I have been talking in this space for years now with tips about how to save money and especially lately, of course, with so many people feeling the financial pinch of this Covid lockdown, saving money has become crucial. But someone posed the very legitimate question of where exactly they should be putting their savings. Some people just keep it in their regular (everyday) checking or savings account. That is not a good idea, and I will l explain why.  You (should) have more than one savings goal for your money, and keeping it in a lump sum actually tricks the mind into thinking you have more money than you do. And for some people this makes it very tempting to spend it. This is the other reason to keep it separate from your everyday money. Once you break it down into the various needs you have for your money you get a more realistic picture of how much you have and how much you still need to save.  Here is a breakdown of some goals you might have and where you should be putting the money for them: #1 Retirement: This can be a 401k or other workplace IRA account, or an IRA you have set up for yourself. At least 15–20% of your income should be going into that. Within that 401k or IRA, the money should be invested, of course. Low cost (index fund) mutual funds are fine. If you want to get fancier than that it is entirely up to you.  #2 An emergency fund: This is especially important in these uncertain times we are going through. If you don’t have a fully-funded emergency fund (at least 3–6 months-worth of expenses), money should be going into this each month. In fact, during this time you might want to beef this up even more. When you reach the 3–6-month goal (or more) then just leave that sitting in a separate account for when you need it. This should be a liquid readily accessible account (not invested).  ,#3 A car fund: Most people own a car and should always be saving towards the next one (paying car payments to yourself) so that you never have to finance one. Get off that car payment carousel! This will save you untold amounts of interest payments thrown away to the bank during the course of your lifetime. If you have no need for a car, then obviously this one does not apply to you,  #4 Other savings goals: I recommend you separate them out into separate accounts. This is anything else you are saving for, a wedding, down-payment on a house, home repairs, trip, kids college, etc.  For most of these savings I recommend you open up an online bank account (or more than one) and then set up automatic payments going into them (from your regular checking/saving account), calculating how much you will need for that goal and the amount of time you have to save for it. I suggest this for two reasons. One, the online banks have a slightly higher interest rate than brick and mortar’s do, and two, they are (at least psychologically) less accessible (out of sight/out of mind), so you will be less tempted to dip into them. And labeling them with a certain goal makes them more “off limits” to impulse spending too.  One more thing. If any of these goals is on a long-range timeline (you will not be needing this money for at least five years or longer), then you might consider buying a (low-cost index fund) mutual fund to be putting that money into for better returns. Since the market is volatile by nature, I would not recommend doing this for any shorter range goals as you risk losing (some of) your money. But for longer range goals, it is a pretty safe bet that, with the usual returns on the stock market, you are likely to do better with this money than putting it into a savings account.  So now you have an exact blueprint of where and how to save your money. Just plug in your particular goals and you can have the whole thing set up in one afternoon. And the beauty of this automatic savings is once it’s done you never have to think about it again. All you have to do is tweak it from time to time as your goals change (and/or are met). You can just get on with your life and stop stressing about money. And that’s what this whole money saving business that I’ve been teaching you is all about! 😀 A peaceful stress-free life!  Wishing you a bright, stress-free, peaceful life of savings!

