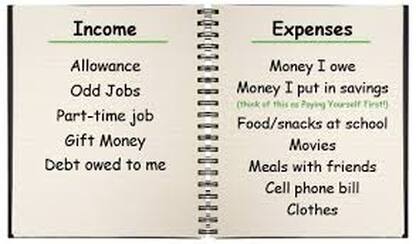

Last month I talked about what lessons it is important to be teaching your kids about money. I mentioned that I would go into more specifics about teaching teens about money in a later blog. Well, I figured I might as well go on to it sooner rather than later, so here we go.  Those lessons taught throughout childhood should be continued to be reinforced throughout their teen years of course, but now you must get even more specific about actually preparing them for living their lives as financially independent adults. By teen years they should:  Be paying for as much of their own needs as possible. This includes their clothes, phones, entertainment, car expenses, etc. Even if you are giving them an allowance to cover some of it, the money should be “theirs” to budget for all these expenses. This will set them up for learning to budget their living expenses when they are out on their own.  Be saving for their future needs. They should have been saving for bigger “wants” throughout their childhood. Now they have some needs to be saving for. The biggest and most obvious is that first car. Encourage them to save for it. Even if you help them out, by giving them some cash “gifts” along the way to add to the savings or offering to match their savings (to let’s say equal to the amount that have saved), it should still feel like something that they have saved up and paid their own money for. This way they will learn to save for their bigger purchases throughout their lives. When my own children bought their first cars this way, I went one step further and had them set up an online bank account and pretend that they had bought the car “on payments”. But instead of paying the car payments to the bank they set up automatic payments going into their own (online) “car account”. This way they were ready to pay cash when they needed to buy their next car and would never need a car loan (or pay interest payments). For more on this see No Loan Auto Ownership  Be advised to go to college with no (or as little as possible) student loans. Make sure they know that where they went to college will not make a whit of difference years down the line, but those student loans (if they choose to take them) will still be with them for a long time to come. They can attend community college for the first two years. Unless they get a great scholarship, they should attend a state school. For more tips on how to save money on college see: Smart-financial-planning for College  Be taught the dangers of credit cards and debt. When your child is nearing the age of 18 they will be starting to receive credit card “offers” in the mail. Teach them to steer clear of these. Talk to them about how easy it is to go into debt. Teach them to only spend the money that they already have. Do not be spending “future money” that has not even been earned yet.  Many kids get credit cards in college with disastrous results. They end up graduating with not only student loans hanging over their heads, but also start out their independent lives with credit card debts already weighing them down. Let them use a debit card for their expenses in college. Caution them to keep track of how much is in the account at all times.  )Know about credit scores. No one should be taking out a credit card until they have a very full and mature grasp on managing their money and budgeting wisely to pay their expenses and also saving for the future. Only once this is happening should they open a credit card in order to obtain a good credit score. It is possible to live without a credit card at all but unfortunately not having a (good!) credit score can make life difficult at times as it is looked at by prospective employees, landlords, car rentals, and of course, eventually, mortgage bankers. But it should be used only for the purpose of obtaining that good score. To achieve this, teach your offspring to open one credit card and use it for one thing (one bill, or only groceries, or gas, or whatever). Always pay it in full and on time every month. Never carry a balance on it. And never use it for anything else, especially something that they can’t afford. Save up for things and pay cash with money that they already have. This is one of the most important concepts you can teach them.  Know about the virtues of compound interest. And why it is so important to start investing early. Teach them that if they invest early and let the money grow they will have to invest far less of their own money to achieve the same nest egg of someone who started later. The magic of compounding interest will do the growth for them.  Know how important it is to always live below their means. Which if you think about it is exactly what they will be doing if you have successfully taught them all of the above lessons.  Know how to feed themselves frugally. Teach them to cook. Show them how much cheaper it is to buy your own inexpensive ingredients than it is to eat at restaurants or get take-out. For a primer on frugal grocery shopping see Money Saving Tips from Your Auntie Victoria  When you send your newly minted adults out into the world armed with this important knowledge, you (and they) can be assured that they will not become a part of the hapless statistics on adults living in debt and with no financial safety net beneath them. They will have a strong financial foundation from the very start. And your work is done.  Wishing you and your children the brightest future you can have!

