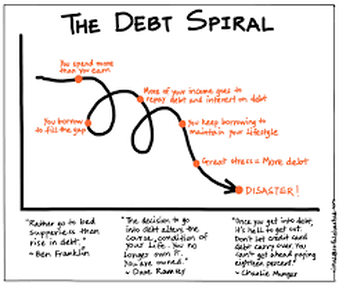

There is a law of physics that you’ve all heard of that states that an object in motion tends to stay in motion. Well, I’ve observed that it is the same with most people’s finances. Once people get going in a certain direction with their money, they tend to remain on it until something happens to change it.   This motion can be in either direction. Once people begin to live beyond their means and start to accumulate debt, that downward spiral into debt begins to snowball, making it very difficult to get off the ride. But the good news is that, conversely, if people can start to move the needle in the opposite direction and start to save money instead of accumulating debt, this too can have a snowball effect and the more you save, well, the more you save! Being in debt becomes a perpetuating cycle for the very reason that you are in debt. When all your money is going towards your credit card and other debt payments, there is never any money to use whenever something comes up. And this too goes on the card. You can see (or maybe know firsthand) how this could go on and on. On the other hand, if you have money saved, you not only easily pay for any financial emergency or need that comes your way, and avoid paying interest payments, but you can also take advantage of strategies that can grow your money even further.  The most obvious of these opportunities would be the ability to invest your money. Now instead of paying out interest you have the ability to turn it around and have that interest work for you. And thus the snowball grows (in a good direction!)  When you have a cushion of money beneath you, you no longer have to approach life from a position of desperation. Desperate people need to resort to desperate measures to keep themselves afloat. Think of those insidious payday loans, with their ungodly interest rates.  Desperate people do not have the money to maintain their possessions (I.e., cars, appliances, roof, etc.) or even their health, and often end up paying much more in the long run for car repairs, home repairs, or even worse, a health crisis because they were unable to keep up with the maintenance required.  Of course, the key is to turn this trajectory around to be moving in a positive direction. The hard part is the turning. It does take a lot of work and sacrifice to get a debt situation under control. But once you push through and make it to the other side the rewards are immense. Now you can relax and let that money work for you. The very interest you were fighting now becomes your friend. It’s a great feeling.  I hope I can inspire you to begin to move your needle in the right direction. I will be here cheering you on the whole way! If you need any specific strategies to help get you going, take a look through some of my other blogs for some tips and tricks that might work for you. If you need more personal help, feel free to contact me for a one-on-one appointment.  Wishing you all the best in snowballing your way to a better and brighter future!