0 Comments

This strange lockdown we have found ourselves in and the resultant loss or decrease in income has left many people to ponder their financial situation and ways they have been managing their money up until this point. As I mentioned in the previous blogs, some people are just now waking up to the need for setting money aside for times such as this. The idea of the emergency fund has resurfaced into people’s consciousness, and the term is being batted around quite a bit of late. So I thought I would dedicate this space to the topic.  First of all, what is an emergency fund, and why do we need one? The general consensus is that we should have about 3-6-months-worth of living expenses put aside, that is there to be used strictly for emergencies only. This money is best kept in an online bank account (slightly better interest rate) and completely separate from your everyday checking/savings accounts. The exact amount in there is up to you. If your income is very variable or otherwise unstable, then the larger amount (6 months) would be advised. Some people prefer to have even more than 6-months-worth if their income is very unstable, or they are very risk averse, or prefer more of a cushion. Everyone, no matter how stable they think their income is, should have at least 3 months at the bare minimum, because no matter how good things are going for you right now, “s#@t” happens!  The purpose of having that fund is to keep your finances from being derailed when the unexpected happens. If you have that cushion put aside you can just dip in, pay that medical bill, or home repair or live on it through a job loss and get right back on track where you left off without throwing your whole finances into a tizzy. And even more importantly you won’t be forced to reach into your wallet for the credit card and put yourself into debt over the situation.  Someone posed the question to me recently: “How do I determine when to take money out of my emergency fund?.” An excellent question, and that is why I chose to address it in this month’s blog. The bottom line is this, the more you budget for the unexpected, the less you will ever have to dip into your emergency fund. It’s as simple as that. So how do you determine when you really do need to break that piggy bank?  Before dipping into the emergency fund you should ask yourself: “Do I really need to use this money right now?” Do you have some time to save up the money that you need, and get by without it for a while. Can you get by without whatever the expenditure is altogether? “Is this something I really need to buy?” Can you borrow something (at least while you save up)? Can you make do without it in some other way? “Is buying this thing right now really necessary?” Maybe it’s not the “need” you think it is, but more of a “want”. “Is this purchase right now really worth the sacrifice it will take to replenish my emergency account?” “If I don’t spend the money right now on this emergency will this situation cost me more money in the long run?” (i.e. a car or house repair that will get worse if left unfixed). In that case, by all means, do it.  And after you have dipped into your emergency fund consider if this expense is something you should be adding to your monthly budget so that you are prepared for this type of emergency in the future (I.e. beefing up your “car repair” or “home repair” fund, or adding a new category to cover whatever the expense was).  Ideally, if you have budgeted for every possible “unexpected” expense that may come your way, your emergency fund becomes just a big fat luxurious cushion for you to sit on and enjoy the security of. Wouldn’t that be a nice feeling!  Wishing you a bright secure future!

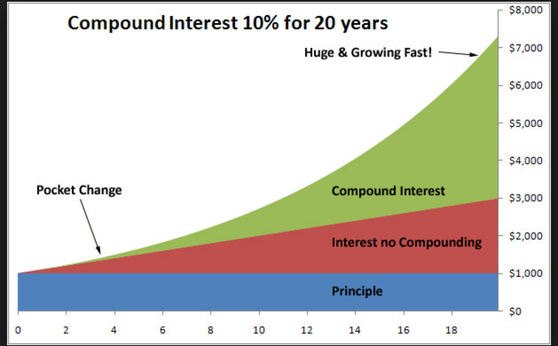

Having spoken with a few millennials lately, including one young lady who was very motivated to get started on the right financial footing, (this is not always the case with the young people I encounter), I thought I’d devote this blog entry to those just starting out on their lives’ journey. This is the stuff that I wish somebody had told me when I was just starting out. I figured it out along the way, but it would have been nice to know it all from the beginning. And some people, unfortunately, just never do figure it out for themselves. Would I have listened? Who knows? But, as they say, if I knew then what I know now, and followed the advice I am about to impart to you, I would very easily be a multi-millionaire by now. And you can be too. Anyone can do it.  Often I find myself very frustrated that young adults, who have the most to gain from learning to be smart with their finances, can be the most resistant to hearing (and following) it. And the sad thing is that if they don’t do it now, although they can still do alright whenever they decide to start, they can never make up for that lost time and the money they could have made by investing early. The magic of all those years of compound interest can never be regained.   So, without further ado, in a nutshell, here are my most salient tips for millennials: #1. The golden rule of finance: Always, Always, Always Live Below Your Means! Start out that way and get used to it. As your income increases you can increase your lifestyle, but always stay below what you are making. 15% of your income should going into your retirement fund at all times.  #2. The other golden rule of finance: Pay Yourself First! You will be paying out a lot of your hard earned money to other people and businesses in your lifetime (your landlord, the mortgage bank, electric company, insurance companies, gas company, food producers, goods manufacturers, health care providers, etc., etc., etc.,…..), but don’t give all your money away to other people or you will have nothing to show for it. Always be keeping something for yourself… up front, before any of your money goes out to anyone else.  #3. Make it Automatic Set up that money to go into your retirement account (401k or Roth IRA) and your other savings (goal) accounts straight out of every paycheck before you even see the money. Out of sight, out of mind.  #4. Keep track of your expenses Set up a system so that you know exactly how much you are spending, every day, every month, every year, and on what. You can do this by hand (simply writing it down) by computer (i.e. your own spread sheet) or with a website (such as mint.com)  #5 Prioritize your budget: Spend your money on what is most important to YOU First comes dire needs, housing, food, transportation, etc. Then prioritize the rest according to your income and needs. Wants come last, and only if you can afford them. Think carefully about wants-vs-needs. Do you really want to sabotage your future goals for some frivolous indulgences today?  #6 Plan for your goals Write them down and save for them systematically (how much do you need to save and when do you want it?). Do you want to get an education? Plan a wedding? Buy a house? Buy a car? Go on a vacation? Always be saving for your future purchases so that you will… (see #7)  #7 Never borrow money! (AKA buy things on credit) Don’t get into the interest paying trap. It is a slippery slope once you start on the debt quagmire. This includes education (student loans), cars (car loans), and those insidious credit cards. Always save up and pay for things in cash. If you don’t have the money, you can’t afford it. The only possible exception to this is buying a house. But even here, if you can manage to save up and pay cash that would be awesome. People do it. I did it for my second house (after I paid the first off by ten years). Certainly aim to put down as large a down-payment as you can and take out a 15-year mortgage. Then (pre)pay that down as quickly as possible. And don’t buy a more expensive house than you can afford. Though the lending banks will pre-approve you for a much bigger mortgage than you can comfortably afford, don't fall for it.  It’s really as easy as following these 7 very simple rules and you will be set for life. It’s not rocket science. Anyone can do it, at any income level. Stick with this lifestyle and you will go from millennial to millionaire, a very bright future indeed!  Which one are you? Hopefully in the green!  You can do it!!

