Happy New Year! If you, like so many other people, are looking to save money this coming year, I have come up with a list of money saving resolutions that you might want to adopt starting this January.  This list is for you to pick and choose from. They may not all apply to where you are in your financial journey right now, and even if many of them did, I wouldn’t suggest that you try take on too many changes all at once. In fact, if you want to tackle quite a few of them this year, I recommend that you take on a few now and get used to the change, and then maybe adopt a few more changes one at a time as the year goes by, depending on how motivated and ambitious you are feeling. So here they are (in no particular order). I hope you find a few that may be helpful to your own situation.  1. Max out your retirement contributions (401K, Roth IRA).   3. Write down what your short term, medium term, and long term savings goals are, and devise a plan to start saving for them.   5. Go through all your monthly bills (especially those online subscriptions for TV/music/gaming, etc.) and cancel what you really don’t need. Call others to ask for reduced rates.  6. Slash your grocery bills as much as possible. Make it a challenge! See Auntie Victoria's Money saving Grocery Shopping Tips  7. Pay off your debt and stop charging things!  8. Stop buying new clothes. You probably already have more than enough to live on for the year. (live with what you have and/or shop thrift shops or resale sites).  9.Resolve to use free entertainment as much as possible this year.  10. Get a library card and start using it (this will help with #9 as well (free books/movies/events, etc)  11. If you have a mortgage, make a plan to prepay it off as quickly as possible. Start making extra payments towards the principle every month. (this will save you a ton in interest payments!). 12. Start keeping track of all your spending (get a little notebook to track it daily). Add it all up (into categories) at the end of each month.  13. Start thinking of your upcoming expenses ahead of time (i.e start saving for next December’s holiday season now).  14. Along the lines of the above: Start a “car account” to always be saving up for your next car (automatically, of course), see tip #2). See No Loan Auto Ownership  15.Stop buying drinks. Make coffee at home, drink tap water (get reusable travel containers). Just stop drinking other (sugary) drinks. See One Thing to Stop Wasting Money On  16. Do a no-spend month challenge.  17. Cut the cable. There are plenty of ways these days to watch TV at little or no cost.  18. Break a (costly) habit. Even a small spending habit that you give up can add up over time (a $1.50 candy bar bought each day would add up to $45.00/month… or $547.50/year!  19. Cook and eat more of your meals at home (can you do a “no restaurant” year?) Or at least a month?  20. If you have kids, start saving for their education now. Don’t be overwhelmed. I don’t mean for you do this all at once. Just pick one, (or a few) and go for it! Any step in the right direction is a good one to get you started on your journey to financial success!  Wishing you all a very happy, healthy prosperous New Year and, of course a very bright future!

0 Comments

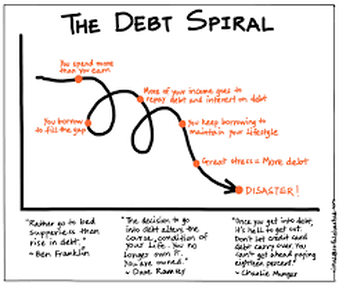

There is a law of physics that you’ve all heard of that states that an object in motion tends to stay in motion. Well, I’ve observed that it is the same with most people’s finances. Once people get going in a certain direction with their money, they tend to remain on it until something happens to change it.   This motion can be in either direction. Once people begin to live beyond their means and start to accumulate debt, that downward spiral into debt begins to snowball, making it very difficult to get off the ride. But the good news is that, conversely, if people can start to move the needle in the opposite direction and start to save money instead of accumulating debt, this too can have a snowball effect and the more you save, well, the more you save! Being in debt becomes a perpetuating cycle for the very reason that you are in debt. When all your money is going towards your credit card and other debt payments, there is never any money to use whenever something comes up. And this too goes on the card. You can see (or maybe know firsthand) how this could go on and on. On the other hand, if you have money saved, you not only easily pay for any financial emergency or need that comes your way, and avoid paying interest payments, but you can also take advantage of strategies that can grow your money even further.  The most obvious of these opportunities would be the ability to invest your money. Now instead of paying out interest you have the ability to turn it around and have that interest work for you. And thus the snowball grows (in a good direction!)  When you have a cushion of money beneath you, you no longer have to approach life from a position of desperation. Desperate people need to resort to desperate measures to keep themselves afloat. Think of those insidious payday loans, with their ungodly interest rates.  Desperate people do not have the money to maintain their possessions (I.e., cars, appliances, roof, etc.) or even their health, and often end up paying much more in the long run for car repairs, home repairs, or even worse, a health crisis because they were unable to keep up with the maintenance required.  Of course, the key is to turn this trajectory around to be moving in a positive direction. The hard part is the turning. It does take a lot of work and sacrifice to get a debt situation under control. But once you push through and make it to the other side the rewards are immense. Now you can relax and let that money work for you. The very interest you were fighting now becomes your friend. It’s a great feeling.  I hope I can inspire you to begin to move your needle in the right direction. I will be here cheering you on the whole way! If you need any specific strategies to help get you going, take a look through some of my other blogs for some tips and tricks that might work for you. If you need more personal help, feel free to contact me for a one-on-one appointment.  Wishing you all the best in snowballing your way to a better and brighter future!