0 Comments

Sometimes there is just something to be said for boiling it all down into a nutshell and that is just what I have decided to do in this blog. This is pretty much says it all in seven easy-to-follow rules. The best time to start living these rules is from the minute you start that very first job. That is the time to set up good habits that will keep your finances healthy and thriving for your entire life and ultimately lead you on the path to that beautiful dream of financial freedom!  If you know anybody who is just starting out here is the perfect gift for them. Just print these rules out for them and you will have changed the trajectory of their life forever.  1. Always live below your income level (and be saving for retirement and goals). 2. Always be saving at least 15% of your income into your retirement account(s). 3. Always have an emergency fund set up of at least 3–6 months' worth of spending. Your Emergency Fund questions 4. Keep track of all your spending. Know where your money is going! 5. Learn to distinguish wants-vs-needs. Many things that we think of as needs are actually wants. Don’t buy wants if you can’t afford them. 6. Never buy anything on credit (including cars). No Loan Auto Ownership. Save up and pay for things with cash. One exception to this would be a mortgage on a house but put a hefty downpayment down. Get a 15 yr fixed rate mortgage and pay it off ASAP. 7. Pay yourself first! Put your savings on Automatic Pilot. Set up an online bank account (or a few) to save up for your future needs. It’s better if you can have a separate one for each goal (i.e the car account, the wedding account, the vacation account, etc.) Set up automatic payments going into them each month from your checking or savings account. You really can’t go wrong if you live by these simple rules. They're not that hard to do! Wishing you all a very bright future!   There is panic all around us. What should we be doing to keep ourselves and our loved ones safe? How long will this last? What supplies do we need? Do we have enough toilet paper? Sometimes we can be blindsided by what life throws at us. The best way to be prepared for the unexpected is to, well, be prepared.  In the case of a new disease coming your way, you are in a much better position to deal with it if you have been living a good healthy life up until that point, eating good fresh whole foods, getting proper rest and exercise, maintaining a healthy weight, etc.. If you have been living this way, chances are you have a much better immune system to fight off the infection. But if you have been eating a poor diet, are out of shape and overweight, leading to possible chronic conditions, can you suddenly start living a healthy lifestyle and expect to have the same healthy immunity as the infection invades your community?  Obviously you would have had to been building up that immunity and living a healthy lifestyle for quite some time for it to be effective for you now. I guess you are getting the idea of where this is leading to. The way we live our everyday financial lives also has a big impact on how well we are prepared for whatever life may throw our way.   Perhaps this coronavirus has directly (or even indirectly) affected your income. Are you financially prepared to weather the storm? Times like this bring home just how important it is to live below your means (when you have means) and constantly be putting money away for the lean times (or that big “lean time” in your future, otherwise known as retirement).  If your ordinary life includes having no debt, having a good emergency fund put aside, and saving on a regular basis, then you are much less likely to feel panic and upheaval when you come to a bump in the road. The more “padding” you have the less you will feel those bumps. Things that are a (financial) crisis to the ill prepared are merely blips to those that have the money to deal with them and move on.    If you see the sense in this and would like to shift from a living-on-the-edge (paycheck to paycheck) lifestyle there are many actions that you can begin to take to shift to a saving way of life. If you don’t know where to start I have many blogs on various aspects of money saving strategies that you can implement. Right now, while you are likely sequestered at home, might be the best time to finally sit down and take a good look at your financial situation and take control. Here are just a few that you might find particularly helpful: New Year Savings Resolutions Would You Love to Save More Money? Spring Clean Your Finances Strengthen Your Frugal Muscle, Lighten Your Stress Easy Peasy Savings, Make it Automatic Saving Money Every Day The Perks, Pluses, and Payoffs of Prioritizing My Message to Millennials Ready, Set, Goal! Money Saving Grocery tips from your “Auntie” Victoria And if you scroll through the rest of the blogs, you may find some more that apply to your particular situation and needs. If you need further individual help feel free to contact me at (845) 758-0250, or brightfuture2budgt4.gmail.com for a personal appointment.  Wishing you all the best for staying healthy now and moving toward a healthy financial future.