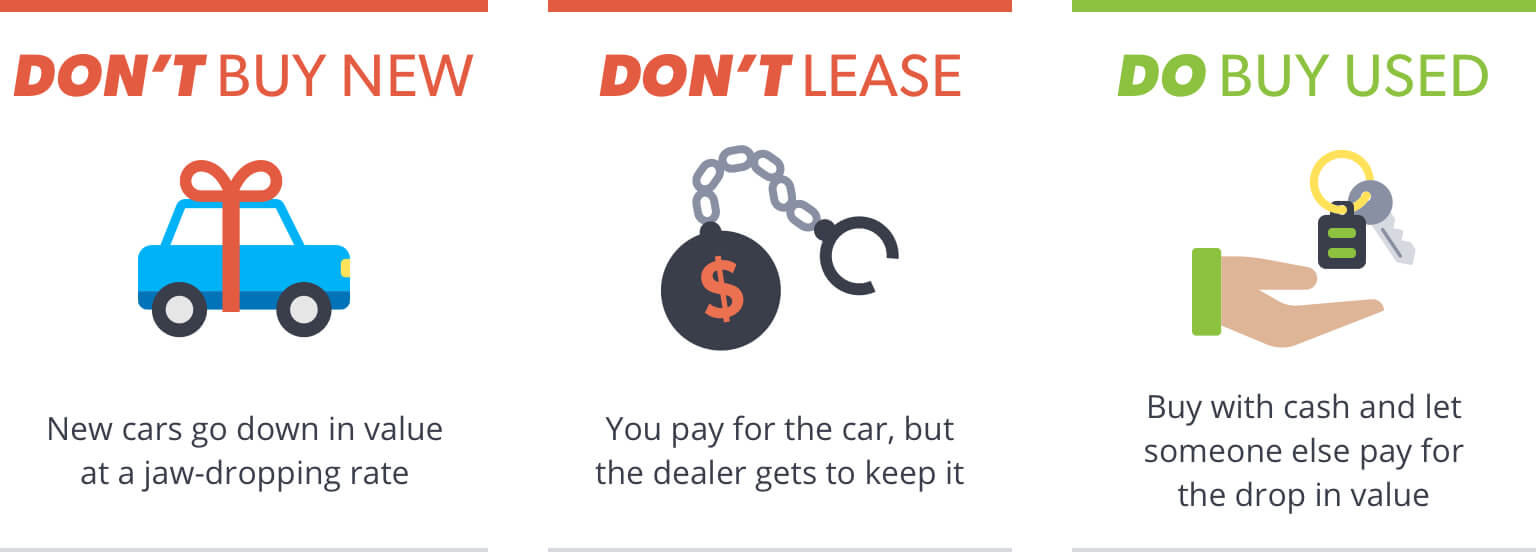

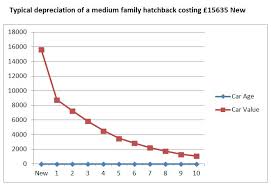

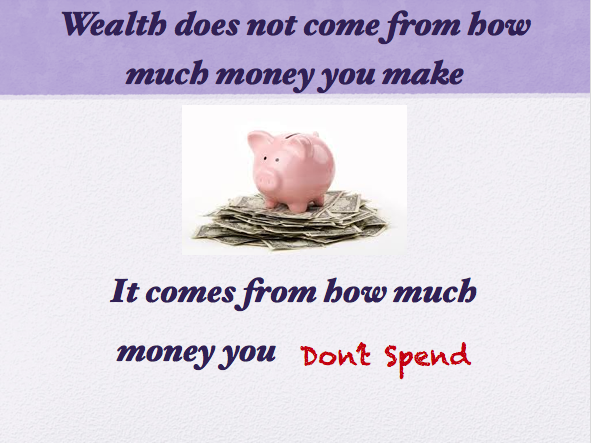

Since I am currently in the market for a “new” car, I thought I would share with you how I do not nor have I ever had a car loan. It’s quite simple if you start from the beginning but wherever you are in your auto ownership journey you can start at this moment and work your way up and out of car loans for good.  What’s wrong with car loans you say… isn’t financing a car the “American way"? Who doesn’t have a car loan? Well I don’t, for one, and I would wager a guess that every “Millionaire Next Door” doesn’t either. And yes, you’re right it has become the “American way” but which Americans are benefiting from that? Hint: It’s not you, the proud recipient of the car loan. It is the almighty bank (or sometimes the car dealerships) that are winning in this drive-now, pay-later arrangement. And the amazing thing is that they have you hoodwinked into believing that they are doing you a favor by getting you into the best car they can for low money down and easy monthly payments. Wow! What a nice guy… NOT! Believe me, car dealers are not in the business of doing you a favor. The only thing they are interested in is their own bottom line. The biggest best car they can sell you lines their own pockets, and getting you to take a loan from them (instead of the bank) is just more icing on the cake. And if you have ever been car shopping lately you will notice that they (subtly or maybe not so subtly) will start touting the glories of leasing a car. This is like taking a car loan on steroids (for them). Think about it. You pay a down payment (maybe $1,000) and then “easy” monthly payments of $299/month, and at the end of the three-year lease you are out $11,764 and you own absolutely nothing! You can now either give the car back and start all over again or pay some exorbitant fee (on top of the almost $12,000 you’ve already paid) to now own the car. You could have bought a (used) car for $11,764 three years ago and still had plenty of life left to it for years to come. And if you financed your car, let’s look at one example of how much you are actually paying for that car by the end of the loan period: If you take out a loan for $25,000 at 4.5% for a 60-month term, your monthly payments will be $570 and at the end of the term you would have paid out $27,364. A total of $2,364 lining the pockets of whoever held your loan. Nice! … For them. How do you feel about giving them all that “free” money? Would you like an extra two thousand in your bank account? But, you tell me, “I don’t have the money to just purchase a car outright.” Well, I can tell you that on a modest income I have never taken out a car loan to buy a car. How did I do it? Well, I bought my very first car for cash and from that point forward I was saving the money (that most people are paying out for car loans) to purchase my next car for cash. Most of the cars were used, at least a few years old, but I did make the mistake of purchasing two of them brand new (all for cash). No loans. If you can afford car payments you can afford to save up for a car!  