2 Comments

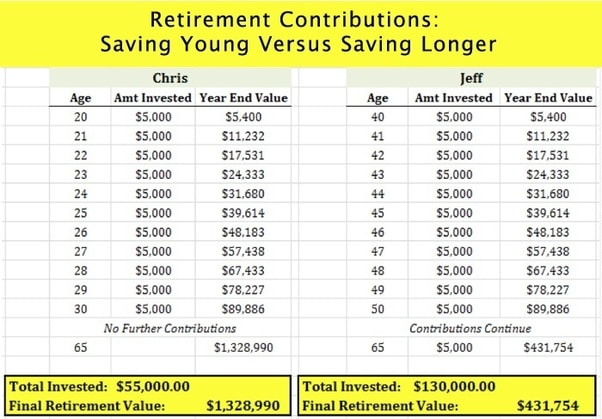

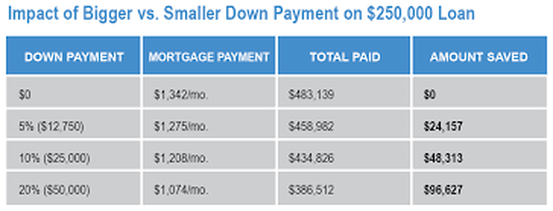

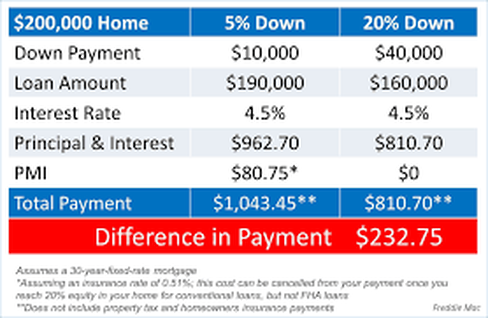

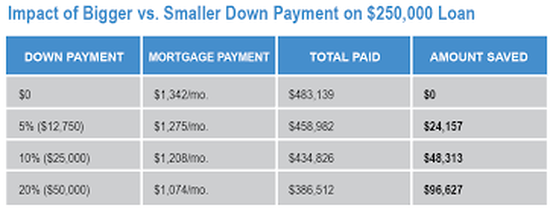

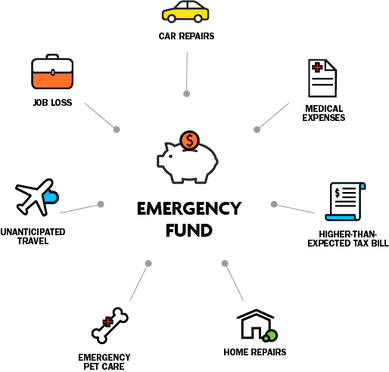

I’ve seen or heard this question posted in many different ways throughout the years, the gist of it being that one needs to make a fundamental decision between enjoying their life or saving for the future. I’ve heard the argument that you must “live” for today because you could be hit by a bus tomorrow. Young people have screamed YOYO! (Did I just coin that?), as in, “You’re Only Young Once”. They maintain that they must spend and “live” for today while they are young enough to enjoy it.  But I don’t see it as a black and white, either/or situation: Save OR have fun. I believe that if you are wise with your money you can do both. Saving your money does not mean that you have to be a miserly scrooge sitting in your lonely attic counting your money and never having any fun. In fact, with a little planning and wise money management you can easily have a very pleasurable life and also save for your future at the same time.  The one equation that people need to let go of is “Spending Money = Fun.” There may be some correlation to that sometimes, but it is certainly not a given. You can spend lots of money on something and have a terrible time, and even more importantly it is very possible to have a great time spending no money at all. I’m sure you can think of several examples of both these facts in your own life. Let’s start with the young (my newly coined YOYO philosophy). Yes, they can certainly save and also have fun. First of all, they have one huge advantage in their favor… the magic of compound interest. The fact is if you start saving (investing) early you will only need to save a fraction of your own money in order to build up a very tidy nest egg for retirement. Most of the money in your IRA at retirement will be growth on the returns you accrued through the years (not the money you actually put in). Pretty neat trick, huh?  With a little prioritizing and forethought young folks can also be saving for their other more near-future needs/wants (a car, a house, a wedding, et.) by putting those savings on automatic pilot and just living on what’s left. The prioritizing comes in as you make the conscious decision to forego (instant pleasure X) which is not really adding a great deal of joy to your life in order to save up for that something that will bring you great pleasure indeed.  The one joy that seems to be mentioned a lot is traveling. And here is where the young have another distinct advantage. They can travel for practically nothing, staying in youth hostels, or other low cost accommodations. There are even many temporary internship/job opportunities overseas that can allow them to see the world while sometimes even making a little money. The possibilities of low-cost travel are only limited by the imagination for the young (or young at heart). Google “traveling on next to nothing” and see what you come up with. I read a great memoir on the subject a while back called “No Baggage – A Minimalist Tale of Love and Wandering” by Clara Bensen.  What about if you are not young? I see people of all ages squandering their money on daily instant gratification pleasures without even realizing that they are doing it. Once, when I was telling some friends about a trip to Singapore that I had just returned from, somebody asked me “I don’t understand. You can’t afford cable TV, but you can afford a trip to Singapore?” My answer to that is you can afford anything (within reason, of course), but you can’t afford everything. I chose to forgo all those channels at $150/month in order to save my money for something better. I even found a way to get TV for free (an old fashioned roof antenna). I also put my frugal skills to use to make the trip possible without breaking the piggybank.   If fun is your priority, then go ahead and have it! Have as much as you want. Live! Take advantage of all that free fun that is out there for the taking. If there is some kind of fun that you must have money for, then just look at your spending habits and give something up that does not bring as much joy and save up for what you want.   I see absolutely no reason why you can’t do both. Save and have fun! After all, you only live once!  Wishing you a happy life today and a bright future tomorrow!   Someone I know recently bought a house and my 24-year-old son was asking me about the details. His number one question being “How do people save up that much for a down payment?” As I answered his questions it got me to thinking that I never addressed this topic in these blogs, so here goes:  How do you know when you are ready to buy a house? Well some people think it’s just a matter of saving up that down payment, but really a lot more preparedness needs to go into it. First of all, how settled are you? Many young people move around quite a lot for job changes or other purposes so even if they are very lucky enough to have that down payment at such a young age, it is not necessarily the best time to be putting down roots into home ownership just yet.   