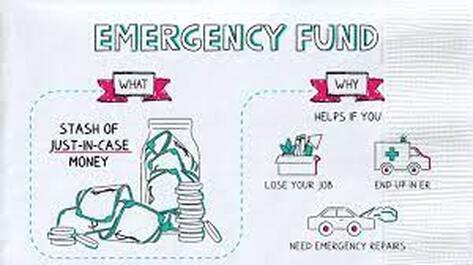

Well, it’s windfall season, and many people are looking forward to a double bonus this year. Not only might you be getting a tax refund, but that third stimulus check may be heading your way at the very same time! The big question is “What do we do with it?” Of course, there are any number of things you can do, and a lot of what you do may ultimately depend on your personality. Are you a spender or a saver?  The great irony here is that the very people who might need to be saving that money (because they have a history of spending) are the ones who may choose to spend it, whereas the natural savers (who are already in good financial stead due to that character trait) are likely to save this money too. So let’s have a run down here on what you should be doing with the money, depending on your individual financial circumstance at the current time. Here is an easy-peasy priority list that you can run down anytime a big fat windfall check comes your way that will give you the best bang for your buck in getting ahead with your finances (which hopefully is your ultimate goal here): 1. Are you current with your bills? If you are not, then this is what you need to use this money for. If this is a struggle for you then it will have to go to your most dire needs, and that’s that. My heart goes out to you during this trying time and I hope as this crisis gets better your situation will improve accordingly.  2. Do you have any debt? Then, by all means, pay it off (or at least down). Start with your smallest debt and pay them off smallest to largest until you have used up all the money. Bonus! Maybe this head start will give you the incentive you need to get serious about continuing on to pay the rest off.  3. Do you have an emergency fund (of three-to-six months-worth of expenses) saved up? If not, put it towards that. Put this in a separate account away from your everyday saving/checking accounts. And again, maybe this will be incentive to keep going and fully fund it! Plenty of people found out this year just how important it is to have one!  4. Do you have any big financial goals you are working to save up for? (a car, education, a wedding, a house, a home repair, or improvement project, a vacation, etc.)? Put it toward that. Open up an online bank account (separate from your everyday account), put the money in there and set up automatic monthly payments going into it to continue funding it until you reach your goal. If this goal is a more long-term savings goal (more than five years away) then you might want to buy a mutual fund to make your deposits into for a greater rate of return on your money. You can do this by opening up a discount brokerage account (such as in Fidelity).  5. Do you have a mortgage? Pay that down (or off!). You do not want to get to retirement age with a mortgage still hanging around your neck. And the faster you can pay it off before retirement the more time you will have to save even more money towards that golden retirement nest-egg! And the less interest you will pay on it in the long run!  6. Retirement. If you are good on all of the above then there is nothing wrong with adding this money to your retirement account, or starting a new one. I know, I didn’t give any “spending” options in this list, but hey, I’m a budget coach. We teach people how to save their money. So, I guess if you are on nice solid financial ground on all fronts and you want to take this money and spend it on something then what can I say? But whatever you do, please put the money to good use. If you really don’t need it at all, maybe you could donate it to those that really do.  This prioritization schedule can be applied to all windfall money that comes into your life at any time for whatever reason. It is very easy to go down the list, see where you are with your finances and know exactly what to do with it.  I hope this helps! As always, wishing you all a very bright financial future!   Sometimes there is just something to be said for boiling it all down into a nutshell and that is just what I have decided to do in this blog. This is pretty much says it all in seven easy-to-follow rules. The best time to start living these rules is from the minute you start that very first job. That is the time to set up good habits that will keep your finances healthy and thriving for your entire life and ultimately lead you on the path to that beautiful dream of financial freedom!  