Sometimes there is just something to be said for boiling it all down into a nutshell and that is just what I have decided to do in this blog. This is pretty much says it all in seven easy-to-follow rules. The best time to start living these rules is from the minute you start that very first job. That is the time to set up good habits that will keep your finances healthy and thriving for your entire life and ultimately lead you on the path to that beautiful dream of financial freedom!  If you know anybody who is just starting out here is the perfect gift for them. Just print these rules out for them and you will have changed the trajectory of their life forever.  1. Always live below your income level (and be saving for retirement and goals). 2. Always be saving at least 15% of your income into your retirement account(s). 3. Always have an emergency fund set up of at least 3–6 months' worth of spending. Your Emergency Fund questions 4. Keep track of all your spending. Know where your money is going! 5. Learn to distinguish wants-vs-needs. Many things that we think of as needs are actually wants. Don’t buy wants if you can’t afford them. 6. Never buy anything on credit (including cars). No Loan Auto Ownership. Save up and pay for things with cash. One exception to this would be a mortgage on a house but put a hefty downpayment down. Get a 15 yr fixed rate mortgage and pay it off ASAP. 7. Pay yourself first! Put your savings on Automatic Pilot. Set up an online bank account (or a few) to save up for your future needs. It’s better if you can have a separate one for each goal (i.e the car account, the wedding account, the vacation account, etc.) Set up automatic payments going into them each month from your checking or savings account. You really can’t go wrong if you live by these simple rules. They're not that hard to do! Wishing you all a very bright future!