Having spoken with a few millennials lately, including one young lady who was very motivated to get started on the right financial footing, (this is not always the case with the young people I encounter), I thought I’d devote this blog entry to those just starting out on their lives’ journey. This is the stuff that I wish somebody had told me when I was just starting out. I figured it out along the way, but it would have been nice to know it all from the beginning. And some people, unfortunately, just never do figure it out for themselves. Would I have listened? Who knows? But, as they say, if I knew then what I know now, and followed the advice I am about to impart to you, I would very easily be a multi-millionaire by now. And you can be too. Anyone can do it.  Often I find myself very frustrated that young adults, who have the most to gain from learning to be smart with their finances, can be the most resistant to hearing (and following) it. And the sad thing is that if they don’t do it now, although they can still do alright whenever they decide to start, they can never make up for that lost time and the money they could have made by investing early. The magic of all those years of compound interest can never be regained.   So, without further ado, in a nutshell, here are my most salient tips for millennials: #1. The golden rule of finance: Always, Always, Always Live Below Your Means! Start out that way and get used to it. As your income increases you can increase your lifestyle, but always stay below what you are making. 15% of your income should going into your retirement fund at all times.  #2. The other golden rule of finance: Pay Yourself First! You will be paying out a lot of your hard earned money to other people and businesses in your lifetime (your landlord, the mortgage bank, electric company, insurance companies, gas company, food producers, goods manufacturers, health care providers, etc., etc., etc.,…..), but don’t give all your money away to other people or you will have nothing to show for it. Always be keeping something for yourself… up front, before any of your money goes out to anyone else.  #3. Make it Automatic Set up that money to go into your retirement account (401k or Roth IRA) and your other savings (goal) accounts straight out of every paycheck before you even see the money. Out of sight, out of mind.  #4. Keep track of your expenses Set up a system so that you know exactly how much you are spending, every day, every month, every year, and on what. You can do this by hand (simply writing it down) by computer (i.e. your own spread sheet) or with a website (such as mint.com)  #5 Prioritize your budget: Spend your money on what is most important to YOU First comes dire needs, housing, food, transportation, etc. Then prioritize the rest according to your income and needs. Wants come last, and only if you can afford them. Think carefully about wants-vs-needs. Do you really want to sabotage your future goals for some frivolous indulgences today?  #6 Plan for your goals Write them down and save for them systematically (how much do you need to save and when do you want it?). Do you want to get an education? Plan a wedding? Buy a house? Buy a car? Go on a vacation? Always be saving for your future purchases so that you will… (see #7)  #7 Never borrow money! (AKA buy things on credit) Don’t get into the interest paying trap. It is a slippery slope once you start on the debt quagmire. This includes education (student loans), cars (car loans), and those insidious credit cards. Always save up and pay for things in cash. If you don’t have the money, you can’t afford it. The only possible exception to this is buying a house. But even here, if you can manage to save up and pay cash that would be awesome. People do it. I did it for my second house (after I paid the first off by ten years). Certainly aim to put down as large a down-payment as you can and take out a 15-year mortgage. Then (pre)pay that down as quickly as possible. And don’t buy a more expensive house than you can afford. Though the lending banks will pre-approve you for a much bigger mortgage than you can comfortably afford, don't fall for it.  It’s really as easy as following these 7 very simple rules and you will be set for life. It’s not rocket science. Anyone can do it, at any income level. Stick with this lifestyle and you will go from millennial to millionaire, a very bright future indeed!  Which one are you? Hopefully in the green!  You can do it!!