If you know anybody who is just starting out here is the perfect gift for them. Just print these rules out for them and you will have changed the trajectory of their life forever.  1. Always live below your income level (and be saving for retirement and goals). 2. Always be saving at least 15% of your income into your retirement account(s). 3. Always have an emergency fund set up of at least 3–6 months' worth of spending. Your Emergency Fund questions 4. Keep track of all your spending. Know where your money is going! 5. Learn to distinguish wants-vs-needs. Many things that we think of as needs are actually wants. Don’t buy wants if you can’t afford them. 6. Never buy anything on credit (including cars). No Loan Auto Ownership. Save up and pay for things with cash. One exception to this would be a mortgage on a house but put a hefty downpayment down. Get a 15 yr fixed rate mortgage and pay it off ASAP. 7. Pay yourself first! Put your savings on Automatic Pilot. Set up an online bank account (or a few) to save up for your future needs. It’s better if you can have a separate one for each goal (i.e the car account, the wedding account, the vacation account, etc.) Set up automatic payments going into them each month from your checking or savings account. You really can’t go wrong if you live by these simple rules. They're not that hard to do! Wishing you all a very bright future!   I have been talking in this space for years now with tips about how to save money and especially lately, of course, with so many people feeling the financial pinch of this Covid lockdown, saving money has become crucial. But someone posed the very legitimate question of where exactly they should be putting their savings. Some people just keep it in their regular (everyday) checking or savings account. That is not a good idea, and I will l explain why.  You (should) have more than one savings goal for your money, and keeping it in a lump sum actually tricks the mind into thinking you have more money than you do. And for some people this makes it very tempting to spend it. This is the other reason to keep it separate from your everyday money. Once you break it down into the various needs you have for your money you get a more realistic picture of how much you have and how much you still need to save. Here is a breakdown of some goals you might have and where you should be putting the money for them: #1 Retirement: This can be a 401k or other workplace IRA account, or an IRA you have set up for yourself. At least 15–20% of your income should be going into that. Within that 401k or IRA, the money should be invested, of course. Low cost (index fund) mutual funds are fine. If you want to get fancier than that it is entirely up to you.  #2 An emergency fund: This is especially important in these uncertain times we are going through. If you don’t have a fully-funded emergency fund (at least 3–6 months-worth of expenses), money should be going into this each month. In fact, during this time you might want to beef this up even more. When you reach the 3–6-month goal (or more) then just leave that sitting in a separate account for when you need it. This should be a liquid readily accessible account (not invested).  ,#3 A car fund: Most people own a car and should always be saving towards the next one (paying car payments to yourself) so that you never have to finance one. Get off that car payment carousel! This will save you untold amounts of interest payments thrown away to the bank during the course of your lifetime. If you have no need for a car, then obviously this one does not apply to you,  #4 Other savings goals: I recommend you separate them out into separate accounts. This is anything else you are saving for, a wedding, down-payment on a house, home repairs, trip, kids college, etc.  For most of these savings I recommend you open up an online bank account (or more than one) and then set up automatic payments going into them (from your regular checking/saving account), calculating how much you will need for that goal and the amount of time you have to save for it. I suggest this for two reasons. One, the online banks have a slightly higher interest rate than brick and mortar’s do, and two, they are (at least psychologically) less accessible (out of sight/out of mind), so you will be less tempted to dip into them. And labeling them with a certain goal makes them more “off limits” to impulse spending too.  