Many people tend to view the holidays as a time of abundance and exuberant gift giving. They equate the season with bountiful shopping and lavish piles of gifts. And while I understand the spirit of generosity and kindness that this custom represents and originates from I can’t help but feel that it has lost something through the years as it has been taken to the extreme.  Of course, being the frugalista that I am, I first must note that, for one thing, it “inspires” (forces?) people to spend beyond their means. So many people today are going into debt for the sake of (the societal pressure to create) a lavish holiday. Do you regret the bills in your mailbox come January? Are you able to pay them off? You can read more in my December 2018 blog about how to have a festive holiday without the debt hangover.  But it goes even beyond the new year regrets. How does this excessive holiday feel to you? Most people report feeling frazzled and stressed out and overwhelmed trying to pull it off. So then, what is the point of it all? Is it for the children? Well, I can tell you right now that children’s happiness not only is not dependent on how many gifts they receive, but is, in fact, negatively impacted by over abundance. They are actually more appreciative of a few well thought-out gifts than a mountain of “stuff." And what message are you sending them with all this “generosity?" Does the word “spoiled” have any meaning to you?   So, if you are currently wrung out by all the stress and overindulgence of the past month, and you are dreading facing those bills in the mailbox come January, it may be time to consider another way next year. Just try it. I think you will be pleasantly surprised.    Wishing you all joy, peace, and contentment at the holidays and always

0 Comments

I spoke on these pages last year about how thankfulness affects your budget and spending habits, so I will not reiterate that (though it bears repeating not only every Thanksgiving but also every day of your life. Read more about that here) This year for the Thanksgiving season I would like to explore another food related topic and blow a common misconception right out of the (over-fished) water. It is often said that eating healthy is expensive. This is one of the usual arguments I get from people when I implore them to save money on their groceries.  I have always been all about eating for less, and have also been mindful of eating a healthy nutritious diet. Rarely has there been a dilemma about choosing one over the other for me. But recently I have discovered that not only is it not more expensive to eat healthily, it is in fact, much cheaper to eat a healthier diet. I have always been a pretty healthy person but I do have a family history of diabetes and heart disease so when my blood test #’s started creeping up I knew it was time to take more serious action to avoid those golden years full of drugs, tests and procedures.  I did a lot of reading on the subject of what kind of diet and lifestyle changes can help control this metabolic syndrome that can lead to an impaired existence in later years, and found the research coming time and time again back to one conclusion: The best diet (for just about any health problem you have) is a vegan diet.  Now I am not really a stranger to that way of life. Two of my kids are vegetarian and the one that lives with me is vegan. So I have a head start in knowing how to cook without meat and even to some extent without dairy products and eggs. Never the less, it is somewhat of a learning curve to eat like that on a daily basis. But we are finding more and more that it is quite easy to come up with delicious meals that contain no meat or dairy, and not feel deprived in the least. Yes, I said we, my husband has quite willingly come on this transformative journey with me. We are not completely there yet. We do occasionally “cheat” and use a dairy product in a dish. And we are still using up the meat that is in our freezer, having it in small portions once every 2 weeks or so. But we have come a long way in the process and feel that we will be eating a totally vegan diet for the most part in a short time.     I am not writing about all this to get on any high horse about veganism. Although I have also, in the process of my research, discovered just how healthy it is for the planet (and of course the lives of the animals) as well. But the real surprise that I would like to impart on these pages is the effect on our food budget! Think about it for a moment. The most expensive items you put in your grocery cart are the meats and dairy products. When you eliminate them your bill goes way down!  The trick is (and I think this is where the “expensive to eat healthy” myth comes from) is not to replace that meat and dairy with specialty “health foods” and vegan “meat” substitutes. We just buy (and eat) basic inexpensive ingredients like rice, beans, legumes, quinoa and other grains, pasta, potatoes (white and sweet), oatmeal, vegetables and fruits. And our (already low by most people’s standards) food bill has dropped to practically nothing!  Cheap and healthy (and delicious, I might add), it’s a win, win, (win) all around! How can you beat that! And we will also save on health bills in the long run. Add another win to that last sentence!  So a little food for thought for you to contemplate this Thanksgiving season. Bon Appetite! Wishing you a wonderful holiday and a bright future!   Experiment! Try some vegan recipes here

