January is, of course, traditionally the time when we make resolutions, and unfortunately the time we also traditionally break them. Why is that? Well …change is hard. We are ultimately creatures of habit and a resolution by its very nature requires change. And we would much prefer going along in our daily lives doing the same things in the same ways as we have always done them. So, regrettably our resolutions go by the wayside … and life goes on… and we feel bad.  Instead of setting resolutions this year, how about setting some goals for yourself? “What’s the difference?” I can hear you asking. While a resolution tends to be somewhat vague (“I want to lose weight”), if you are setting them the proper way, a goal is more specific. And to help you make them specific the genius gurus that be, have come up with this cute little moniker: S.M.A.R.T.  So, taking the example of losing weight, we would say that I want to lose 20 pounds (specific) by April (time bound) and I will do this by losing 2 pounds per week (measurable). This goal would be both attainable and realistic. Saying you wanted to lose 100 pounds by April would be very unrealistic. And setting the mini goal (of two pounds per week) makes it easier to work towards. You can now just concentrate on those two pounds per week, rather than the bigger (more daunting) 20 pounds by April. You can even set up a reward system for yourself every week if you make your 2 pound goal (get a message, your nails done, watch your favorite movie, whatever…)  Now, let’s translate this into a money goal. Rather than a vague “I want to save more money this year”, try “I want to save $2,000 by the end of the year”. Now you can break this down into how much you would need to save each month ($167), and per week ($38), and even per day ($5.48). Once broken down this way, it is easily manageable. What can you give up that is currently costing you $5.48 per day, or $38 per week? And much easier to monitor your progress. You can easily see if you are on track. It is helpful to make a chart for yourself.  To be even more specific make a plan for where you are going to put this saved money (perhaps open up a separate savings account for it). And it should be earmarked for a specific purpose (a vacation, new furniture, a new computer…). Or it can be an account that you will continue to add $2,000 (or more) into each year going forward (toward your emergency fund, or a house, or a car…). Now you are not just making vague resolutions, you are setting goals the SMART way. It is a specific amount (broken down into even more specific “mini” goals), it is realistic and attainable, and certainly measurable. And you can continue to manage your progress throughout the year (and give yourself little mini rewards if you need them).  When you set your goals in this very definitive way, you are now shooting towards something very precise, and keeping that goal in mind it is now easier to “give up” whatever you need to do in order to achieve your goal. You are not just making your own coffee in the morning to “save money”, you are saving up for that computer, or furniture, or car or house. It gives you more of an incentive to make the sacrifice. (In the weight loss scenario given earlier, it makes it easier to give up that one of two things that are contributing to your weight gain and swap them out for healthier options, just to make that 2 pounds weight loss for the week).   So try setting yourself some S.M.A.R.T goals this year instead of those nebulous resolutions and see if you don’t stick to them this time around.  Best of luck to you for a bright and prosperous New Year!