Unless you are sure that you will be staying put for at least the next five years, buying a house is rarely a smart move financially. You will sink a lot of money into the act of buying the house (in closing costs, realtors fees, inspections, lawyer’s fees, etc.)  Then once you buy there is the cost of moving in, and often on top of that people will do some work to the house to make it more to their liking. And there is even the inevitable furnishing and decorating, especially if you are starting from “scratch” with nothing.  And if you have put down a small down payment, you will typically not be gaining much equity in the house for the first few years, at least, as most of these initial payments are going to the interest on the mortgage. It is not until the principle starts to go down a little that the mortgage payments will start to chip away at that principle. And of course it also depends on the housing market. Your house could go up in value, giving you more equity but there is also the possibility that it could go down in value and put you in a situation of being “upside down” on your mortgage. That is actually owing more on it than the house is worth. This is what happened to all those people when the housing bubble burst in 2008.   So with all that said, it will take a while before you will get enough principle back when you sell to offset the costs you put in when buying it. If you sell too soon you will not only not gain any money on the sale you could very well come out in the negative for your years of home ownership. If this is the case you would have actually have been better off to continue renting and saving your money. Next, other than that down payment you have saved up, how is your financial situation? Do you have any debts? If you do, it is very smart to pay them off before embarking on your homeownership journey. Do you have an emergency fund (of three to six month’s expenses) saved aside? I would recommend at least six month’s during this transition into home ownership as you never know what can happen. Is your job secure? You don’t want to take on all this extra monthly expense only to be caught high and dry with a loss of income. This type of scenario sends people scrambling and can result in a disastrous situation.  Even if your job is secure, you have a good down payment saved up and you know you will be staying put, have you crunched the numbers to see of you can afford the cost of homeownership? A common mistake people make is this line of thinking. “I am paying X (say $1,500 per month) on my rent so I might as well be paying that amount on a mortgage and actually owning my own home.” The trouble with that is that you must consider all the other costs of owning. Some things that were covered by your landlord before are now your responsibility. Have you thought about taxes, homeowners insurance, (PMI if you have a small down payment), electricity, heat, TV, internet, water, rubbish removal, etc.?  And in addition to all those fixed expenses, if the house is yours, you are now responsible for the upkeep. And no matter what great shape that house was in when you bought it, something always needs attention. Sometimes it seems barely a month goes by without an unexpected household expense. Even non-household expenses can derail you if you are “living on the edge”, just making all your monthly bills without a penny to spare. This is why it is so important to have that emergency fund set up before you move in.  Now what about that down payment? I just mentioned PMI in the previous paragraph. What is that that? If you put less than a 20% down payment then you have to pay Private Mortgage Insurance. And although you are responsible for these premiums this insurance does nothing to protect you. It is to protect the bank from losing the money they lent you should you default on your payments.    So, this brings us to my son’s question. How much of a down payment should you put down and how do you save up that kind of money? The answer to the first question is as much as possible, at the very least 20% (to avoid that PMI) If it’s home ownership you are after (and not living in a bank-owned house that you are paying dearly for (in interest payments) you should set your sights on the biggest chunk of money you can plop down.  