Read these books about how a vegan diet can change your health : The Starch Solution by Dr John McDougall Food over Medicine by Pamela Popper  I know I am dating myself here, but back when I was a wee lass, Halloween was a simple holiday, simply for kids. And when I say simple I mean that a few weeks before October 31st, we kids, (not our parents) would start thinking about what we wanted to dress up as for Halloween. Then we would scrounge our closets and other parts of the house for things we could use to accomplish our goal. There were usually things like cardboard boxes, tin foil, old clothes of our parents, yarn, fabric scraps and other such items involved. If our parents went all out and bought us a costume, it would be this thing that came in a 12” x 12” box consisting of a flimsy cover-up with a picture on it to represent what we were supposed to be and a cheap mask with a rubber band in the back to hold it on, like this:   These are way more ambitious homemade costumes than we ever came up with. LOL! Very clever! On Halloween day itself we would rush home from school, put our costume on and head out with an old sheet or grocery bag to go around the neighborhood trick or treating. We would be home by dinner to review, organize, and trade our loot and that was it. Halloween over. As for decorations, maybe we would have a few cardboard cutouts of pumpkins, or bats, or ghosts, that we would tape on to our door or windows. And these we saved and used year after year. Oh, and the adults did not celebrate at all. They were not really involved other than to help us with our costume, if we asked, and buy and give out the candy for the trick-or-treaters. Fast forward to today and it (like almost every other holiday, and so many things in our society) has become a multibillion dollar industry that goes on for an entire season.  Now I know I am sounding rather curmudgeonly here and don’t get me wrong I am not against people having fun for Halloween, adults included. I am just saying that if you are in debt, or not saving enough, it would be prudent on your part to reign in the holiday spending. Even my own (frugal) family has gotten into the spirit. When my kids were little we began hosting a spooky bonfire party each year at this time, adults included, which even though my kids are all adults now, we still often continue to this day. As I said we held our annual Halloween event, but I never went crazy with the spending. Since I knew it would be happening I kept it in mind all year long when I was shopping at yard sales and thrift shops. And I would take a look for clearance sales in the stores in the days after Halloween. And, of course, I would save things and use them year after year. I would also pad the decorations with things I had around the house, such as many candles in jars. Even Christmas lights can work for a spooky effect. I would recycle old halloween costumes into creepy scarecrows strategically placed around the yard. My kids would often put together a haunted house or trail, also cleverly using whatever household things they could find. For instance, one year “Dr. Ner’do well’s” lab contained body parts in jars, A cauliflower for the brain, grapes for eyeballs, chicken bones for fingers, etc.    We also invited everyone to come prepared with their favorite scary story to tell as we sat around the fire. Free frights and chills for everyone!  So I think you can see what I’m getting at here. I don’t think we will ever be getting back to that simple sweet Halloween of my childhood years but there are still many ways to get into the spirit and have tons of spooky holiday fun, adults included, without giving up your hard earned money. A little imagination can go a long way towards making your piggy bank happy and still making your Halloween spooktacular!  The author and a friend in our homemade costumes at last years bonfire party.  Happy Frugal Halloween!