Now I have instructed my kids to follow my principles. They each saved up for their first car (with a little help from me at times) and bought them (used) for cash. Then I told them to pretend (like many of their peers) that they have car payments, but pay them to themselves. And now through the magic of online bank accounts it was easy for them to set up a “car account” with $200 or $300 a month being automatically deposited into it from their checking account. And with that very modest “car payment,” if they take good care of the cars they have, in 10 years-time they will have between $24,000 and $36,000 towards the (cash) purchase of their next car. And even more than that, really, because instead of paying interest to a car loan, they are making interest on their bank account. It may be only 2% at the moment, but it sure beats paying out at 4% or more! But if you haven’t done that from the beginning and you are currently saddled with a car loan, then the best thing you can do is keep the car after your loan is up for as long as you can, and here’s the important thing: Keep paying those monthly car payments but pay them to yourself so that when you are ready for your next car you will have a chunk of change sitting there for your purchase.  And why do I say I made the “mistake” of buying a few of my cars brand new? Because the depreciation curve is enormous in the first year or two of car ownership and the bulk of that depreciation takes place in the first 5 minutes of car ownership. The minute you drive that sparkly new car off the lot you have dropped a couple of thou off its resale value. Ouch!! Let someone else take that depreciation (thanks first car owner!). Save yourself a couple of thousand dollars and buy a car that’s at least a year or two old.  So, now I will head out to the dealerships. You can buy a car from an individual for less money, but I like the assurance of having the dealer in case something goes wonky with the car a short time after I buy it. And even though I am paying cash I will still keep in mind that (friendly as they are) the dealer is not my friend. I will do my homework and check out any cars I am considering online, for any issues and the prevailing price for that year’s model. You can try Kelly Blue Book or Edmunds for this info. Then I am prepared to bargain (with the mysterious “manager” in the back, that my dealer will be consulting). I may walk away from the deal two or three times before I am satisfied that I am getting a rock bottom price. Of course the dealer has to make some money on the deal. I don’t begrudge him that. I just want to feel that I got a fair deal. Wish me luck as I head out in search of my next set of wheels and I hope you too will someday enjoy the joys of owning your own set of wheels without those pesky loans dragging you down.   Here’s the biggest mistake almost all people make when it comes to savings: They pay their bills, buy their food, make repairs, buy things for the house, pay for kid’s activities, go shopping for clothes, go to the movies, go out to eat, go shopping for some new clothes, etc., etc., and then save what’s left over at the end of the month. Can you see the problem with this? Is there ever anything left at the end of the month?? Many people will also say that they live paycheck to paycheck, but here is the interesting thing about this; They are saying this no matter what the size of their paycheck. The person who makes $300/wk. is saying