0 Comments

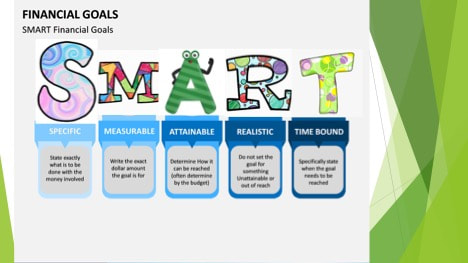

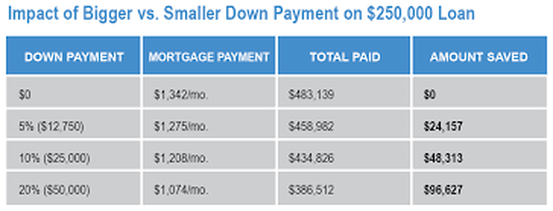

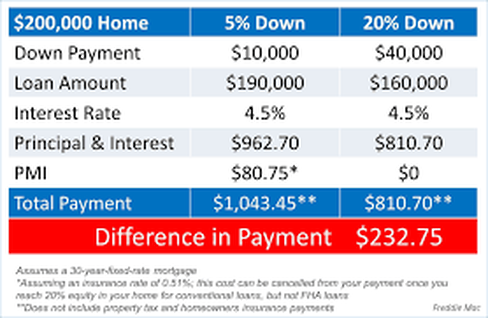

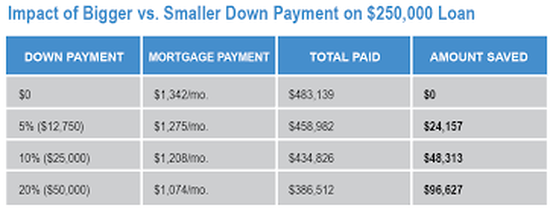

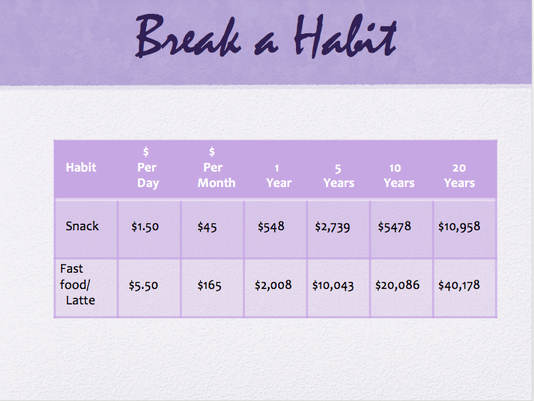

Well, it’s been quite a year to say the least. And I think that how much it affected us and how we came through it had a lot to do with how we had been going about our lives before this year. How prepared were you for something like this?  I think this year many people have come face to face with this age-old question: Are you a grasshopper or an ant? The grasshopper will ignore the future and just live for today only to be surprised when winter comes and he has nothing put aside to get him through the cold snowy months. Meanwhile, the ant has been working throughout the summer to build up a stash to sustain her throughout those food-barren months.  There was no way to foresee this odd turn of events this year and to anticipate how it might affect your family’s finances. But good financial planning does not require a crystal ball.  Your money management style should not change based on the threat of a world event. That is to say, you should always be “preparing” for an impending disaster. If you have not been budgeting in such a manner, then now is the time to do so. You just never can tell when financial hardship will hit, be it worldwide or personal.  The only way to grow your savings during this pandemic or any other time is to spend less and save more. Now is a very good time to examine where your money is going and make some cuts if you are looking to save more money. There are certainly a few things that you are spending money on that are not really necessary.   You should have a nice comfortable savings account set up for your emergency fund (with at least 3–6 months of your living expenses in it) I recommend an online account for this. Any other savings that you will need within the next 5 years or so, should also be in a regular (online) savings account.  For longer-term savings (to grow your savings) open up a discount brokerage account and buy some mutual funds. An S&P 500 fund is the best way to start. As your money grows you can explore other options to diversify your portfolio.  If you have the option of signing up for a 401k (or other retirement account) at work you should do so right away.  The bottom line is if you want to grow your savings to be prepared for the future, you have to save (and invest) your money. There is no magic bullet. Save and invest.  If you are always doing this, even (especially) through the good times, then you will be able to weather through the not-so-good times such as these, just fine.  Don’t be the silly grasshopper from Aesop’s fable, just living paycheck to paycheck, without a thought for tomorrow. Be the little ant saving up for the future  Wishing you all a bright and prosperous future!   Someone I know recently bought a house and my 24-year-old son was asking me about the details. His number one question being “How do people save up that much for a down payment?” As I answered his questions it got me to thinking that I never addressed this topic in these blogs, so here goes:  How do you know when you are ready to buy a house? Well some people think it’s just a matter of saving up that down payment, but really a lot more preparedness needs to go into it. First of all, how settled are you? Many young people move around quite a lot for job changes or other purposes so even if they are very lucky enough to have that down payment at such a young age, it is not necessarily the best time to be putting down roots into home ownership just yet.   Unless you are sure that you will be staying put for at least the next five years, buying a house is rarely a smart move financially. You will sink a lot of money into the act of buying the house (in closing costs, realtors fees, inspections, lawyer’s fees, etc.)  Then once you buy there is the cost of moving in, and often on top of that people will do some work to the house to make it more to their liking. And there is even the inevitable furnishing and decorating, especially if you are starting from “scratch” with nothing.  And if you have put down a small down payment, you will typically not be gaining much equity in the house for the first few years, at least, as most of these initial payments are going to the interest on the mortgage. It is not until the principle starts to go down a little that the mortgage payments will start to chip away at that principle. And of course it also depends on the housing market. Your house could go up in value, giving you more equity but there is also the possibility that it could go down in value and put you in a situation of being “upside down” on your mortgage. That is actually owing more on it than the house is worth. This is what happened to all those people when the housing bubble burst in 2008.   