1 Comment

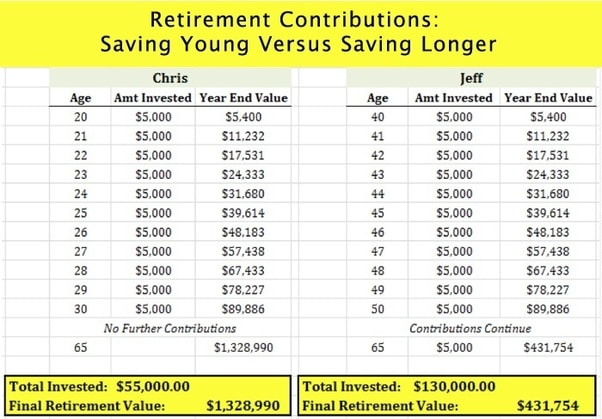

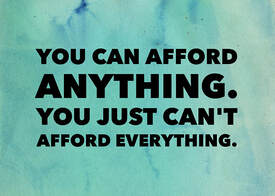

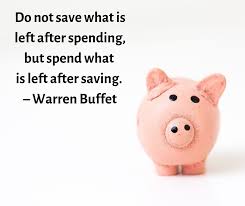

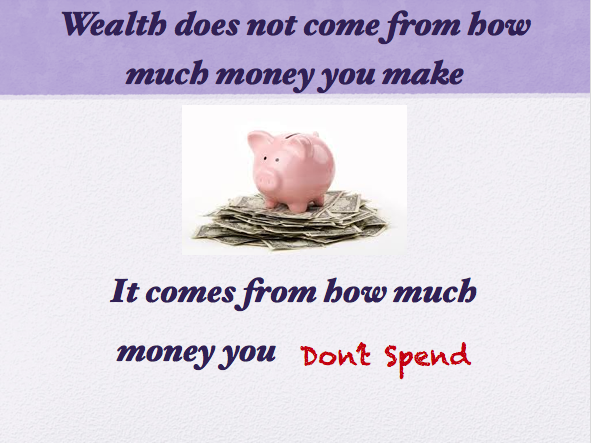

I’ve seen or heard this question posted in many different ways throughout the years, the gist of it being that one needs to make a fundamental decision between enjoying their life or saving for the future. I’ve heard the argument that you must “live” for today because you could be hit by a bus tomorrow. Young people have screamed YOYO! (Did I just coin that?), as in, “You’re Only Young Once”. They maintain that they must spend and “live” for today while they are young enough to enjoy it.  But I don’t see it as a black and white, either/or situation: Save OR have fun. I believe that if you are wise with your money you can do both. Saving your money does not mean that you have to be a miserly scrooge sitting in your lonely attic counting your money and never having any fun. In fact, with a little planning and wise money management you can easily have a very pleasurable life and also save for your future at the same time.  The one equation that people need to let go of is “Spending Money = Fun.” There may be some correlation to that sometimes, but it is certainly not a given. You can spend lots of money on something and have a terrible time, and even more importantly it is very possible to have a great time spending no money at all. I’m sure you can think of several examples of both these facts in your own life. Let’s start with the young (my newly coined YOYO philosophy). Yes, they can certainly save and also have fun. First of all, they have one huge advantage in their favor… the magic of compound interest. The fact is if you start saving (investing) early you will only need to save a fraction of your own money in order to build up a very tidy nest egg for retirement. Most of the money in your IRA at retirement will be growth on the returns you accrued through the years (not the money you actually put in). Pretty neat trick, huh?  With a little prioritizing and forethought young folks can also be saving for their other more near-future needs/wants (a car, a house, a wedding, et.) by putting those savings on automatic pilot and just living on what’s left. The prioritizing comes in as you make the conscious decision to forego (instant pleasure X) which is not really adding a great deal of joy to your life in order to save up for that something that will bring you great pleasure indeed.  The one joy that seems to be mentioned a lot is traveling. And here is where the young have another distinct advantage. They can travel for practically nothing, staying in youth hostels, or other low cost accommodations. There are even many temporary internship/job opportunities overseas that can allow them to see the world while sometimes even making a little money. The possibilities of low-cost travel are only limited by the imagination for the young (or young at heart). Google “traveling on next to nothing” and see what you come up with. I read a great memoir on the subject a while back called “No Baggage – A Minimalist Tale of Love and Wandering” by Clara Bensen.  What about if you are not young? I see people of all ages squandering their money on daily instant gratification pleasures without even realizing that they are doing it. Once, when I was telling some friends about a trip to Singapore that I had just returned from, somebody asked me “I don’t understand. You can’t afford cable TV, but you can afford a trip to Singapore?” My answer to that is you can afford anything (within reason, of course), but you can’t afford everything. I chose to forgo all those channels at $150/month in order to save my money for something better. I even found a way to get TV for free (an old fashioned roof antenna). I also put my frugal skills to use to make the trip possible without breaking the piggybank.   If fun is your priority, then go ahead and have it! Have as much as you want. Live! Take advantage of all that free fun that is out there for the taking. If there is some kind of fun that you must have money for, then just look at your spending habits and give something up that does not bring as much joy and save up for what you want.   I see absolutely no reason why you can’t do both. Save and have fun! After all, you only live once!  Wishing you a happy life today and a bright future tomorrow!   I have been talking in this space for years now with tips about how to save money and especially lately, of course, with so many people feeling the financial pinch of this Covid lockdown, saving money has become crucial. But someone posed the very legitimate question of where exactly they should be putting their savings. Some people just keep it in their regular (everyday) checking or savings account. That is not a good idea, and I will l explain why.  You (should) have more than one savings goal for your money, and keeping it in a lump sum actually tricks the mind into thinking you have more money than you do. And for some people this makes it very tempting to spend it. This is the other reason to keep it separate from your everyday money. Once you break it down into the various needs you have for your money you get a more realistic picture of how much you have and how much you still need to save.  