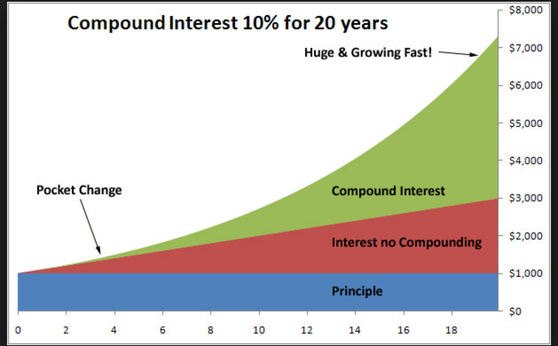

Perhaps you have heard there is currently an epidemic of people in our country crippled under outrageous student loan debt. Some people are heading into retirement and still struggling to pay off their college loans. This is completely unnecessary. Don't end up like this!  I recently gave a talk at the local community center about the smart way to go about planning with your kids for their college so that they can get a degree with as little as possible, or better yet, no debt, and I realized that this is a subject that I have yet to address in this blog space. I would like to start off by saying that all four of my children have college degrees, one with a PhD, and not one of them has ever taken out a college loan. I don’t say this to brag, but rather to illustrate my point that it can be done and it’s not even that difficult to do. But you have to have the right mindset. And my kids did not even all follow the same “formula” to achieve this, but each found their own way to achieve their degree with no loans bogging them down at graduation time. When I say the right mindset, I mean to go into the college years with a clearheaded view of the objective, which is to obtain a college degree that will help launch you into a decent paying career. Some people have taken to making too big a deal about the “college experience” and to this I say it is only four years out of a young person’s life and not worth going into crushing debt for many years to come for some perfect college adventure or “high end” degree. You can pay a reasonable price for that degree and still have a good experience and some good times and you will have the rest of your life for adventures as well. So here are some things to consider when planning for those college years that can help in obtaining that debt-free degree:  #1. Keep the scales balanced – Be realistic in your approach to college. Do not go deeply into debt for a degree that will not lead to a lucrative career. Remember you are paying for a service. Keep your R.O.I. (Return On Investment) in mind. Make it your objective to avoid debt if at all possible #2. Getting ready for college - Get good grades - Earn college credits. Take AP courses and/or college courses at a reciprocal college during your high school years if your school offers them. - Get involved, follow a passion (do not just do a “checklist” of things to beef up your resume) - Give to your community in a meaningful way in line with your own interests and ideals. - Start looking for scholarships in sophomore year. Start applying in junior and senior year. - Look at both local scholarships and online scholarships.  #3. College Choice: - Be realistic. Go where you can afford! - Community college for the first two years - State schools - Only go to a private school if you get a very good scholarship (to bring it down to at or below state school tuition). Make sure that scholarship is guaranteed for the entire two or four years. - Do not get caught up in the prestige of a college name. After your first job or two it’s not really going to matter anymore where you attended college. It’s your job performance that will stand for itself. #4. Choose a practical major: - Do some research as to your options - What kind of jobs are available in that field? - What kind of salary can you expect to make? #5. Scholarships: - Apply to as many as possible - Use these websites to find online scholarships: Fastweb, or Niche.com. There are many more. - Ask the individual colleges about them. One of my sons applied for a scholarship that the young tour guide happened to mention on a college visit and won a four year full scholarship to that school! - Fill out the FASFA (some scholarships are tied to it) - Keep applying for scholarships even when you are in college  #6. Work! - While in high school - Over summers - While in college - Be entrepreneurial! Rather than work an hourly wage job (such as a cashier or flipping burgers) work for yourself. Even things like babysitting, dog walking, mowing lawns, or tutoring, tend to be more lucrative. If you have a special talent, use it. Give music lessons, make something to sell, help people with their websites. These types of jobs often pay more than the hourly wage jobs. - Be an RA after your freshman year ,#7. Housing: - Live at home if possible. One of my kids lived at home and commuted to two years of community college and then another two years at a local state school, all the while working at a grocery store and paid off the tuition as he went along. - Take all expenses into account if considering off-campus living (utilities, food shopping, transportation, etc..) - As for transportation, seriously consider not having a car through the college years, especially if you are going away to college. Most colleges have a decent mass transit system to get around the area. None of my kids that went away to college had their own car during those years and they got by just fine. - Embrace minimalism! Do not go crazy shopping for college housing “stuff”. If you look like this heading off to college, you spent too much:  #8. Food: - Meal plan-vs-grocery shopping? Carefully consider which would work the best for you and be the least expensive option. - If you take the meal plan, use it! Don’t pay for food not eaten. Every meal you paid