I have been talking in this space for years now with tips about how to save money and especially lately, of course, with so many people feeling the financial pinch of this Covid lockdown, saving money has become crucial. But someone posed the very legitimate question of where exactly they should be putting their savings. Some people just keep it in their regular (everyday) checking or savings account. That is not a good idea, and I will l explain why.  You (should) have more than one savings goal for your money, and keeping it in a lump sum actually tricks the mind into thinking you have more money than you do. And for some people this makes it very tempting to spend it. This is the other reason to keep it separate from your everyday money. Once you break it down into the various needs you have for your money you get a more realistic picture of how much you have and how much you still need to save.  Here is a breakdown of some goals you might have and where you should be putting the money for them: #1 Retirement: This can be a 401k or other workplace IRA account, or an IRA you have set up for yourself. At least 15–20% of your income should be going into that. Within that 401k or IRA, the money should be invested, of course. Low cost (index fund) mutual funds are fine. If you want to get fancier than that it is entirely up to you.  #2 An emergency fund: This is especially important in these uncertain times we are going through. If you don’t have a fully-funded emergency fund (at least 3–6 months-worth of expenses), money should be going into this each month. In fact, during this time you might want to beef this up even more. When you reach the 3–6-month goal (or more) then just leave that sitting in a separate account for when you need it. This should be a liquid readily accessible account (not invested).  ,#3 A car fund: Most people own a car and should always be saving towards the next one (paying car payments to yourself) so that you never have to finance one. Get off that car payment carousel! This will save you untold amounts of interest payments thrown away to the bank during the course of your lifetime. If you have no need for a car, then obviously this one does not apply to you,  #4 Other savings goals: I recommend you separate them out into separate accounts. This is anything else you are saving for, a wedding, down-payment on a house, home repairs, trip, kids college, etc.  For most of these savings I recommend you open up an online bank account (or more than one) and then set up automatic payments going into them (from your regular checking/saving account), calculating how much you will need for that goal and the amount of time you have to save for it. I suggest this for two reasons. One, the online banks have a slightly higher interest rate than brick and mortar’s do, and two, they are (at least psychologically) less accessible (out of sight/out of mind), so you will be less tempted to dip into them. And labeling them with a certain goal makes them more “off limits” to impulse spending too.  One more thing. If any of these goals is on a long-range timeline (you will not be needing this money for at least five years or longer), then you might consider buying a (low-cost index fund) mutual fund to be putting that money into for better returns. Since the market is volatile by nature, I would not recommend doing this for any shorter range goals as you risk losing (some of) your money. But for longer range goals, it is a pretty safe bet that, with the usual returns on the stock market, you are likely to do better with this money than putting it into a savings account.  So now you have an exact blueprint of where and how to save your money. Just plug in your particular goals and you can have the whole thing set up in one afternoon. And the beauty of this automatic savings is once it’s done you never have to think about it again. All you have to do is tweak it from time to time as your goals change (and/or are met). You can just get on with your life and stop stressing about money. And that’s what this whole money saving business that I’ve been teaching you is all about! 😀 A peaceful stress-free life!  Wishing you a bright, stress-free, peaceful life of savings!

0 Comments

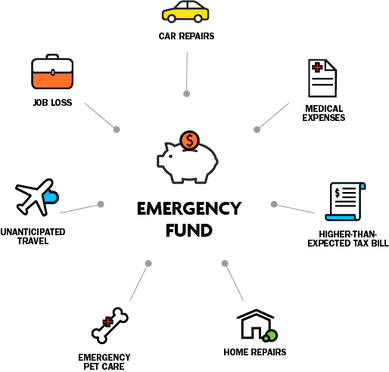

This strange lockdown we have found ourselves in and the resultant loss or decrease in income has left many people to ponder their financial situation and ways they have been managing their money up until this point. As I mentioned in the previous blogs, some people are just now waking up to the need for setting money aside for times such as this. The idea of the emergency fund has resurfaced into people’s consciousness, and the term is being batted around quite a bit of late. So I thought I would dedicate this space to the topic.  First of all, what is an emergency fund, and why do we need one? The general consensus is that we should have about 3-6-months-worth of living expenses put aside, that is there to be used strictly for emergencies only. This money is best kept in an online bank account (slightly better interest rate) and completely separate from your everyday checking/savings accounts. The exact amount in there is up to you. If your income is very variable or otherwise unstable, then the larger amount (6 months) would be advised. Some people prefer to have even more than 6-months-worth if their income is very unstable, or they are very risk averse, or prefer more of a cushion. Everyone, no matter how stable they think their income is, should have at least 3 months at the bare minimum, because no matter how good things are going for you right now, “s#@t” happens!  The purpose of having that fund is to keep your finances from being derailed when the unexpected happens. If you have that cushion put aside you can just dip in, pay that medical bill, or home repair or live on it through a job loss and get right back on track where you left off without throwing your whole finances into a tizzy. And even more importantly you won’t be forced to reach into your wallet for the credit card and put yourself into debt over the situation.  Someone posed the question to me recently: “How do I determine when to take money out of my emergency fund?.” An excellent question, and that is why I chose to address it in this month’s blog. The bottom line is this, the more you budget for the unexpected, the less you will ever have to dip into your emergency fund. It’s as simple as that. So how do you determine when you really do need to break that piggy bank?  Before dipping into the emergency fund you should ask yourself: “Do I really need to use this money right now?” Do you have some time to save up the money that you need, and get by without it for a while. Can you get by without whatever the expenditure is altogether? “Is this something I really need to buy?” Can you borrow something (at least while you save up)? Can you make do without it in some other way? “Is buying this thing right now really necessary?” Maybe it’s not the “need” you think it is, but more of a “want”. “Is this purchase right now really worth the sacrifice it will take to replenish my emergency account?” “If I don’t spend the money right now on this emergency will this situation cost me more money in the long run?” (i.e. a car or house repair that will get worse if left unfixed). In that case, by all means, do it.  And after you have dipped into your emergency fund consider if this expense is something you should be adding to your monthly budget so that you are prepared for this type of emergency in the future (I.e. beefing up your “car repair” or “home repair” fund, or adding a new category to cover whatever the expense was).  Ideally, if you have budgeted for every possible “unexpected” expense that may come your way, your emergency fund becomes just a big fat luxurious cushion for you to sit on and enjoy the security of. Wouldn’t that be a nice feeling!  Wishing you a bright secure future!

|

Archives

June 2022

Categories

All

|

RSS Feed

RSS Feed