Another way to keep your down payment at a higher percentage of the cost of the house is to buy a less expensive house. This way that same down payment you have saved is now a larger percent of the total cost. You can always move into bigger house (or expand the one you are in) down the line should the need arise and your finances improve. Here’s a dirty little secret the banks don’t want you to know. They will approve you of a mortgage that is really out of a comfortable price range for you. Why? Because they are really not interested in how comfortable you are making the payments. They are just looking to get the biggest mortgage for themselves (the more you borrow, the more interest payments they will get). So buy a house that you are comfortable with (monthly payment wise), not what the bank approves you for, and ideally this monthly payment should be no more that ¼ of your monthly income. And one more thing on the subject of mortgages. The bank will automatically default to a 30-year-mortgage, but you are much better off to get a 15-year. The quicker you can get that house paid off, the less total interest you will pay on it. You can save yourself many thousands of dollars (even hundreds of thousands) by just doing this one thing.  Now to Jesse’s question of how to save up for that mortgage. The same way I recommend you save up for anything else. Make it automatic! Open up an online account and set up automatic monthly payments going into it. Take the total amount you want to save and divide it by the months until you want to have the money. If you want to save up a $75,000 down payment in four years that would mean you need to save about $1,500 per month. *See Easy Peasy Make it Automatic  If your timeline for savings is actually more than five years then you might want to consider investing (all or part of) the money into a low cost (relatively safe) mutual fund (such as an S&P 500). Putting those payments away each month will also help you to be living below your income and able to make all those extra expenses when you do move into that house. Owning your own home is the American Dream. It is a great feeling to live in a house of your very own and can also be a real plus to your total financial picture if you are indeed prepared for it, but please make sure you are fully ready before taking the plunge or it has the potential for turning into a nightmare. Do it right and make it your dream come true!  Best of luck to you if you are looking to embark on this exciting new chapter of your story. Wishing you a bright future in your own home sweet home!   I have been talking in this space for years now with tips about how to save money and especially lately, of course, with so many people feeling the financial pinch of this Covid lockdown, saving money has become crucial. But someone posed the very legitimate question of where exactly they should be putting their savings. Some people just keep it in their regular (everyday) checking or savings account. That is not a good idea, and I will l explain why.  You (should) have more than one savings goal for your money, and keeping it in a lump sum actually tricks the mind into thinking you have more money than you do. And for some people this makes it very tempting to spend it. This is the other reason to keep it separate from your everyday money. Once you break it down into the various needs you have for your money you get a more realistic picture of how much you have and how much you still need to save.  Here is a breakdown of some goals you might have and where you should be putting the money for them: #1 Retirement: This can be a 401k or other workplace IRA account, or an IRA you have set up for yourself. At least 15–20% of your income should be going into that. Within that 401k or IRA, the money should be invested, of course. Low cost (index fund) mutual funds are fine. If you want to get fancier than that it is entirely up to you.  #2 An emergency fund: This is especially important in these uncertain times we are going through. If you don’t have a fully-funded emergency fund (at least 3–6 months-worth of expenses), money should be going into this each month. In fact, during this time you might want to beef this up even more. When you reach the 3–6-month goal (or more) then just leave that sitting in a separate account for when you need it. This should be a liquid readily accessible account (not invested).  ,#3 A car fund: Most people own a car and should always be saving towards the next one (paying car payments to yourself) so that you never have to finance one. Get off that car payment carousel! This will save you untold amounts of interest payments thrown away to the bank during the course of your lifetime. If you have no need for a car, then obviously this one does not apply to you,  #4 Other savings goals: I recommend you separate them out into separate accounts. This is anything else you are saving for, a wedding, down-payment on a house, home repairs, trip, kids college, etc.  For most of these savings I recommend you open up an online bank account (or more than one) and then set up automatic payments going into them (from your regular checking/saving account), calculating how much you will need for that goal and the amount of time you have to save for it. I suggest this for two reasons. One, the online banks have a slightly higher interest rate than brick and mortar’s do, and two, they are (at least psychologically) less accessible (out of sight/out of mind), so you will be less tempted to dip into them. And labeling them with a certain goal makes them more “off limits” to impulse spending too.  