for but did not eat is wasted money! - Limit eating out and take-out. - Cook your own food Brew your own coffee Drink water (get a reusable water bottle)  #9. Books - Do not buy college text books at full price. Use websites like “Chegg” and “Bookfinder” to buy used books or rent them. You can also download them (sometimes for free) on sites like the Google ebookstore. You can double your savings by sharing them with a friend taking the same class. #10. Graduate on time! - Do not take extra semesters to graduate, paying more for your degree than necessary. This is especially important If you are taking out any loans for your education. - In fact, try to graduate a year, or at least a semester early if you can. This is especially feasible if you have transferred college credits (i.e. AP courses) from high school.  Have a Bright (debt-free) Future!   Having spoken with a few millennials lately, including one young lady who was very motivated to get started on the right financial footing, (this is not always the case with the young people I encounter), I thought I’d devote this blog entry to those just starting out on their lives’ journey. This is the stuff that I wish somebody had told me when I was just starting out. I figured it out along the way, but it would have been nice to know it all from the beginning. And some people, unfortunately, just never do figure it out for themselves. Would I have listened? Who knows? But, as they say, if I knew then what I know now, and followed the advice I am about to impart to you, I would very easily be a multi-millionaire by now. And you can be too. Anyone can do it.  Often I find myself very frustrated that young adults, who have the most to gain from learning to be smart with their finances, can be the most resistant to hearing (and following) it. And the sad thing is that if they don’t do it now, although they can still do alright whenever they decide to start, they can never make up for that lost time and the money they could have made by investing early. The magic of all those years of compound interest can never be regained.   So, without further ado, in a nutshell, here are my most salient tips for millennials: #1. The golden rule of finance: Always, Always, Always Live Below Your Means! Start out that way and get used to it. As your income increases you can increase your lifestyle, but always stay below what you are making. 15% of your income should going into your retirement fund at all times.  #2. The other golden rule of finance: Pay Yourself First! You will be paying out a lot of your hard earned money to other people and businesses in your lifetime (your landlord, the mortgage bank, electric company, insurance companies, gas company, food producers, goods manufacturers, health care providers, etc., etc., etc.,…..), but don’t give all your money away to other people or you will have nothing to show for it. Always be keeping something for yourself… up front, before any of your money goes out to anyone else.  #3. Make it Automatic Set up that money to go into your retirement account (401k or Roth IRA) and your other savings (goal) accounts straight out of every paycheck before you even see the money. Out of sight, out of mind.  #4. Keep track of your expenses Set up a system so that you know exactly how much you are spending, every day, every month, every year, and on what. You can do this by hand (simply writing it down) by computer (i.e. your own spread sheet) or with a website (such as mint.com)  #5 Prioritize your budget: Spend your money on what is most important to YOU First comes dire needs, housing, food, transportation, etc. Then prioritize the rest according to your income and needs. Wants come last, and only if you can afford them. Think carefully about wants-vs-needs. Do you really want to sabotage your future goals for some frivolous indulgences today?  #6 Plan for your goals Write them down and save for them systematically (how much do you need to save and when do you want it?). Do you want to get an education? Plan a wedding? Buy a house? Buy a car? Go on a vacation? Always be saving for your future purchases so that you will… (see #7)  #7 Never borrow money! (AKA buy things on credit) Don’t get into the interest paying trap. It is a slippery slope once you start on the debt quagmire. This includes education (student loans), cars (car loans), and those insidious credit cards. Always save up and pay for things in cash. If you don’t have the money, you can’t afford it. The only possible exception to this is buying a house. But even here, if you can manage to save up and pay cash that would be awesome. People do it. I did it for my second house (after I paid the first off by ten years). Certainly aim to put down as large a down-payment as you can and take out a 15-year mortgage. Then (pre)pay that down as quickly as possible. And don’t buy a more expensive house than you can afford. Though the lending banks will pre-approve you for a much bigger mortgage than you can comfortably afford, don't fall for it.  It’s really as easy as following these 7 very simple rules and you will be set for life. It’s not rocket science. Anyone can do it, at any income level. Stick with this lifestyle and you will go from millennial to millionaire, a very bright future indeed!  Which one are you? Hopefully in the green!  You can do it!!