it and so is the person who makes $600/wk. and the one who makes $3,000/wk. and on up. Right up to that athlete or rock star who is making several million dollars a year and blowing it all, only to go bankrupt when the income dries up. It seems to be just human nature to live just up to your income level whatever that may be, or even a little above that (accounting for all the debt people tend to find themselves in). But if you want to save money the only way you can do it is by living below your means, whatever they may be. Another way to put this is: You don’t save money by how much you make, but by how much you don’t spend. The great investment “guru” Warren Buffet puts it this way:  This is great advice, but how do you do it? Well the great US of A knows how. You pay taxes every year, right? Does Uncle Sam just let you have your full pay and then ask you to cough up the taxes on April 15th? You bet your sweet bippy he doesn’t, because he knows what would happen. People adjust their lifestyle to however much money is coming in. So he just takes his cut up front and people adjust to living on what’s left. Well you can do the same thing for yourself. Just take it off the top. The U.S. government even gave people a means to do just that by starting the 401K program, giving you a tax advantage and a way for you to save money by skimming it right off your paycheck without even ever seeing the money. If you have this offered at your place of employment you should certainly be taking advantage of it. Some generous companies will even match your contribution dollar for dollar up to a certain amount. Free money! Never pass up this opportunity! But even if you don’t have the opportunity for a 401K (or 403B, TSP, etc.), you can still make the magic of automatic savings work for you. All you have to do is set it up once for yourself and done. Savings skimmed right off the top. Out of sight, out of mind. You will quickly adjust to living on what remains. How you set this up depends on what you are saving for. Your first savings goal should be your retirement. I know this sounds kind of backward or counterintuitive, but because you need such a large amount, and because it makes such a difference when you start compounding that interest early, it is imperative that you start this ASAP! If you don’t have a 401K then you can set up your own retirement account in a Roth IRA. I recommend you do this by opening up a discount brokerage account at a firm such as Fidelity or Vanguard. This gives you many options on what to invest your money in inside of your Roth IRA and gives you complete control over it. Once you have your Roth set up it is quite simple to set up automatic payments of whatever amount you choose monthly going from your checking account into your IRA. Whether you have a 401K in the workplace or your own Roth IRA, you can also set up similar automatic payments going into (online) savings accounts for your other savings goals (wedding, car, house down payment, education, etc.) Once you have your savings goals set up automatically in this way, you no longer have to stress about money. You are all set for your future needs both short and long-term, and you can spend what’s left freely. Won’t that be a nice feeling!  |

Archives

June 2022

Categories

All

|

RSS Feed

RSS Feed