So with all that said, it will take a while before you will get enough principle back when you sell to offset the costs you put in when buying it. If you sell too soon you will not only not gain any money on the sale you could very well come out in the negative for your years of home ownership. If this is the case you would have actually have been better off to continue renting and saving your money. Next, other than that down payment you have saved up, how is your financial situation? Do you have any debts? If you do, it is very smart to pay them off before embarking on your homeownership journey. Do you have an emergency fund (of three to six month’s expenses) saved aside? I would recommend at least six month’s during this transition into home ownership as you never know what can happen. Is your job secure? You don’t want to take on all this extra monthly expense only to be caught high and dry with a loss of income. This type of scenario sends people scrambling and can result in a disastrous situation.  Even if your job is secure, you have a good down payment saved up and you know you will be staying put, have you crunched the numbers to see of you can afford the cost of homeownership? A common mistake people make is this line of thinking. “I am paying X (say $1,500 per month) on my rent so I might as well be paying that amount on a mortgage and actually owning my own home.” The trouble with that is that you must consider all the other costs of owning. Some things that were covered by your landlord before are now your responsibility. Have you thought about taxes, homeowners insurance, (PMI if you have a small down payment), electricity, heat, TV, internet, water, rubbish removal, etc.?  And in addition to all those fixed expenses, if the house is yours, you are now responsible for the upkeep. And no matter what great shape that house was in when you bought it, something always needs attention. Sometimes it seems barely a month goes by without an unexpected household expense. Even non-household expenses can derail you if you are “living on the edge”, just making all your monthly bills without a penny to spare. This is why it is so important to have that emergency fund set up before you move in.  Now what about that down payment? I just mentioned PMI in the previous paragraph. What is that that? If you put less than a 20% down payment then you have to pay Private Mortgage Insurance. And although you are responsible for these premiums this insurance does nothing to protect you. It is to protect the bank from losing the money they lent you should you default on your payments.    So, this brings us to my son’s question. How much of a down payment should you put down and how do you save up that kind of money? The answer to the first question is as much as possible, at the very least 20% (to avoid that PMI) If it’s home ownership you are after (and not living in a bank-owned house that you are paying dearly for (in interest payments) you should set your sights on the biggest chunk of money you can plop down.  Another way to keep your down payment at a higher percentage of the cost of the house is to buy a less expensive house. This way that same down payment you have saved is now a larger percent of the total cost. You can always move into bigger house (or expand the one you are in) down the line should the need arise and your finances improve. Here’s a dirty little secret the banks don’t want you to know. They will approve you of a mortgage that is really out of a comfortable price range for you. Why? Because they are really not interested in how comfortable you are making the payments. They are just looking to get the biggest mortgage for themselves (the more you borrow, the more interest payments they will get). So buy a house that you are comfortable with (monthly payment wise), not what the bank approves you for, and ideally this monthly payment should be no more that ¼ of your monthly income. And one more thing on the subject of mortgages. The bank will automatically default to a 30-year-mortgage, but you are much better off to get a 15-year. The quicker you can get that house paid off, the less total interest you will pay on it. You can save yourself many thousands of dollars (even hundreds of thousands) by just doing this one thing.  Now to Jesse’s question of how to save up for that mortgage. The same way I recommend you save up for anything else. Make it automatic! Open up an online account and set up automatic monthly payments going into it. Take the total amount you want to save and divide it by the months until you want to have the money. If you want to save up a $75,000 down payment in four years that would mean you need to save about $1,500 per month. *See Easy Peasy Make it Automatic  If your timeline for savings is actually more than five years then you might want to consider investing (all or part of) the money into a low cost (relatively safe) mutual fund (such as an S&P 500). Putting those payments away each month will also help you to be living below your income and able to make all those extra expenses when you do move into that house. Owning your own home is the American Dream. It is a great feeling to live in a house of your very own and can also be a real plus to your total financial picture if you are indeed prepared for it, but please make sure you are fully ready before taking the plunge or it has the potential for turning into a nightmare. Do it right and make it your dream come true!  