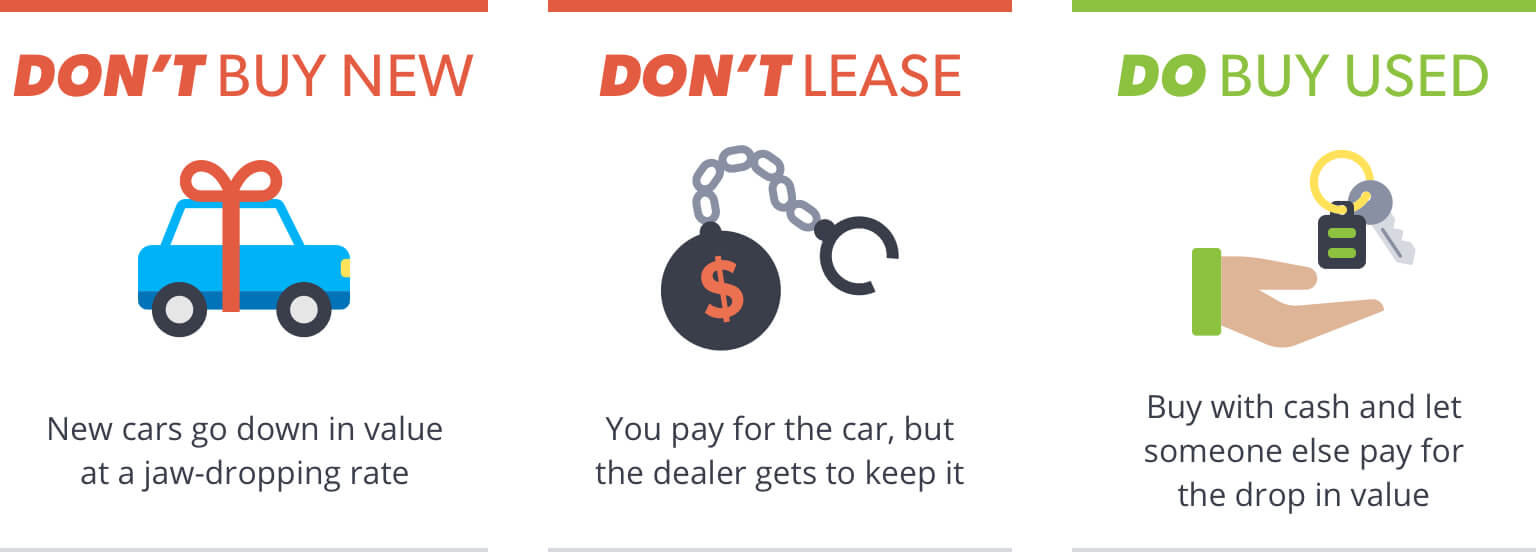

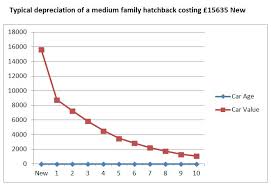

Since I am currently in the market for a “new” car, I thought I would share with you how I do not nor have I ever had a car loan. It’s quite simple if you start from the beginning but wherever you are in your auto ownership journey you can start at this moment and work your way up and out of car loans for good.  What’s wrong with car loans you say… isn’t financing a car the “American way"? Who doesn’t have a car loan? Well I don’t, for one, and I would wager a guess that every “Millionaire Next Door” doesn’t either. And yes, you’re right it has become the “American way” but which Americans are benefiting from that? Hint: It’s not you, the proud recipient of the car loan. It is the almighty bank (or sometimes the car dealerships) that are winning in this drive-now, pay-later arrangement. And the amazing thing is that they have you hoodwinked into believing that they are doing you a favor by getting you into the best car they can for low money down and easy monthly payments. Wow! What a nice guy… NOT! Believe me, car dealers are not in the business of doing you a favor. The only thing they are interested in is their own bottom line. The biggest best car they can sell you lines their own pockets, and getting you to take a loan from them (instead of the bank) is just more icing on the cake. And if you have ever been car shopping lately you will notice that they (subtly or maybe not so subtly) will start touting the glories of leasing a car. This is like taking a car loan on steroids (for them). Think about it. You pay a down payment (maybe $1,000) and then “easy” monthly payments of $299/month, and at the end of the three-year lease you are out $11,764 and you own absolutely nothing! You can now either give the car back and start all over again or pay some exorbitant fee (on top of the almost $12,000 you’ve already paid) to now own the car. You could have bought a (used) car for $11,764 three years ago and still had plenty of life left to it for years to come. And if you financed your car, let’s look at one example of how much you are actually paying for that car by the end of the loan period: If you take out a loan for $25,000 at 4.5% for a 60-month term, your monthly payments will be $570 and at the end of the term you would have paid out $27,364. A total of $2,364 lining the pockets of whoever held your loan. Nice! … For them. How do you feel about giving them all that “free” money? Would you like an extra two thousand in your bank account? But, you tell me, “I don’t have the money to just purchase a car outright.” Well, I can tell you that on a modest income I have never taken out a car loan to buy a car. How did I do it? Well, I bought my very first car for cash and from that point forward I was saving the money (that most people are paying out for car loans) to purchase my next car for cash. Most of the cars were used, at least a few years old, but I did make the mistake of purchasing two of them brand new (all for cash). No loans. If you can afford car payments you can afford to save up for a car!  Now I have instructed my kids to follow my principles. They each saved up for their first car (with a little help from me at times) and bought them (used) for cash. Then I told them to pretend (like many of their peers) that they have car payments, but pay them to themselves. And now through the magic of online bank accounts it was easy for them to set up a “car account” with $200 or $300 a month being automatically deposited into it from their checking account. And with that very modest “car payment,” if they take good care of the cars they have, in 10 years-time they will have between $24,000 and $36,000 towards the (cash) purchase of their next car. And even more than that, really, because instead of paying interest to a car loan, they are making interest on their bank account. It may be only 2% at the moment, but it sure beats paying out at 4% or more! But if you haven’t done that from the beginning and you are currently saddled with a car loan, then the best thing you can do is keep the car after your loan is up for as long as you can, and here’s the important thing: Keep paying those monthly car payments but pay them to yourself so that when you are ready for your next car you will have a chunk of change sitting there for your purchase.  