You’ve all heard the expression “April flowers bring May Flowers” I’m sure. But what does it mean? Well in its literal sense of course, we need the rains of early spring to give us those beautiful flowers to enjoy in May. But what is the deeper meaning of the phrase beyond that? When we say it we are talking about how we are willing to put up with some less desirable weather in April because we know it is necessary so that we may delight in the lovely blooms that follow. But we can also apply the phrase to other situations in life. Very often it is easier to endure a less than pleasant circumstance because we know it is essential for something better to come. The financial guru Dave Ramsey has a great saying “Live like no one else so you can live (and give) like no one else later on.” In other words, if you have a future financial goal in mind you will be willing to make the sacrifices that it takes right now in order to attain them. You appreciate the showers because you know they will result in a richness of flowers.  Are you a grasshopper or an ant? The grasshopper will ignore the future and just live for today only to be surprised when winter comes and he has nothing put aside to get him through the cold snowy months. Meanwhile, the ant has been working throughout the summer to build up a stash to sustain her throughout those food barren months. Does this mean that the ant has no fun while he is preparing for the future? Absolutely not! There are a great many ways that that little ant can have fun while also taking the time to put those resources away for that rainy day. But the wise little ant always keeps in mind that winter is coming and does what she needs to do to be prepared.  So, yes, enjoy yourself for today. There are any number of ways that you can enjoy life for very little cost or for free. But if you are a wise little ant you will always be stocking up for the future so that (unlike that silly irresponsible grasshopper) when the future comes you will have an abundance to enjoy and your winter will be more like a gorgeous phantasmagorical riot of spring blossoms. Because you, my little friend, prepared for it.   This is the priority based budget. And it is a great tool to use to help you realize just what your priorities are and exactly where you want your money to go (and, maybe even more importantly, not to go). I could look at where your money is going and give you an idea of where you might be able to trim the fat and the things that I would not “waste” my money on, but at the end of the day it is your money to choose to spend as you will. Of course if you are looking to save money you cannot “choose” to keep spending on all the things you have been spending it on. This is where the priority based budget comes in as a tool to help you with that decision making process. The concept is very simple. You start with the most important things that you want your money to go for. And here we are not talking about the things you “want” the most. We are talking about your most basic needs. You also start with the amount of money you bring in for the month. As you list each expenditure you subtract that amount from your monthly income. So you would start with things like housing (rent or mortgage, and property taxes if applicable), food, electricity, water, heat, insurance, and then continue down the list to “lesser” but necessary to your life expenditures. And as you do this you continue to subtract from your monthly income. By the time you get to the bottom, depending on what your income is you should be getting to your “want” items in order of which things you want the most. When you get down to zero on the other side you are done. You can’t (or I guess I should say shouldn’t) spend money that is not coming in, because this is, of course, what leads to debt. Everyone has different priorities and what would be a frivolous expenditure in my eyes may be a very important source of joy and happiness for you. But the bottom line (zero) is the bottom line no matter what your circumstances are. You cannot go beyond that and this is what forces you to examine what your spending priorities are.  