Best of luck to you if you are looking to embark on this exciting new chapter of your story. Wishing you a bright future in your own home sweet home!   It’s resolution time again! Want to lose weight? Get healthier? Will this be the year you buy that new car? Declutter the house? Ditch the spouse? So many possibilities! We always start each fresh new year with such high hopes and expectations. And often high on the list is finally getting those finances in order, paying off debt if you have it, and getting started on that savings plan. Then the year rolls along, and what goes wrong? Well, generally the optimum word here is plan. Do you have one? This quote says It all:  So whatever your financial goals are, you need to actually devise a strategy to achieve them. And you need to be as specific as possible. You first need to take stock of where you are. You can read about how to do that in my very first blog "New Year Savings Resolutions"  When you are writing your goals (and yes, you should be writing them down) you should be as specific as possible. No vague “wishes” here, but very concrete plans for what you are saving for, how much you need to save and when you want it saved by. With this down in black and white you can now devise a plan of action to achieve your goal(s). Here is an acronym that you can use to help you with this: ."Specific: Exactly what are you saving for? (or what debt do you want to pay off? Measurable: Put a very specific dollar amount on your goal (i.e. I want to save $10,000 for a car by next fall). Achievable: Do not state goals that you cannot possibly reach. You will only frustrate yourself. But by the same token, you don’t want to make them so easy that you’re not really accomplishing anything (and still frittering most of your money away). Relevant: Is this an appropriate goal for you at this time, that you want to achieve? (Not saving for a house or a big wedding because everyone else is telling you it’s time.) (Not saving for a big boat when you have credit card or school loan debt to pay off.) Timely: Give your goal a deadline. "I want to save up a down payment for a house ($50,000) by spring of 2022." This way you can break it down as to how much you will need to save monthly to achieve this goal.  Once you have a firm grasp of your goals and how much you will need to save each month to attain them, you can do what you need to do to get there. The first thing you should do is make the savings automatic. Set up an online bank account and have the amount you have decided upon deposited into that account each month, right off the top. Out of sight, out of mind. It’s amazing how you can learn to live on a reduced amount when you never see the money in the first place.  If you need to pay off debts before you move on to savings, pay the minimums on all debts except one and throw as much as you can into the debt you are paying off. Once that one is paid off, move onto the next one. It will get easier and easier as you pay them off as you will have less minimums to pay as you knock off each one.  The other bonus of having these very specific, measurable, and methodical goals is that it makes it easier to sacrifice where you need to as you see your money going towards a higher priority. It feels good to forgo a few immediate pleasures for the sake of your future goals when you can watch your steady progress towards your own financial bright future!   I have talked a lot in these blogs about the what’s and how’s of scrimping and saving for a “rainy day” but today I’d like to talk about the why. That glorious goal! In order to keep your spending under control and not keep living for that constant instant gratification it’s important to keep sight of the dream.  What kind of a vision do you have? What would you do if you had money? When you have your ideal future visualized, it’s much easier to give up all those pricey extravagances that you feel you must treat yourself to regularly. Be specific, really immerse yourself in the dream. If you have a life partner have fun dreaming together. It makes for fun dinnertime or cocktail hour conversation. Would you buy a nice house somewhere? On the beach? In the mountains? Go on an adventure? Buy a motor home and tour the country? Travel to other parts of the world? Treat your family (and future grandkids) to some fun vacations? Save photo’s that you would like your life to look like someday.  