One more thing. If any of these goals is on a long-range timeline (you will not be needing this money for at least five years or longer), then you might consider buying a (low-cost index fund) mutual fund to be putting that money into for better returns. Since the market is volatile by nature, I would not recommend doing this for any shorter range goals as you risk losing (some of) your money. But for longer range goals, it is a pretty safe bet that, with the usual returns on the stock market, you are likely to do better with this money than putting it into a savings account.  So now you have an exact blueprint of where and how to save your money. Just plug in your particular goals and you can have the whole thing set up in one afternoon. And the beauty of this automatic savings is once it’s done you never have to think about it again. All you have to do is tweak it from time to time as your goals change (and/or are met). You can just get on with your life and stop stressing about money. And that’s what this whole money saving business that I’ve been teaching you is all about! 😀 A peaceful stress-free life!  Wishing you a bright, stress-free, peaceful life of savings!   There is panic all around us. What should we be doing to keep ourselves and our loved ones safe? How long will this last? What supplies do we need? Do we have enough toilet paper? Sometimes we can be blindsided by what life throws at us. The best way to be prepared for the unexpected is to, well, be prepared.  In the case of a new disease coming your way, you are in a much better position to deal with it if you have been living a good healthy life up until that point, eating good fresh whole foods, getting proper rest and exercise, maintaining a healthy weight, etc.. If you have been living this way, chances are you have a much better immune system to fight off the infection. But if you have been eating a poor diet, are out of shape and overweight, leading to possible chronic conditions, can you suddenly start living a healthy lifestyle and expect to have the same healthy immunity as the infection invades your community?  Obviously you would have had to been building up that immunity and living a healthy lifestyle for quite some time for it to be effective for you now. I guess you are getting the idea of where this is leading to. The way we live our everyday financial lives also has a big impact on how well we are prepared for whatever life may throw our way.   Perhaps this coronavirus has directly (or even indirectly) affected your income. Are you financially prepared to weather the storm? Times like this bring home just how important it is to live below your means (when you have means) and constantly be putting money away for the lean times (or that big “lean time” in your future, otherwise known as retirement).  If your ordinary life includes having no debt, having a good emergency fund put aside, and saving on a regular basis, then you are much less likely to feel panic and upheaval when you come to a bump in the road. The more “padding” you have the less you will feel those bumps. Things that are a (financial) crisis to the ill prepared are merely blips to those that have the money to deal with them and move on.    If you see the sense in this and would like to shift from a living-on-the-edge (paycheck to paycheck) lifestyle there are many actions that you can begin to take to shift to a saving way of life. If you don’t know where to start I have many blogs on various aspects of money saving strategies that you can implement. Right now, while you are likely sequestered at home, might be the best time to finally sit down and take a good look at your financial situation and take control. Here are just a few that you might find particularly helpful: New Year Savings Resolutions Would You Love to Save More Money? Spring Clean Your Finances Strengthen Your Frugal Muscle, Lighten Your Stress Easy Peasy Savings, Make it Automatic Saving Money Every Day The Perks, Pluses, and Payoffs of Prioritizing My Message to Millennials Ready, Set, Goal! Money Saving Grocery tips from your “Auntie” Victoria And if you scroll through the rest of the blogs, you may find some more that apply to your particular situation and needs. If you need further individual help feel free to contact me at (845) 758-0250, or brightfuture2budgt4.gmail.com for a personal appointment.  Wishing you all the best for staying healthy now and moving toward a healthy financial future.

