more gifts children get the less they are actually appreciated? If they open, open, open more and more gifts the presents themselves become secondary to the act of tearing into the innumerable presents. Is this greedy abandonment really the kind of “happiness” you want for your child? Just a few thoughtful gifts might instill a more genuine thankfulness in your child. My last gift giving tip comes too late for this Christmas, but is certainly something you can start for next Christmas. That is to prepare for the holidays all year, both in your spending and your buying. The old fashioned “envelope system” works great here. Just deposit a little bit out of each paycheck and let that be your holiday budget for next year. Pay cash for your presents and other holiday expenses, and when the money’s gone it’s gone. No more spending. And no credit card bills to fret over in January. You can also spread out your buying for the entire year. Look for those after-Christmas sales. Take advantage of clearance sales throughput the year. And one of my favorites, yard sales and thrift shops. I used to pick up gifts for my kids (often still in the box or with tags on) all summer at yard sales and my Christmas shopping was almost done (for dirt cheap) by October except for a few requested items to round out the list. This works especially well with smaller kids who are not as particular as older kids can get. You can sometimes score presents for the adults on your list this way too (keep them in mind when you look around). So, yes, Virginia (or whatever your name is), you can have a joyous holiday season without going into debt for it. In fact, I might venture to say that you can have an even more joyous and peaceful holiday when you keep it simple and take this time to relax and enjoy yourself with your family and friends without all that frenzied spending. Give it a try. You have nothing to lose and lots to gain! Wishing you all a warm and wonderful holiday and a peaceful and prosperous new year!   Living in such a materialistic society as we do, it can be hard to even detangle oneself from the mindset of constantly wanting and buying more and more stuff. We have been bombarded with ads from a very early age, from every possible media, telling us why we “need” this that and the other thing. We are told how each of these items will make our lives easier, fuller, more fun, etc., etc. Just the very act of “shopping” has become a leisure time activity in and of itself. We are trained to always want the bigger and better next thing. We compare ourselves to others based on if our stuff is as good, new, and shiny as theirs. We never reach the point of satisfaction because there is always that next best new thing coming out that we have to have, as evidenced by the lines for the newest model iPhone. Really??! Is it that much better than the previous model that you have to waste precious hours of your life waiting on line to have it a few hours (or even days or weeks) earlier than you would have been able to get it otherwise? To me, that represents the epitome of how deeply this materialistic mindset is entrenched in us.   And once we get that new thing, how long does the satisfied happy feeling last? Not long apparently as evidenced by all the stuff put out at garage sales (many with tags still on), not to mention Craigslist, eBay, and even worse, into the ever-growing landfills. It is the thrill of the acquisition that is being sought. Once we actually own the thing the joy fades pretty quickly. This just sets us up for wanting more to experience that “high of the buy” once again. As you can see with this type of scenario one can never be truly satisfied and happy. Would you like to get off this unsatisfying and frustrating carousel? I know I do and I make a very concentrated effort in my life to buck the system. It can be hard to do when you are literally surrounded by it, but the better you get at recognizing the pattern and fighting to control being sucked in by it, the happier (not to mention less stressed and richer) you can be. It is when you get out of the “more and better stuff” mindset you truly start to appreciate the things that you have. And ironically the less stuff you have the more you appreciate it. And even more ironically the less you pay for each item the more you appreciate it. I take great satisfaction in having acquired an item for free or very inexpensively that has given me much use or added beauty to my life. The less I spend on something the more I appreciate it, because not only do I appreciate the thing itself, I am also appreciative that it did not take my hard earned money away from me. This can be especially true of items that we tend to collect a lot of, such as clothes. It feels much better to have a few shirts that you really like and enjoy wearing than to have your closets and drawers stuffed with them, many of which you don’t even wear. And if you spent a lot of money on those shirts that you don’t even wear that can make you feel worse. As