And why do I say I made the “mistake” of buying a few of my cars brand new? Because the depreciation curve is enormous in the first year or two of car ownership and the bulk of that depreciation takes place in the first 5 minutes of car ownership. The minute you drive that sparkly new car off the lot you have dropped a couple of thou off its resale value. Ouch!! Let someone else take that depreciation (thanks first car owner!). Save yourself a couple of thousand dollars and buy a car that’s at least a year or two old.  So, now I will head out to the dealerships. You can buy a car from an individual for less money, but I like the assurance of having the dealer in case something goes wonky with the car a short time after I buy it. And even though I am paying cash I will still keep in mind that (friendly as they are) the dealer is not my friend. I will do my homework and check out any cars I am considering online, for any issues and the prevailing price for that year’s model. You can try Kelly Blue Book or Edmunds for this info. Then I am prepared to bargain (with the mysterious “manager” in the back, that my dealer will be consulting). I may walk away from the deal two or three times before I am satisfied that I am getting a rock bottom price. Of course the dealer has to make some money on the deal. I don’t begrudge him that. I just want to feel that I got a fair deal. Wish me luck as I head out in search of my next set of wheels and I hope you too will someday enjoy the joys of owning your own set of wheels without those pesky loans dragging you down.   Do you need a vacation? And can you afford one? Well those are two very different questions. The answer to question one? Hmmm . . . need? I would say in Maslow’s hierarchy of needs it would be pretty low down on the list. But do you want a vacation? Well, that’s an entirely different question! As for the second question, the simple answer is if you have the money to pay for it upfront (and are not taking this money from a more pressing need), then you can afford it. If you need to finance the cost, then no, you cannot afford it. So what can you do to make it more affordable? Ahhh… well that’s where I come in! A thoughtfully planned out vacation does not have to break the piggy bank. If you are aware of your budget up front, which you are, since you have put the money aside for it, there are many tricks and tips you can use to keep it affordable. If you are going to whip out the plastic to book it and then again all through the trip you can easily lose track of how much your spending is racking up to. Once the vacation is over, is that one week of relaxation worth the stress of having to pay it off until the next round of big spending at the holidays?  So, that said, you will start by planning a vacation that you can realistically afford. The purpose of vacation time is to relax and enjoy yourself. Personally I find that life is more relaxing and enjoyable when I staying in control of my expenses and living below my means. I think you will too. Here are some step by step tips to make any vacation more enjoyable and affordable, starting with planning and throughout the days of your trip.  ,Planning: Of course the first step is to be realistic about what kind of vacation you can afford on your budget. If you have $2,000 to spend, you are not going on a six week trip around the world. But can you do something fun on a smaller budget? Absolutely!! Take a little time to think about your priorities? What is the best thing about vacation time for you? Sightseeing? Beach time? Activities? Relaxation? Time with the kids? You may not be able to do everything, but you should be able to hit a few of your priority choices. Half the fun of a vacation is actually in the planning stages. Talk about your vacation dreams with the people you will be vacationing with. Have fun with it! Which of them might you be able to actuate on your next vacation? While you’re at it, daydream about future vacations. There is great pleasure to be had in just the dreaming alone!  