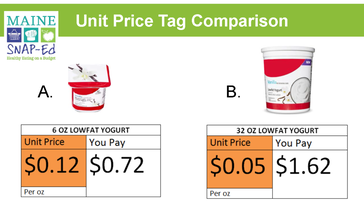

A while back when my niece was moving out on her own, I made this guide for her to help her save on grocery shopping. And now I thought it would be a good idea to share it with the rest of you. So just consider me your "Auntie" Victoria, as I present you with some of my sage tips on getting the most from your food shopping dollar.  #1 – Do not start with a menu list for the week! #2 – Look at the circulars every week, and make your list from the sale items (you have to know your prices, just because it says it’s “on sale” doesn’t mean it’s a good price). Learn your prices. You can keep a book/ list of them if you want to.   #3 – Then plan your meals for the week, based on what you have. #4 – Stock up on items when the sale is super good. #5 – Buy store brand / generic. It is almost always just as good (and, in fact, the same exact product) as the name brand. And you will pay much less.  #6 – Keep a running list of what you are getting low on (to replenish), and keep a well stocked pantry. This eliminates the need to go out shopping for a few needed items between (weekly) shopping trips. # 7 – Which brings us to: Shop only once a week! (In fact, some savvy shoppers shop only once every other week), This saves time, gas, and the temptation to impulse buy! #8 – Plan meals based on inexpensive ingredients! Rice, pasta, eggs, etc. Eat less expensive meat. Chicken, ground beef, stew meat, things like that. Eat meatless as much as possible, See my blog on how eating healthy (vegan) is cheaper. #9 – Don’t buy prepackaged food (i.e. boxed “mixes”, frozen “meals”) Make things from scratch. It's cheaper and healthier too! #10– Don’t buy things in single portion sizes. Portion out your individual size snacks yourself into baggies, little containers, etc. #11 – Use reusable containers as much as possible. Not “throwaways” (such as tin foil and plastic wrap,) Always ask yourself if a reusable container would do for this purpose. (Baggies can be washed out and reused, but even better to use an actual reusable container).  #12 – This goes for cleaning products too. Use rags instead of paper towels (you can wash them, and reuse).  #13 - Don’t buy bottled water! Tap water is fine. In fact most bottled water comes from a tap somewhere! If you are worried about your tap water, you can buy a filter for your tap, or a filtered pitcher for your fridge. Buy reusable water bottles to fill yourself when going out. If you absolutely must buy bottled water (which you don’t), buy the gallon size (of store brand), and fill your water bottles (or glasses) from that. This also saves the environment from all that plastic!  #14 – In fact don’t buy drinks! They are a super expensive, and unnecessary product, and usually just glorified sugar water. Not good for your budget or your health! Stick to water, or non-dairy milk drinks, or maybe orange juice (which you can buy from frozen concentrate, and make yourself). I know they sell “100% juice drinks”, but they are even more expensive, and even though it is “fruit” sugar, it is still just sugar. If you must buy juice (which you don’t), then at least water them down (a lot!) when you drink (serve) them. And don’t even get me started on soda!  #15 – Use the smallest amount of product necessary to get the job done. Experiment to to see what this would be (by using smaller and smaller amounts – or starting with a tiny amount, and working your way up. For instance, shampoo, conditioner, lotion, toothpaste, laundry detergent, dish soap, cleaning products, and also expensive ingredients in recipes (if you can’t eliminate them altogether). Make a game out of it. “Waste not want not!”  Does anybody even know what this expression means anymore? (#16– And now for the subject of coupons. I know you would think being frugal, I would be one of those crazy coupon ladies, but actually I’m not. The problem is they are mostly for expensive, prepackaged, processed junk food. And it is way too expensive (and unhealthy) to buy that crap anyway. If you do come across a coupon for something other than that (usually for health and beauty products), it is still usually cheaper to just buy the store brand. The only time it is usually worthwhile, is if the store is having a sale, and you have a coupon (especially if the store has a double coupon policy). But, of course you have to know your prices (what that item usually sells for, and if store brand is cheaper). #17– You also have to know your prices, when it comes to Bulk Buying. I often find that the prices on those giant bulk packages (i.e. Sam’s Club) are not better than you can get when that item goes on sale in the grocery store. So, if you are going to bulk buy, make sure you check the unit price (you should always be comparing unit prices anyway!) and know what it typically goes on sale for. And make sure you will be using that item up, before, say, 2 years past the expiration date or (if it is perishable) it turns into a science project. It’s not a bargain if you end up throwing half of it away.  #18 – Speaking of Expiration Dates, they are not that magical. The item is not made to self destruct, or go suddenly bad, on that very date on the packaging. And the companies give themselves plenty of leeway on that (better to be safe than sorry on their end) – it also keeps you buying more of their product as the one in your pantry “expires” and you have to replace it. Take them with a grain of salt (so to speak). I have eaten things long past the expiration date, and am still here to tell about it.  #19 – Don’t throw any food away!! Save even the tiniest amounts. You can use them for your lunch the next day, or incorporate them into dinner, or whatever. Learn to be creative with leftovers! #20 – Always start your dinner plans with “What has to be used up first?” (vegetables or meat “on their way out”, leftovers that have been in there a while, etc.). (Things in your pantry past the expiration date!). In other words: Don’t waste food!! You should never be throwing out food that you spent good money on!  #21– You can also take advantage of this concept at the supermarket. They will usually have a ‘bargain rack” of bread, etc., just at it’s expiration date, or fruits veggies that have to be used up in the next day or two, at very reduced prices. Take advantage of this. Buy them and use them right away.  Well I guess 21 tips are good to start with. LOL!! I could go on and on . . . . Not only with food shopping tips, but ways to save money on everything!! If you ever want help on budgeting to raise a family and “get by on less”, you know who to come to! Your “Auntie” Victoria, of course! Happy Saving!  Bonus tip! (Since you read all the way to the end)... If you really want to save money go Vegan! Meats and dairy are the most expensive items in your shopping cart. If you eliminate them from your diet you will save even more. It's cheaper AND healthier to eat this way. I did it! It's easier then you think! And you will feel great too!