One more thing. If any of these goals is on a long-range timeline (you will not be needing this money for at least five years or longer), then you might consider buying a (low-cost index fund) mutual fund to be putting that money into for better returns. Since the market is volatile by nature, I would not recommend doing this for any shorter range goals as you risk losing (some of) your money. But for longer range goals, it is a pretty safe bet that, with the usual returns on the stock market, you are likely to do better with this money than putting it into a savings account.  So now you have an exact blueprint of where and how to save your money. Just plug in your particular goals and you can have the whole thing set up in one afternoon. And the beauty of this automatic savings is once it’s done you never have to think about it again. All you have to do is tweak it from time to time as your goals change (and/or are met). You can just get on with your life and stop stressing about money. And that’s what this whole money saving business that I’ve been teaching you is all about! 😀 A peaceful stress-free life!  Wishing you a bright, stress-free, peaceful life of savings!   This strange lockdown we have found ourselves in and the resultant loss or decrease in income has left many people to ponder their financial situation and ways they have been managing their money up until this point. As I mentioned in the previous blogs, some people are just now waking up to the need for setting money aside for times such as this. The idea of the emergency fund has resurfaced into people’s consciousness, and the term is being batted around quite a bit of late. So I thought I would dedicate this space to the topic.  First of all, what is an emergency fund, and why do we need one? The general consensus is that we should have about 3-6-months-worth of living expenses put aside, that is there to be used strictly for emergencies only. This money is best kept in an online bank account (slightly better interest rate) and completely separate from your everyday checking/savings accounts. The exact amount in there is up to you. If your income is very variable or otherwise unstable, then the larger amount (6 months) would be advised. Some people prefer to have even more than 6-months-worth if their income is very unstable, or they are very risk averse, or prefer more of a cushion. Everyone, no matter how stable they think their income is, should have at least 3 months at the bare minimum, because no matter how good things are going for you right now, “s#@t” happens!  The purpose of having that fund is to keep your finances from being derailed when the unexpected happens. If you have that cushion put aside you can just dip in, pay that medical bill, or home repair or live on it through a job loss and get right back on track where you left off without throwing your whole finances into a tizzy. And even more importantly you won’t be forced to reach into your wallet for the credit card and put yourself into debt over the situation.  Someone posed the question to me recently: “How do I determine when to take money out of my emergency fund?.” An excellent question, and that is why I chose to address it in this month’s blog. The bottom line is this, the more you budget for the unexpected, the less you will ever have to dip into your emergency fund. It’s as simple as that. So how do you determine when you really do need to break that piggy bank?  Before dipping into the emergency fund you should ask yourself: “Do I really need to use this money right now?” Do you have some time to save up the money that you need, and get by without it for a while. Can you get by without whatever the expenditure is altogether? “Is this something I really need to buy?” Can you borrow something (at least while you save up)? Can you make do without it in some other way? “Is buying this thing right now really necessary?” Maybe it’s not the “need” you think it is, but more of a “want”. “Is this purchase right now really worth the sacrifice it will take to replenish my emergency account?” “If I don’t spend the money right now on this emergency will this situation cost me more money in the long run?” (i.e. a car or house repair that will get worse if left unfixed). In that case, by all means, do it.  And after you have dipped into your emergency fund consider if this expense is something you should be adding to your monthly budget so that you are prepared for this type of emergency in the future (I.e. beefing up your “car repair” or “home repair” fund, or adding a new category to cover whatever the expense was).  Ideally, if you have budgeted for every possible “unexpected” expense that may come your way, your emergency fund becomes just a big fat luxurious cushion for you to sit on and enjoy the security of. Wouldn’t that be a nice feeling!  Wishing you a bright secure future!