If your money is very tight, you may not even get past the “needs” at the top of the budget. There is no room for “wants” at all. If this is the case you will need to examine how you can increase your income. You can temporarily take on a second job, but you will also need to come up with a more permanent solution to your income dilemma. Can you ask for a raise? Look for a better job in your field? Should you try a different line of work? Get additional education? You need to come up with a plan of action, and start taking the necessary steps to get there. If you have debt, then paying that off should go right after your basic needs are met. If you do not have debt, then you are in a position to start saving and that savings should be at the top of your line items. Retirement savings being at the top, followed by other savings goals. i.e. a wedding, a house, kids (or your own) education, a car, vacation, home improvements, etc. This is the concept of “Pay yourself first” and it works! This way you have all your life goals covered by the time you get down to the bottom of the budget to those everyday “wants”. I have included some budget worksheets that you can use to create your own Priority Based Budget. One has categories to give you some guidelines (but feel free to change them according to your own priorities). And some samples to help you see how it's done: Sample 1. Sample 2. The other is left blank for you to fill in as you see fit. And more samples: Sample 3. Sample 4 The lefthand column of both of them is for you to start with your monthly income and then subtract as you make your way down your list of spending priorities until you get to zero at the bottom... money gone... budget done! You must of course (if you are sensible and want to get ahead with your money) include your saving goals as part of your monthly budget and also things that you will not necessarily spend money on every month, but that you will do so from time to time (like car or home repairs).  Once you finish with this exercise you will have a clear black and white picture of where your money is going according to your own life’s plan. You are on top of your money. You are in control. And that’s a pretty darn good feeling! Congratulations!   This is, of course, the time of year that we traditionally give thanks for our blessings. We express gratitude for our warm homes, our families, our health, the bountiful food set before us, and whatever other good fortune has befallen us during the course of the year . . . then we dig in, and move on to other things; sports, the weather, movies, politics (and hopefully world war III does not erupt at the dinner table at this point). But what about the other 364 days of the year? And what, pray tell, does this have to do with frugality? In a word… everything! Why? If you think about it for a moment, the very causation of overspending is exactly the opposite of gratitude and thankfulness. If we are truly content and happy with what we have in our lives at this very moment, then why would we feel the need to go out and acquire (buy) more (and more) stuff? We wouldn’t.  It’s one thing to pay lip service to thankfulness, but unless we truly feel it in our hearts we will never be completely content and will never resist that constant urge to have more. Don’t get me wrong. I’m not saying you’re a bad person every time you buy something. And it is absolutely human nature to continually want more, in fact, I would argue not only human but all animal nature as well. It is bred into us as a survival mechanism. In a world of “survival of the fittest” and scarcity, this instinct is necessary to keep us alive. But herein lies the rub. We no longer live in that world of scarcity, but unfortunately, our basic animal instinct has not caught up with that fact. So now instead of a nice little cache of saved up nuts and berries to get us through the colder months, we have 15 pairs of shoes and 50 pieces of jewelry stashed away. And that wanting “itch” will just not go away.  Comparison is another enemy of contentedness. We don’t only live in our own little bubble, but we are constantly looking at what everyone else has. I can’t even fathom what the survival mechanism is in play here but animals definitely do this too. If you’ve ever had more than one cat, for instance, it is comical to watch them run to the other’s bowl before they have even finished their own meal, just to make sure the other cat did not get something better than they did. If you live in a 1,500 square foot house while everyone around you is in a tiny shack you feel like a queen, but how would you feel if everyone else was living in a 4,000 square foot “McMansion”? Is there anything different about your 1,500 square foot house? No. So what changed your level of happiness?  Most people in our country live far more opulent lives than a large percent of the world’s population, even more opulent than the general population of our own country did 50 years ago. But since see we don’t see them (or remember that simpler time) we are constantly striving for something better. The problem is that there is never an end-game to this desire. And people quite literally go into debt every day because of it. I’m not saying it is easy, and it is certainly going against the very grain of our instinctual nature but in the long run, your life will be more deeply satisfying and happy if you can fight the urge to splurge and feel the rich ample abundance of what you already have. And that, my friends, is what being frugal is all about.  Wishing you all a very happy Thanksgiving!