Accommodations: The time to book is as early as possible, again keeping your budget in mind. If you can’t afford a motel, camping might be the way to go. If you can’t afford to travel, keep it close to home. See if you can lock in a good deal as early as the summer before. Keep your eye out for specials. There are so many travel and discount websites now, you just have to go to your favorites and watch for them. If it is feasible, try to find something with a kitchen to save on meal expenses. Or you can try a house swap, or hostel. Don’t forget to check out Airbnb for some offbeat affordable options. If you are very flexible about where and when you go (retirees for instance) here is where you may be able to snag some great last-minute deals if you keep watching!  Transportation: Again, keeping the budget in mind. If money is tight this is not the year to be flying off somewhere. Keep it closer to home. If you have a little more leeway, then maybe this year you can take it further afield. Don’t feel you need to fly away to get away. Remember, some people are flying to wherever you live to “get away.” Again, starting at least 6 months out, keep your eye on the flights. When you see a good deal, book it. Don’t wait to see if there are last-minute specials. The airlines don’t really do that anymore and you may very well end up paying more for a last-minute flight. There are also apps and websites that will alert you to a drop in price, and some airlines will send you a refund for the difference. You can save some money by flying on any day except Friday or Sunday, the two most expensive days to fly. And also by booking at less than optimal times and flights that have layovers. Remember to watch for add-on expenses (checking in luggage, etc.) The best thing to do is learn to pack very light. One carry-on bag and you’re done. I’ve done this on several two week trips with no problem whatsoever. You don’t need a lot! You can wear things over and over with no dire consequences. If you are driving, remember to factor gas prices into your budget, also tolls and parking expenses. If you are renting a vehicle get the smallest (cheapest) vehicle you can make do with (it will also be more fuel efficient). It may be a good idea to just go with mass transit at your destination if you can.   Meals: Here, as I have alluded to earlier, the more you can avoid eating out the better. It’s great to have a place with a kitchen. But even if you don’t, always bring a cooler to keep stocked on meal options. Try to get a room that includes free breakfast. Eat up on that!! This way a light lunch will do. Keep things in your room for that. Sandwich bread, peanut butter (or other “fillings”), fruit, yogurt, cheese, crackers, nuts, etc. Don’t forget to bring your water bottle. Now you can eat in your room or take your lunch out on the road for a picnic wherever you go for the day. Dinner does not have to be a fancy affair every night. A quick deli meal or some tacos will do. Also remember to share meals if you go somewhere with big servings (or bring a “doggie bag” home for the next night’s dinner). And for the adults, try not to go out for “drinks” every night. You can have “cocktail hour” on your balcony sometimes, with a bottle of wine (or cocktail ingredients) brought from home (or purchased locally)  Activities: These can run the gamut, from those pricey theme park vacations or expensive activities to a (free) hike in the woods or making s’mores around the campfire. You should “limit” yourself to what your budget dictates. Why do I put limit in quotations? Because there are so many beautiful experiences you can have for free that I hardly think this is a limiting factor. It fact I might argue here that the best things in life are truly free! Get the local papers and look up free events in the area. Bring along (or rent) bikes, boats, balls, rackets, etc., etc. Bring board games for those rainy days. The things that bring joy to you and your family are the fun and pleasure of spending time together. You cannot buy relaxation or happiness.