they say, “Less is more”. It really is true! I take great pleasure in buying a shirt that I really like at a thrift shop for a few bucks (or even better if someone has given it to me for free) and I feel that pleasure each time I wear the shirt. The fact that our world is bombarded with stuff and we can go out to stores filled with it and buy, buy, buy, and now even at home we are bombarded with the urge to buy, buy, buy on our computers leaves us in a state of wanting constant instant gratification. All we have to do is have a thought of wanting something and it can be ours at the swipe of a credit card or click of a button. But has this made us any happier? I would venture to say no. What it has done is deprive us of the joy of waiting for our pleasure. For it is in that anticipation of pleasure that our excitement builds up. If we have to wait for something, then we appreciate it so much more when we finally do get it. Instant gratification has effectively deprived us of that very pleasure. Some people think of trying to live below their means as a painful way to live. They view it as deprivation. But it is all in the mindset of how you approach it. I find that living below my means gives me more pleasure than living the life of constant instant gratification through buying more and more stuff. It is a less stressful, slower, more satisfying way to live. It allows you to savor pleasure more deeply rather than to be constantly looking to acquire the next best thing. I urge you to give the joy of slow acquisition a try. You will be surprised how much pleasure not spending money can bring you. Your life will be less stressful, more peaceful and richer than ever before, I promise!   In January and February, we talked about getting organized with your expenses and setting some financial goals for yourself. I discussed the importance of keeping track of your expenses and setting up a monthly budget. Hopefully, you are now getting a better idea of where your money is going and are starting to feel more on top of your financial life. Perhaps this has lead you to make some changes in what you are spending your money on and how much is going out each month. If that is the case, good for you, you are on your way!  Now that winter is over and you are feeling more energetic and ready to give your house a good cleaning and get out there and clean up your yard to make way for the beautiful spring growth and flowers, you can also do some spring cleaning of your finances. Just as you declutter your house of unwanted extra stuff for a more peaceful environment and clean up all that yard debris for a tidier look, you can also take a look at your finances to clear out those unnecessary expenses that are keeping you from reaching your savings goals and from the peace of mind of living below your means. Once you are organized and are keeping track of your expenses, then you can begin to go over them with a fine tooth comb and start eliminating the financial clutter. Simplify your spending! There are probably at least a few things that you have gotten into the habit of buying that you can do without. And there are probably a few things that you are spending more money on than is necessary. How quickly or gradually you go about this financial downsizing is entirely up to you. Maybe you are the type that likes to get used to things slowly, and form new habits one at a time before making the next change, or maybe you like to see the rapid results of all that “found” money you can have (to pay off debts or start saving money more quickly) when you really pare down your budget all at once. Proceed at your own style and pace. Eliminating a few (or more than a few) daily or weekly expenses can really add up to big savings. Here are a few examples of how small savings can add up:  But don’t overlook those big (typically monthly) expenses too. Take a look at your phone plan, your utility usage and company, TV and internet providers, car/homeowners insurance. Shop around to see if you can get a better deal. Sometimes all it takes is the threat of moving on to spur your present company to offer you a sweeter deal. Even think about your mortgage or rent payments. Can you downsize? Refinance? Get a roommate? Once you eliminate a lot of that spending clutter your psyche will feel lighter, and your wallet and bank account will now be able to grow and thrive like those beautiful spring flowers. It’s a good deal all around. Give it a try!   If you are of a normal weight like I am, people will sometimes say to you “Oh, you are so lucky you don’t have to worry about your weight.” Or even more erroneously, “You are so lucky you can eat whatever you want.” Neither of these statements can be further from the truth. In fact, the only reason I am a normal weight is because I do worry about my weight, every day. And I do watch what I eat, every meal. It is just as much a struggle for me as for them. In fact, probably more so, given the fact that I am only 4’10” making every calorie count!