Last month I discussed the topic of saving money on your school expenses. Now I would like to suggest that you think of every day as an opportunity to save money. Staunching the flow of money out of your pockets in your daily life you can really add up to some serious savings by the month’s end. And even more serious savings by the end of a year. Invest that money and just watch the pile grow larger year after year. All with a few simple changes in your life to save, well, some simple change each and every day.  It really requires nothing but a shift in your mindset. When you start to look around at every purchase you make (or decide not to make) with an eye to saving a few bucks you will be amazed at how many opportunities to do just that will arise. Here are some key points to consider before making any purchase. It may seem obvious but first of all, do you really need it? A great deal of purchases are made for things that we don’t really need. Try to be more cognizant of this before parting with any of your hard earned bucks. From the blatant impulse buy (snacks, drinks, etc.) to the fancy gadgets. Stop and think. Do I need this? Do I already own something else I can use for this purpose? Can I borrow it? Can I wait until it comes down in price? Buy it used? If you decide that you really do need an item, do not buy it on impulse. Take some time to comparison shop, look for deals, bargain with the seller. If you take enough time you may even cool off and decide you don’t need it after all And remember the old expression “Waste not, want not” (or am I dating myself here)? Another (more modern?) way of putting it is “Use it up, wear it out, make it do, or do without.” These are excellent frugal words to live by. The less you waste your resources, the less you have to spend money replacing them. This applies to all aspects of life and everything you spend your money on, from food, to beauty products, to cleaning products, to clothes, to utilities (heat, electricity) and even to electronics, appliances, and cars. If you keep these expressions in the forefront of your mind it will help you to make wiser more frugal spending decisions in your everyday life. Speaking of utilities like heat, electricity, and also phones, internet, and TV, and insurance, do not leave them on autopilot. Revisit what you are spending on these things every so often. Are you really using everything you are paying for? Do some comparison shopping. Perhaps it’s time to switch companies? Sometimes even the threat of such a thing will get your existing company to lower its rates. Sometimes entertainment is a big budget drain. Keep in mind that there are a great many ways to be entertained for free. At home game nights, potluck suppers with friends, videos borrowed from the library, village festivals and events, picnics in the park, hikes, bike rides, free museums, and art exhibits, the list goes on and on. (And if all else fails you can always take one of my enlightening and fun courses or attend one of my Frugal Living meetings one night for a nominal fee) ;)😃😃 I would like to get up on my soapbox for just a moment with a little speech on the pleasure principle. Think about something that you really enjoy. Chocolate? Wine? A big juicy steak or lobster? Now imagine that you have unlimited access to said thing (since we’re imagining here, you might as well imagine that said thing will not do anything to your waistline or arteries). Now you can eat this thing as much as you want all day, every day. (I’m not sure what it says about me that all the items I chose were food). Anyway, what do you think that constant access to your beloved treat would do to your enjoyment of it? I would wager a guess that it would no longer hold the same joyous appeal after a while. So what I am saying is a little self-deprivation of the things that you love can actually enhance your enjoyment of them. Good for your pocketbook, your waistline and your pleasure sensors! A win-win-win all around! And it goes without saying (or does it?) that you should always consider before you make a purchase whether this is a want or a need. Be honest. Many times what we call a need is actually a want.  And what I like to do is make a game out of it. Challenge yourself. How low can you go with your grocery shopping this week? Can you skip a week and creatively make use of what you have in your pantry already? How long can you stretch that product? Always use everything to the last drop. How long can you go without buying clothes? Without getting a haircut? Save every $5 bill you get for one month (one year?) Make mini goals for yourself. If you usually spend $100/week on groceries, try to keep it to $80 this week (then $60 …). Can you put away an extra $200/month ($50/week) to pay for a nice vacation next summer? (without having to put in on the credit card). Once you get into the “mode” you will begin to discover many ways in your daily life that you can shave off a few dollars spent. And this success will spur you on to even greater savings. It’s a wonderful feeling to gain control of your spending and have your money work for you in a way it never has before. The joy of frugal living can be very addicting. And unlike other addictions this is a great one to have!