Perhaps you have heard there is currently an epidemic of people in our country crippled under outrageous student loan debt. Some people are heading into retirement and still struggling to pay off their college loans. This is completely unnecessary. Don't end up like this!  I recently gave a talk at the local community center about the smart way to go about planning with your kids for their college so that they can get a degree with as little as possible, or better yet, no debt, and I realized that this is a subject that I have yet to address in this blog space. I would like to start off by saying that all four of my children have college degrees, one with a PhD, and not one of them has ever taken out a college loan. I don’t say this to brag, but rather to illustrate my point that it can be done and it’s not even that difficult to do. But you have to have the right mindset. And my kids did not even all follow the same “formula” to achieve this, but each found their own way to achieve their degree with no loans bogging them down at graduation time. When I say the right mindset, I mean to go into the college years with a clearheaded view of the objective, which is to obtain a college degree that will help launch you into a decent paying career. Some people have taken to making too big a deal about the “college experience” and to this I say it is only four years out of a young person’s life and not worth going into crushing debt for many years to come for some perfect college adventure or “high end” degree. You can pay a reasonable price for that degree and still have a good experience and some good times and you will have the rest of your life for adventures as well. So here are some things to consider when planning for those college years that can help in obtaining that debt-free degree:  #1. Keep the scales balanced – Be realistic in your approach to college. Do not go deeply into debt for a degree that will not lead to a lucrative career. Remember you are paying for a service. Keep your R.O.I. (Return On Investment) in mind. Make it your objective to avoid debt if at all possible #2. Getting ready for college - Get good grades - Earn college credits. Take AP courses and/or college courses at a reciprocal college during your high school years if your school offers them. - Get involved, follow a passion (do not just do a “checklist” of things to beef up your resume) - Give to your community in a meaningful way in line with your own interests and ideals. - Start looking for scholarships in sophomore year. Start applying in junior and senior year. - Look at both local scholarships and online scholarships.  #3. College Choice: - Be realistic. Go where you can afford! - Community college for the first two years - State schools - Only go to a private school if you get a very good scholarship (to bring it down to at or below state school tuition). Make sure that scholarship is guaranteed for the entire two or four years. - Do not get caught up in the prestige of a college name. After your first job or two it’s not really going to matter anymore where you attended college. It’s your job performance that will stand for itself. #4. Choose a practical major: - Do some research as to your options - What kind of jobs are available in that field? - What kind of salary can you expect to make? #5. Scholarships: - Apply to as many as possible - Use these websites to find online scholarships: Fastweb, or Niche.com. There are many more. - Ask the individual colleges about them. One of my sons applied for a scholarship that the young tour guide happened to mention on a college visit and won a four year full scholarship to that school! - Fill out the FASFA (some scholarships are tied to it) - Keep applying for scholarships even when you are in college  #6. Work! - While in high school - Over summers - While in college - Be entrepreneurial! Rather than work an hourly wage job (such as a cashier or flipping burgers) work for yourself. Even things like babysitting, dog walking, mowing lawns, or tutoring, tend to be more lucrative. If you have a special talent, use it. Give music lessons, make something to sell, help people with their websites. These types of jobs often pay more than the hourly wage jobs. - Be an RA after your freshman year ,#7. Housing: - Live at home if possible. One of my kids lived at home and commuted to two years of community college and then another two years at a local state school, all the while working at a grocery store and paid off the tuition as he went along. - Take all expenses into account if considering off-campus living (utilities, food shopping, transportation, etc..) - As for transportation, seriously consider not having a car through the college years, especially if you are going away to college. Most colleges have a decent mass transit system to get around the area. None of my kids that went away to college had their own car during those years and they got by just fine. - Embrace minimalism! Do not go crazy shopping for college housing “stuff”. If you look like this heading off to college, you spent too much:  #8. Food: - Meal plan-vs-grocery shopping? Carefully consider which would work the best for you and be the least expensive option. - If you take the meal plan, use it! Don’t pay for food not eaten. Every meal you paid for but did not eat is wasted money! - Limit eating out and take-out. - Cook your own food Brew your own coffee Drink water (get a reusable water bottle)  #9. Books - Do not buy college text books at full price. Use websites like “Chegg” and “Bookfinder” to buy used books or rent them. You can also download them (sometimes for free) on sites like the Google ebookstore. You can double your savings by sharing them with a friend taking the same class. #10. Graduate on time! - Do not take extra semesters to graduate, paying more for your degree than necessary. This is especially important If you are taking out any loans for your education. - In fact, try to graduate a year, or at least a semester early if you can. This is especially feasible if you have transferred college credits (i.e. AP courses) from high school.  Have a Bright (debt-free) Future!  |

Archives

June 2022

Categories

All

|

RSS Feed

RSS Feed