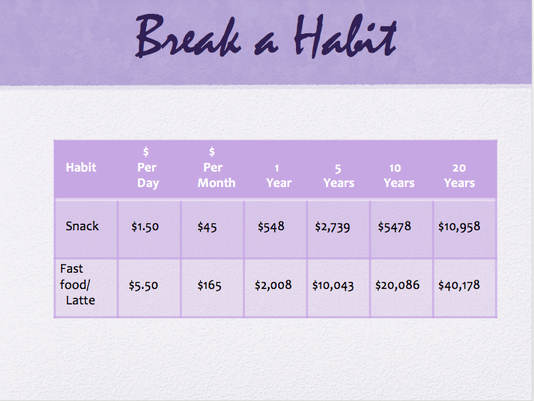

So what does that have to do with money, you ask? Well, I have also had people say to me, "Oh you are lucky that you were able to stay home with your kids and did not have to go out and work." And once again, luck had very little to do with it. Many of the women who said this to me had husbands who were making more money than mine did. These women also had cable TV, big new SUV’s or minivans, new clothes and shoes, maybe a Coach bag, and (back in the day when I had dial-up) high-speed internet. I would wager a bet that they also thought nothing of going out to lunch, buying coffee and drinks out, getting their nails and hair done, and picking up take-out for dinner. And yes, before you start yelling at me, I know there are single moms or other circumstances when women need to work, but my point is that often what people perceive as luck may actually be a result of the many choices made every day in life. Luck can also be a matter of perception in another way. Let’s say you get in a car accident and break your arm. Are you lucky or unlucky? Well, some might say of course you are unlucky! You got into a car accident and broke your arm for goodness sake! How can that be lucky? But then there is the person who says, “I am so lucky that all I got was a broken arm! I am still alive!!” Same scenario. Completely different perspective. So what is luck then? It is a matter of the results of your actions, and a matter of perception. So, the question is can you create your own “luck”? You absolutely can! Let me create a little story for you to illustrate my point even further: Let’s say Dick and Jane make the exact same amount of money. OK, scratch that, since Dick probably makes more. Let’s say Dixie and Jane make the exact same amount of money and through some cosmic fate have the exact same bills and expenditures every month. Each is able to save up exactly $100 per month after everything is paid, giving them each an extra $1,200 per year. At the end of Year One, Dixie takes that money and goes on a much-deserved vacation. Jane puts it in a one-year CD. At the end of Year Two, Dixie needs some new living room furniture, so she spends her $1,000 on that plus $200 on a hot new outfit. Jane now has $2,424 (her yearly savings of $1,200 plus $1,242 in her CD). She puts $2,200 of it into another CD, and spends $30 on a water filter for her tap, so she can stop buying bottled water, and spends $70 on an indoor antenna for her TV and cancels her $110 per month cable service. With the remaining $124 she has a great time at the thrift shop buying a new wardrobe for the coming year. Year Three: Dixie has her usual $1,200 at the end of the year. She splurges on buying herself the latest iPhone, which is just out, plus a nice case for it. Jane now has $2,244 from her CD, plus $350 saved by not buying bottled water, plus $1,320 saved by not paying for cable every month, plus her usual $1,200 for the year. A total of $5144. She spends $800 buying a washer and dryer so that she can stop going to the laundromat. She decides to invest the remaining $4,344 into a low-cost index mutual fund. At the end of Year Four, Dixie has her usual $1,200. Jane has her usual $1,200 plus $350 saved on water, plus $1320 saved on cable, plus $180 saved on laundry. And her mutual fund did pretty well to earn her 8%, so she now has $4,691 in that for a total of $7,741 … I could go on and on, but I hope you are starting to get the picture. One night Dixie meets Jane at a party. When the topic turns to finances, Jane happens to mention that she currently has about $3,000 in her savings account plus a mutual fund with over $4,500. Dixie is impressed and amazed and comments on how “lucky” Jane is to be so far ahead of her, while she, herself struggles living paycheck to paycheck. Does this sound familiar? Is Jane “lucky”? So how about starting to turn your own “luck” around. And one day in the future maybe you will chuckle inwardly when someone at a party tells you how lucky you are to have such a nice healthy nest-egg for your retirement and a nice bright future to look forward to.  Welcome back! I hope you have been working diligently at paying attention and keeping a record of your daily expenses. Have you had any surprises? Were there things that you found yourself spending money on that you never even gave a thought to? It’s all these little dribs and drabs of money sifting through your fingers that add up. It doesn’t seem like a lot when you are buying one little thing at a time, but when you tally it all up at the end of the month and multiply that by 12 for what you are spending on all these frivolities per year .... Yikes! In this day and age, it is often not actual money that we are parting with. Most people today have become even one more step removed from their spending awareness. Just pull a little piece of plastic out of your wallet, plunk it down and, voila, you have whatever you want. It barely seems that you’ve “lost” a thing. It’s just so easy to be unaware of how much is going out. This first step in stemming the constant flow of too much money going out is to become mindful of your daily spending habits and just where your money is going. If you have done your “homework” from my January blog, then you now have a better idea of that. The next step is to write yourself a budget. This is where you can begin to trim some of that fat. Do you really want to keep spending all that money or are there some things you can forgo in the interest of saving money? Once you have a clear picture of where your money is going and how much you no longer want to spend (aka waste), you can allocate a certain amount to each line item of spending every month. Now you will have an accurate outline in black and white of where your money is going (and where you don’t want it to go!) Here is a budget form that I created