Here is a breakdown of some goals you might have and where you should be putting the money for them: #1 Retirement: This can be a 401k or other workplace IRA account, or an IRA you have set up for yourself. At least 15–20% of your income should be going into that. Within that 401k or IRA, the money should be invested, of course. Low cost (index fund) mutual funds are fine. If you want to get fancier than that it is entirely up to you.  #2 An emergency fund: This is especially important in these uncertain times we are going through. If you don’t have a fully-funded emergency fund (at least 3–6 months-worth of expenses), money should be going into this each month. In fact, during this time you might want to beef this up even more. When you reach the 3–6-month goal (or more) then just leave that sitting in a separate account for when you need it. This should be a liquid readily accessible account (not invested).  ,#3 A car fund: Most people own a car and should always be saving towards the next one (paying car payments to yourself) so that you never have to finance one. Get off that car payment carousel! This will save you untold amounts of interest payments thrown away to the bank during the course of your lifetime. If you have no need for a car, then obviously this one does not apply to you,  #4 Other savings goals: I recommend you separate them out into separate accounts. This is anything else you are saving for, a wedding, down-payment on a house, home repairs, trip, kids college, etc.  For most of these savings I recommend you open up an online bank account (or more than one) and then set up automatic payments going into them (from your regular checking/saving account), calculating how much you will need for that goal and the amount of time you have to save for it. I suggest this for two reasons. One, the online banks have a slightly higher interest rate than brick and mortar’s do, and two, they are (at least psychologically) less accessible (out of sight/out of mind), so you will be less tempted to dip into them. And labeling them with a certain goal makes them more “off limits” to impulse spending too.  One more thing. If any of these goals is on a long-range timeline (you will not be needing this money for at least five years or longer), then you might consider buying a (low-cost index fund) mutual fund to be putting that money into for better returns. Since the market is volatile by nature, I would not recommend doing this for any shorter range goals as you risk losing (some of) your money. But for longer range goals, it is a pretty safe bet that, with the usual returns on the stock market, you are likely to do better with this money than putting it into a savings account.  So now you have an exact blueprint of where and how to save your money. Just plug in your particular goals and you can have the whole thing set up in one afternoon. And the beauty of this automatic savings is once it’s done you never have to think about it again. All you have to do is tweak it from time to time as your goals change (and/or are met). You can just get on with your life and stop stressing about money. And that’s what this whole money saving business that I’ve been teaching you is all about! 😀 A peaceful stress-free life!  Wishing you a bright, stress-free, peaceful life of savings!   I have talked a lot in these blogs about the what’s and how’s of scrimping and saving for a “rainy day” but today I’d like to talk about the why. That glorious goal! In order to keep your spending under control and not keep living for that constant instant gratification it’s important to keep sight of the dream.  What kind of a vision do you have? What would you do if you had money? When you have your ideal future visualized, it’s much easier to give up all those pricey extravagances that you feel you must treat yourself to regularly. Be specific, really immerse yourself in the dream. If you have a life partner have fun dreaming together. It makes for fun dinnertime or cocktail hour conversation. Would you buy a nice house somewhere? On the beach? In the mountains? Go on an adventure? Buy a motor home and tour the country? Travel to other parts of the world? Treat your family (and future grandkids) to some fun vacations? Save photo’s that you would like your life to look like someday.  Just think how nice it will be to be able to look forward to your retirement years rather than start panicking as the time approaches, wondering how you will live when the paychecks stop coming. It will be such a wonderful feeling to look forward to those golden years knowing that you have enough to live on and then some. Think how nice it would be to have enough money put aside so that you never have to work again. If you do work it will be on your own terms at something you enjoy doing.  It really isn’t that hard. The earlier you start, of course, the easier it will be. But even if you didn’t start early you can start right now and you will be amazed at how quickly the money can add up when you are putting it away at a steady automatic rate and investing it for that compounding interest. So, go ahead and dream! Dreams can and do become reality!   You’ve all heard the expression “April flowers bring May Flowers” I’m sure. But what does it mean? Well in its literal sense of course, we need the rains of early spring to give us those beautiful flowers to enjoy in May. But what is the deeper meaning of the phrase beyond that? When we say it we are talking about how we are willing to put up with some less desirable weather in April because we know it is necessary so that we may delight in the lovely blooms that follow. But we can also apply the phrase to other situations in life. Very often it is easier to endure a less than pleasant circumstance because we know it is essential for something better to come. The financial guru Dave Ramsey has a great saying “Live like no one else so you can live (and give) like no one else later on.” In other words, if you have a future financial goal in mind you will be willing to make the sacrifices that it takes right now in order to attain them. You appreciate the showers because you know they will result in a richness of flowers.  