Living in such a materialistic society as we do, it can be hard to even detangle oneself from the mindset of constantly wanting and buying more and more stuff. We have been bombarded with ads from a very early age, from every possible media, telling us why we “need” this that and the other thing. We are told how each of these items will make our lives easier, fuller, more fun, etc., etc. Just the very act of “shopping” has become a leisure time activity in and of itself. We are trained to always want the bigger and better next thing. We compare ourselves to others based on if our stuff is as good, new, and shiny as theirs. We never reach the point of satisfaction because there is always that next best new thing coming out that we have to have, as evidenced by the lines for the newest model iPhone. Really??! Is it that much better than the previous model that you have to waste precious hours of your life waiting on line to have it a few hours (or even days or weeks) earlier than you would have been able to get it otherwise? To me, that represents the epitome of how deeply this materialistic mindset is entrenched in us.   And once we get that new thing, how long does the satisfied happy feeling last? Not long apparently as evidenced by all the stuff put out at garage sales (many with tags still on), not to mention Craigslist, eBay, and even worse, into the ever-growing landfills. It is the thrill of the acquisition that is being sought. Once we actually own the thing the joy fades pretty quickly. This just sets us up for wanting more to experience that “high of the buy” once again. As you can see with this type of scenario one can never be truly satisfied and happy. Would you like to get off this unsatisfying and frustrating carousel? I know I do and I make a very concentrated effort in my life to buck the system. It can be hard to do when you are literally surrounded by it, but the better you get at recognizing the pattern and fighting to control being sucked in by it, the happier (not to mention less stressed and richer) you can be. It is when you get out of the “more and better stuff” mindset you truly start to appreciate the things that you have. And ironically the less stuff you have the more you appreciate it. And even more ironically the less you pay for each item the more you appreciate it. I take great satisfaction in having acquired an item for free or very inexpensively that has given me much use or added beauty to my life. The less I spend on something the more I appreciate it, because not only do I appreciate the thing itself, I am also appreciative that it did not take my hard earned money away from me. This can be especially true of items that we tend to collect a lot of, such as clothes. It feels much better to have a few shirts that you really like and enjoy wearing than to have your closets and drawers stuffed with them, many of which you don’t even wear. And if you spent a lot of money on those shirts that you don’t even wear that can make you feel worse. As they say, “Less is more”. It really is true! I take great pleasure in buying a shirt that I really like at a thrift shop for a few bucks (or even better if someone has given it to me for free) and I feel that pleasure each time I wear the shirt. The fact that our world is bombarded with stuff and we can go out to stores filled with it and buy, buy, buy, and now even at home we are bombarded with the urge to buy, buy, buy on our computers leaves us in a state of wanting constant instant gratification. All we have to do is have a thought of wanting something and it can be ours at the swipe of a credit card or click of a button. But has this made us any happier? I would venture to say no. What it has done is deprive us of the joy of waiting for our pleasure. For it is in that anticipation of pleasure that our excitement builds up. If we have to wait for something, then we appreciate it so much more when we finally do get it. Instant gratification has effectively deprived us of that very pleasure. Some people think of trying to live below their means as a painful way to live. They view it as deprivation. But it is all in the mindset of how you approach it. I find that living below my means gives me more pleasure than living the life of constant instant gratification through buying more and more stuff. It is a less stressful, slower, more satisfying way to live. It allows you to savor pleasure more deeply rather than to be constantly looking to acquire the next best thing. I urge you to give the joy of slow acquisition a try. You will be surprised how much pleasure not spending money can bring you. Your life will be less stressful, more peaceful and richer than ever before, I promise!   Here’s the biggest mistake almost all people make when it comes to savings: They pay their bills, buy their food, make repairs, buy things for the house, pay for kid’s activities, go shopping for clothes, go to the movies, go out to eat, go shopping for some new clothes, etc., etc., and then save what’s left over at the end of the month. Can you see the problem with this? Is there ever anything left at the end of the month?? Many people will also say that they live paycheck to paycheck, but here is the interesting thing about this; They are saying this no matter what the size of their paycheck. The person who makes $300/wk. is saying it and so is the person who makes $600/wk. and the one who makes $3,000/wk. and on up. Right up to that athlete or rock star who is making several million dollars a year and blowing it all, only to go bankrupt when the income dries up. It seems to be just human nature to live just up to your income level whatever that may be, or even a little above that (accounting for all the debt people tend to find themselves in). But if you want to save money the only way you can do it is by living below your means, whatever they may be. Another way to put this is: You don’t save money by how much you make, but by how much you don’t spend. The great investment “guru” Warren Buffet puts it this way:  This is great advice, but how do you do it? Well the great US of A knows how. You pay taxes every year, right? Does Uncle Sam just let you have your full pay and then ask you to cough up the taxes on April 15th? You bet your sweet bippy he doesn’t, because he knows what would happen. People adjust their lifestyle to however much money is coming in. So he just takes his cut up front and people adjust to living on what’s left. Well you can do the same thing for yourself. Just take it off the top. The U.S. government even gave people a means to do just that by starting the 401K program, giving you a tax advantage and a way for you to save money by skimming it right off your paycheck without even ever seeing the money. If you have this offered at your place of employment you should certainly be taking advantage of it. Some generous companies will even match your contribution dollar for dollar up to a certain amount. Free money! Never pass up this opportunity! But even if you don’t have the opportunity for a 401K (or 403B, TSP, etc.), you can still make the magic of automatic savings work for you. All you have to do is set it up once for yourself and done. Savings skimmed right off the top. Out of sight, out of mind. You will quickly adjust to living on what remains. How you set this up depends on what you are saving for. Your first savings goal should be your retirement. I know this sounds kind of backward or counterintuitive, but because you need such a large amount, and because it makes such a difference when you start compounding that interest early, it is imperative that you start this ASAP! If you don’t have a 401K then you can set up your own retirement account in a Roth IRA. I recommend you do this by opening up a discount brokerage account at a firm such as Fidelity or Vanguard. This gives you many options on what to invest your money in inside of your Roth IRA and gives you complete control over it. Once you have your Roth set up it is quite simple to set up automatic payments of whatever amount you choose monthly going from your checking account into your IRA. Whether you have a 401K in the workplace or your own Roth IRA, you can also set up similar automatic payments going into (online) savings accounts for your other savings goals (wedding, car, house down payment, education, etc.) Once you have your savings goals set up automatically in this way, you no longer have to stress about money. You are all set for your future needs both short and long-term, and you can spend what’s left freely. Won’t that be a nice feeling!  |

Archives

June 2022

Categories

All

|

RSS Feed

RSS Feed