If you can’t afford a vacation, you can’t afford a vacation, but you can still enjoy yourself and share good times and laughter with your family and friends. And whatever your vacation budget is you can still have a quality vacation and make memories to last a lifetime for you and your family. It’s all up to you!   I have talked a lot in these blogs about the what’s and how’s of scrimping and saving for a “rainy day” but today I’d like to talk about the why. That glorious goal! In order to keep your spending under control and not keep living for that constant instant gratification it’s important to keep sight of the dream.  What kind of a vision do you have? What would you do if you had money? When you have your ideal future visualized, it’s much easier to give up all those pricey extravagances that you feel you must treat yourself to regularly. Be specific, really immerse yourself in the dream. If you have a life partner have fun dreaming together. It makes for fun dinnertime or cocktail hour conversation. Would you buy a nice house somewhere? On the beach? In the mountains? Go on an adventure? Buy a motor home and tour the country? Travel to other parts of the world? Treat your family (and future grandkids) to some fun vacations? Save photo’s that you would like your life to look like someday.  Just think how nice it will be to be able to look forward to your retirement years rather than start panicking as the time approaches, wondering how you will live when the paychecks stop coming. It will be such a wonderful feeling to look forward to those golden years knowing that you have enough to live on and then some. Think how nice it would be to have enough money put aside so that you never have to work again. If you do work it will be on your own terms at something you enjoy doing.  It really isn’t that hard. The earlier you start, of course, the easier it will be. But even if you didn’t start early you can start right now and you will be amazed at how quickly the money can add up when you are putting it away at a steady automatic rate and investing it for that compounding interest. So, go ahead and dream! Dreams can and do become reality!   You’ve all heard the expression “April flowers bring May Flowers” I’m sure. But what does it mean? Well in its literal sense of course, we need the rains of early spring to give us those beautiful flowers to enjoy in May. But what is the deeper meaning of the phrase beyond that? When we say it we are talking about how we are willing to put up with some less desirable weather in April because we know it is necessary so that we may delight in the lovely blooms that follow. But we can also apply the phrase to other situations in life. Very often it is easier to endure a less than pleasant circumstance because we know it is essential for something better to come. The financial guru Dave Ramsey has a great saying “Live like no one else so you can live (and give) like no one else later on.” In other words, if you have a future financial goal in mind you will be willing to make the sacrifices that it takes right now in order to attain them. You appreciate the showers because you know they will result in a richness of flowers.  Are you a grasshopper or an ant? The grasshopper will ignore the future and just live for today only to be surprised when winter comes and he has nothing put aside to get him through the cold snowy months. Meanwhile, the ant has been working throughout the summer to build up a stash to sustain her throughout those food barren months. Does this mean that the ant has no fun while he is preparing for the future? Absolutely not! There are a great many ways that that little ant can have fun while also taking the time to put those resources away for that rainy day. But the wise little ant always keeps in mind that winter is coming and does what she needs to do to be prepared.  So, yes, enjoy yourself for today. There are any number of ways that you can enjoy life for very little cost or for free. But if you are a wise little ant you will always be stocking up for the future so that (unlike that silly irresponsible grasshopper) when the future comes you will have an abundance to enjoy and your winter will be more like a gorgeous phantasmagorical riot of spring blossoms. Because you, my little friend, prepared for it.   This is the priority based budget. And it is a great tool to use to help you realize just what your priorities are and exactly where you want your money to go (and, maybe even more importantly, not to go). I could look at where your money is going and give you an idea of where you might be able to trim the fat and the things that I would not “waste” my money on, but at the end of the day it is your money to choose to spend as you will. Of course if you are looking to save money you cannot “choose” to keep spending on all the things you have been spending it on. This is where the priority based budget comes in as a tool to help you with that decision making process. The concept is very simple. You start with the most important things that you want your money to go for. And here we are not talking about the things you “want” the most. We are talking about your most basic needs. You also start with the amount of money you bring in for the month. As you list each expenditure you subtract that amount from your monthly income. So you would start with things like housing (rent or mortgage, and property taxes if applicable), food, electricity, water, heat, insurance, and then continue down the list to “lesser” but necessary to your life expenditures. And as you do this you continue to subtract from your monthly income. By the time you get to the bottom, depending on what your income is you should be getting to your “want” items in order of which things you want the most. When you get down to zero on the other side you are done. You can’t (or I guess I should say shouldn’t) spend money that is not coming in, because this is, of course, what leads to debt. Everyone has different priorities and what would be a frivolous expenditure in my eyes may be a very important source of joy and happiness for you. But the bottom line (zero) is the bottom line no matter what your circumstances are. You cannot go beyond that and this is what forces you to examine what your spending priorities are.  If your money is very tight, you may not even get past the “needs” at the top of the budget. There is no room for “wants” at all. If this is the case you will need to examine how you can increase your income. You can temporarily take on a second job, but you will also need to come up with a more permanent solution to your income dilemma. Can you ask for a raise? Look for a better job in your field? Should you try a different line of work? Get additional education? You need to come up with a plan of action, and start taking the necessary steps to get there. If you have debt, then paying that off should go right after your basic needs are met. If you do not have debt, then you are in a position to start saving and that savings should be at the top of your line items. Retirement savings being at the top, followed by other savings goals. i.e. a wedding, a house, kids (or your own) education, a car, vacation, home improvements, etc. This is the concept of “Pay yourself first” and it works! This way you have all your life goals covered by the time you get down to the bottom of the budget to those everyday “wants”. I have included some budget worksheets that you can use to create your own Priority Based Budget. One has categories to give you some guidelines (but feel free to change them according to your own priorities). And some samples to help you see how it's done: Sample 1. Sample 2. The other is left blank for you to fill in as you see fit. And more samples: Sample 3. Sample 4 The lefthand column of both of them is for you to start with your monthly income and then subtract as you make your way down your list of spending priorities until you get to zero at the bottom... money gone... budget done! You must of course (if you are sensible and want to get ahead with your money) include your saving goals as part of your monthly budget and also things that you will not necessarily spend money on every month, but that you will do so from time to time (like car or home repairs).  Once you finish with this exercise you will have a clear black and white picture of where your money is going according to your own life’s plan. You are on top of your money. You are in control. And that’s a pretty darn good feeling! Congratulations!  |

Archives

June 2022

Categories

All

|

RSS Feed

RSS Feed