to help you plug your expenses into as many categories as I could think of. I have also left some spaces for those that you may have that I haven’t come up with. Now I would like to introduce you to an old timey but timeless way to keep your spending in line and on budget each month. It is based on going back to using good old American cash money for your daily expenses. This is what I did throughout most of my years of raising my family. I did not know it at the time, but since the magic of the internet I have learned that other people do this too and they call it quite simply and accurately “The Envelope System.” It is very inexpensive to get started and implement as all you will need is a $1 box of plain white envelopes. Then you simply divide your budget into spending categories and label the envelopes accordingly (e.g. food, gas, clothes, entertainment, health and beauty, household needs, etc.), and place the amount of money that you have allocated for the month into the appropriate envelopes. This gives you a great visualization of how you are doing. You can actually see how much money you have left to last you until the end of the month. When the money is gone it’s gone. No more spending for the month. Can you “cheat” and take money from another envelope if one of them is empty too soon? Sure! But just who are you cheating? Yourself, of course! And, if you want to stay on budget, now you have less to spend in the category of the envelope you “stole” the money from. You will get better at knowing how much to put in each envelope for the month as you become more practiced at it. And hopefully you will also get better at finding ways you can save more money in each category too! As I continue these blogs I will delve more deeply into just how to find those ways of saving more money in each of those categories. You can also attend my monthly meetings at the Red Hook Community Center for more tips and tricks on saving money through the magic of frugal living. (See the Events and Classes page). So until we meet back here next month, I bid you adieu and happy savings!  I am so excited to welcome you to my new webpage and get started on a money saving journey with my readers. This blog will be chock full of tips and strategies each month that you can use to set and achieve any and all of your financial goals from the short term to long term to the ultimate of a secure, happy, well-funded retirement and even a legacy to leave to your heirs. The new year is traditionally a time of getting started so this is the perfect time to take a look at where you stand right now with your finances and what goals you would like to achieve this year and beyond. No matter where you are at present the best time to get started on improving your financial status is right now! Before you can begin to set goals it is important to know where you are right now. Set aside some time to take a look at where your money is going. Write out an expense sheet. Include all your expenses big and small, from your fixed expenses (rent/mortgage, insurance, cable, phone, etc.) to your more variable expenses (food, heat, gas, clothing, entertainment, etc.). And don’t forget the occasional expenses (school supplies, Christmas, vacations, car repairs, etc.), as well as all those little expenses that you hardly think about (your morning coffee to-go, vending machine treats, lunches out, beauty products, etc.). If you are not in the habit of noting all your expenses, it may take some time to remember them all. I suggest getting a little notebook to record what you spend money on each day at least for a month. (Even I still do this on a daily basis.) You can use this worksheet I've made to complete this step.  In the meantime, take stock of any debt you have. Write down all of your debts including the full amount owed and the interest rates. Add them up to get your total owed. If you have assets, good for you! Take note of them too. Money in the bank? 401k (403b)?, Any investments? And write down what your income is, including all sources; Your (and your spouse’s) salary, child support, SS payments, rental income, extra side jobs, etc. Now that you have a clear picture of where you stand, you can plan your goals. Let me give you a little hint here. Your first goal should be to pay those debts down! No debts? Great! Is there something you want to save up for to buy this year? Do you have a bigger purchase in mind that might take a few years to save up for? (a new car or down payment on a house?) Do you want to save up for education? (yours or your kids). And then of course there is the ultimate goal, that nice comfortable retirement nest-egg! For the smaller goals it is simply a matter of dividing the total needed by the months you have until you need the money. Then you know the exact amount you need to put away each month to achieve it. For that ultimate big retirement reward, slow and steady wins the race. The earlier you start the better off you will be. This should be an automatic amount taken right off the top, before you even see it. Of course a job 401k will do this for you, but if you don’t have access to one you can set up your own retirement account and have automatic deductions going straight into it from your checking or savings account each month. I know this is a lot to contemplate all at once, but for now just take this month to take stock of your expenses and debts, and think about what goals you might have for your money and I will lead you through the rest of it step by step as the year progresses. When you do it step by step you will see how easy it can actually be to turn your finances around. We will start to talk next month about just how to budget your expenses and find the money to put aside for all those goals. ` Stick with me and you too can have a bright future!  |

Archives

June 2022

Categories

All

|

RSS Feed

RSS Feed