Are you a grasshopper or an ant? The grasshopper will ignore the future and just live for today only to be surprised when winter comes and he has nothing put aside to get him through the cold snowy months. Meanwhile, the ant has been working throughout the summer to build up a stash to sustain her throughout those food barren months. Does this mean that the ant has no fun while he is preparing for the future? Absolutely not! There are a great many ways that that little ant can have fun while also taking the time to put those resources away for that rainy day. But the wise little ant always keeps in mind that winter is coming and does what she needs to do to be prepared.  So, yes, enjoy yourself for today. There are any number of ways that you can enjoy life for very little cost or for free. But if you are a wise little ant you will always be stocking up for the future so that (unlike that silly irresponsible grasshopper) when the future comes you will have an abundance to enjoy and your winter will be more like a gorgeous phantasmagorical riot of spring blossoms. Because you, my little friend, prepared for it.   Here’s the biggest mistake almost all people make when it comes to savings: They pay their bills, buy their food, make repairs, buy things for the house, pay for kid’s activities, go shopping for clothes, go to the movies, go out to eat, go shopping for some new clothes, etc., etc., and then save what’s left over at the end of the month. Can you see the problem with this? Is there ever anything left at the end of the month?? Many people will also say that they live paycheck to paycheck, but here is the interesting thing about this; They are saying this no matter what the size of their paycheck. The person who makes $300/wk. is saying it and so is the person who makes $600/wk. and the one who makes $3,000/wk. and on up. Right up to that athlete or rock star who is making several million dollars a year and blowing it all, only to go bankrupt when the income dries up. It seems to be just human nature to live just up to your income level whatever that may be, or even a little above that (accounting for all the debt people tend to find themselves in). But if you want to save money the only way you can do it is by living below your means, whatever they may be. Another way to put this is: You don’t save money by how much you make, but by how much you don’t spend. The great investment “guru” Warren Buffet puts it this way:  This is great advice, but how do you do it? Well the great US of A knows how. You pay taxes every year, right? Does Uncle Sam just let you have your full pay and then ask you to cough up the taxes on April 15th? You bet your sweet bippy he doesn’t, because he knows what would happen. People adjust their lifestyle to however much money is coming in. So he just takes his cut up front and people adjust to living on what’s left. Well you can do the same thing for yourself. Just take it off the top. The U.S. government even gave people a means to do just that by starting the 401K program, giving you a tax advantage and a way for you to save money by skimming it right off your paycheck without even ever seeing the money. If you have this offered at your place of employment you should certainly be taking advantage of it. Some generous companies will even match your contribution dollar for dollar up to a certain amount. Free money! Never pass up this opportunity! But even if you don’t have the opportunity for a 401K (or 403B, TSP, etc.), you can still make the magic of automatic savings work for you. All you have to do is set it up once for yourself and done. Savings skimmed right off the top. Out of sight, out of mind. You will quickly adjust to living on what remains. How you set this up depends on what you are saving for. Your first savings goal should be your retirement. I know this sounds kind of backward or counterintuitive, but because you need such a large amount, and because it makes such a difference when you start compounding that interest early, it is imperative that you start this ASAP! If you don’t have a 401K then you can set up your own retirement account in a Roth IRA. I recommend you do this by opening up a discount brokerage account at a firm such as Fidelity or Vanguard. This gives you many options on what to invest your money in inside of your Roth IRA and gives you complete control over it. Once you have your Roth set up it is quite simple to set up automatic payments of whatever amount you choose monthly going from your checking account into your IRA. Whether you have a 401K in the workplace or your own Roth IRA, you can also set up similar automatic payments going into (online) savings accounts for your other savings goals (wedding, car, house down payment, education, etc.) Once you have your savings goals set up automatically in this way, you no longer have to stress about money. You are all set for your future needs both short and long-term, and you can spend what’s left freely. Won’t that be a nice feeling!  |

Archives

June 2022

Categories

All

|

RSS Feed

RSS Feed