Many people tend to view the holidays as a time of abundance and exuberant gift giving. They equate the season with bountiful shopping and lavish piles of gifts. And while I understand the spirit of generosity and kindness that this custom represents and originates from I can’t help but feel that it has lost something through the years as it has been taken to the extreme.  Of course, being the frugalista that I am, I first must note that, for one thing, it “inspires” (forces?) people to spend beyond their means. So many people today are going into debt for the sake of (the societal pressure to create) a lavish holiday. Do you regret the bills in your mailbox come January? Are you able to pay them off? You can read more in my December 2018 blog about how to have a festive holiday without the debt hangover.  But it goes even beyond the new year regrets. How does this excessive holiday feel to you? Most people report feeling frazzled and stressed out and overwhelmed trying to pull it off. So then, what is the point of it all? Is it for the children? Well, I can tell you right now that children’s happiness not only is not dependent on how many gifts they receive, but is, in fact, negatively impacted by over abundance. They are actually more appreciative of a few well thought-out gifts than a mountain of “stuff." And what message are you sending them with all this “generosity?" Does the word “spoiled” have any meaning to you?   So, if you are currently wrung out by all the stress and overindulgence of the past month, and you are dreading facing those bills in the mailbox come January, it may be time to consider another way next year. Just try it. I think you will be pleasantly surprised.    Wishing you all joy, peace, and contentment at the holidays and always   I spoke on these pages last year about how thankfulness affects your budget and spending habits, so I will not reiterate that (though it bears repeating not only every Thanksgiving but also every day of your life. Read more about that here) This year for the Thanksgiving season I would like to explore another food related topic and blow a common misconception right out of the (over-fished) water. It is often said that eating healthy is expensive. This is one of the usual arguments I get from people when I implore them to save money on their groceries.  I have always been all about eating for less, and have also been mindful of eating a healthy nutritious diet. Rarely has there been a dilemma about choosing one over the other for me. But recently I have discovered that not only is it not more expensive to eat healthily, it is in fact, much cheaper to eat a healthier diet. I have always been a pretty healthy person but I do have a family history of diabetes and heart disease so when my blood test #’s started creeping up I knew it was time to take more serious action to avoid those golden years full of drugs, tests and procedures.  I did a lot of reading on the subject of what kind of diet and lifestyle changes can help control this metabolic syndrome that can lead to an impaired existence in later years, and found the research coming time and time again back to one conclusion: The best diet (for just about any health problem you have) is a vegan diet.  Now I am not really a stranger to that way of life. Two of my kids are vegetarian and the one that lives with me is vegan. So I have a head start in knowing how to cook without meat and even to some extent without dairy products and eggs. Never the less, it is somewhat of a learning curve to eat like that on a daily basis. But we are finding more and more that it is quite easy to come up with delicious meals that contain no meat or dairy, and not feel deprived in the least. Yes, I said we, my husband has quite willingly come on this transformative journey with me. We are not completely there yet. We do occasionally “cheat” and use a dairy product in a dish. And we are still using up the meat that is in our freezer, having it in small portions once every 2 weeks or so. But we have come a long way in the process and feel that we will be eating a totally vegan diet for the most part in a short time.     I am not writing about all this to get on any high horse about veganism. Although I have also, in the process of my research, discovered just how healthy it is for the planet (and of course the lives of the animals) as well. But the real surprise that I would like to impart on these pages is the effect on our food budget! Think about it for a moment. The most expensive items you put in your grocery cart are the meats and dairy products. When you eliminate them your bill goes way down!  The trick is (and I think this is where the “expensive to eat healthy” myth comes from) is not to replace that meat and dairy with specialty “health foods” and vegan “meat” substitutes. We just buy (and eat) basic inexpensive ingredients like rice, beans, legumes, quinoa and other grains, pasta, potatoes (white and sweet), oatmeal, vegetables and fruits. And our (already low by most people’s standards) food bill has dropped to practically nothing!  Cheap and healthy (and delicious, I might add), it’s a win, win, (win) all around! How can you beat that! And we will also save on health bills in the long run. Add another win to that last sentence!  So a little food for thought for you to contemplate this Thanksgiving season. Bon Appetite! Wishing you a wonderful holiday and a bright future!   Experiment! Try some vegan recipes here

Read these books about how a vegan diet can change your health : The Starch Solution by Dr John McDougall Food over Medicine by Pamela Popper  I know I am dating myself here, but back when I was a wee lass, Halloween was a simple holiday, simply for kids. And when I say simple I mean that a few weeks before October 31st, we kids, (not our parents) would start thinking about what we wanted to dress up as for Halloween. Then we would scrounge our closets and other parts of the house for things we could use to accomplish our goal. There were usually things like cardboard boxes, tin foil, old clothes of our parents, yarn, fabric scraps and other such items involved. If our parents went all out and bought us a costume, it would be this thing that came in a 12” x 12” box consisting of a flimsy cover-up with a picture on it to represent what we were supposed to be and a cheap mask with a rubber band in the back to hold it on, like this:   These are way more ambitious homemade costumes than we ever came up with. LOL! Very clever! On Halloween day itself we would rush home from school, put our costume on and head out with an old sheet or grocery bag to go around the neighborhood trick or treating. We would be home by dinner to review, organize, and trade our loot and that was it. Halloween over. As for decorations, maybe we would have a few cardboard cutouts of pumpkins, or bats, or ghosts, that we would tape on to our door or windows. And these we saved and used year after year. Oh, and the adults did not celebrate at all. They were not really involved other than to help us with our costume, if we asked, and buy and give out the candy for the trick-or-treaters. Fast forward to today and it (like almost every other holiday, and so many things in our society) has become a multibillion dollar industry that goes on for an entire season.  Now I know I am sounding rather curmudgeonly here and don’t get me wrong I am not against people having fun for Halloween, adults included. I am just saying that if you are in debt, or not saving enough, it would be prudent on your part to reign in the holiday spending. Even my own (frugal) family has gotten into the spirit. When my kids were little we began hosting a spooky bonfire party each year at this time, adults included, which even though my kids are all adults now, we still often continue to this day. As I said we held our annual Halloween event, but I never went crazy with the spending. Since I knew it would be happening I kept it in mind all year long when I was shopping at yard sales and thrift shops. And I would take a look for clearance sales in the stores in the days after Halloween. And, of course, I would save things and use them year after year. I would also pad the decorations with things I had around the house, such as many candles in jars. Even Christmas lights can work for a spooky effect. I would recycle old halloween costumes into creepy scarecrows strategically placed around the yard. My kids would often put together a haunted house or trail, also cleverly using whatever household things they could find. For instance, one year “Dr. Ner’do well’s” lab contained body parts in jars, A cauliflower for the brain, grapes for eyeballs, chicken bones for fingers, etc.    We also invited everyone to come prepared with their favorite scary story to tell as we sat around the fire. Free frights and chills for everyone!  So I think you can see what I’m getting at here. I don’t think we will ever be getting back to that simple sweet Halloween of my childhood years but there are still many ways to get into the spirit and have tons of spooky holiday fun, adults included, without giving up your hard earned money. A little imagination can go a long way towards making your piggy bank happy and still making your Halloween spooktacular!  The author and a friend in our homemade costumes at last years bonfire party.  Happy Frugal Halloween!

|

Archives

June 2022

Categories

All

|

RSS Feed

RSS Feed