Just think how nice it will be to be able to look forward to your retirement years rather than start panicking as the time approaches, wondering how you will live when the paychecks stop coming. It will be such a wonderful feeling to look forward to those golden years knowing that you have enough to live on and then some. Think how nice it would be to have enough money put aside so that you never have to work again. If you do work it will be on your own terms at something you enjoy doing.  It really isn’t that hard. The earlier you start, of course, the easier it will be. But even if you didn’t start early you can start right now and you will be amazed at how quickly the money can add up when you are putting it away at a steady automatic rate and investing it for that compounding interest. So, go ahead and dream! Dreams can and do become reality!   You’ve all heard the expression “April flowers bring May Flowers” I’m sure. But what does it mean? Well in its literal sense of course, we need the rains of early spring to give us those beautiful flowers to enjoy in May. But what is the deeper meaning of the phrase beyond that? When we say it we are talking about how we are willing to put up with some less desirable weather in April because we know it is necessary so that we may delight in the lovely blooms that follow. But we can also apply the phrase to other situations in life. Very often it is easier to endure a less than pleasant circumstance because we know it is essential for something better to come. The financial guru Dave Ramsey has a great saying “Live like no one else so you can live (and give) like no one else later on.” In other words, if you have a future financial goal in mind you will be willing to make the sacrifices that it takes right now in order to attain them. You appreciate the showers because you know they will result in a richness of flowers.  Are you a grasshopper or an ant? The grasshopper will ignore the future and just live for today only to be surprised when winter comes and he has nothing put aside to get him through the cold snowy months. Meanwhile, the ant has been working throughout the summer to build up a stash to sustain her throughout those food barren months. Does this mean that the ant has no fun while he is preparing for the future? Absolutely not! There are a great many ways that that little ant can have fun while also taking the time to put those resources away for that rainy day. But the wise little ant always keeps in mind that winter is coming and does what she needs to do to be prepared.  So, yes, enjoy yourself for today. There are any number of ways that you can enjoy life for very little cost or for free. But if you are a wise little ant you will always be stocking up for the future so that (unlike that silly irresponsible grasshopper) when the future comes you will have an abundance to enjoy and your winter will be more like a gorgeous phantasmagorical riot of spring blossoms. Because you, my little friend, prepared for it.   This is the priority based budget. And it is a great tool to use to help you realize just what your priorities are and exactly where you want your money to go (and, maybe even more importantly, not to go). I could look at where your money is going and give you an idea of where you might be able to trim the fat and the things that I would not “waste” my money on, but at the end of the day it is your money to choose to spend as you will. Of course if you are looking to save money you cannot “choose” to keep spending on all the things you have been spending it on. This is where the priority based budget comes in as a tool to help you with that decision making process. The concept is very simple. You start with the most important things that you want your money to go for. And here we are not talking about the things you “want” the most. We are talking about your most basic needs. You also start with the amount of money you bring in for the month. As you list each expenditure you subtract that amount from your monthly income. So you would start with things like housing (rent or mortgage, and property taxes if applicable), food, electricity, water, heat, insurance, and then continue down the list to “lesser” but necessary to your life expenditures. And as you do this you continue to subtract from your monthly income. By the time you get to the bottom, depending on what your income is you should be getting to your “want” items in order of which things you want the most. When you get down to zero on the other side you are done. You can’t (or I guess I should say shouldn’t) spend money that is not coming in, because this is, of course, what leads to debt. Everyone has different priorities and what would be a frivolous expenditure in my eyes may be a very important source of joy and happiness for you. But the bottom line (zero) is the bottom line no matter what your circumstances are. You cannot go beyond that and this is what forces you to examine what your spending priorities are.  If your money is very tight, you may not even get past the “needs” at the top of the budget. There is no room for “wants” at all. If this is the case you will need to examine how you can increase your income. You can temporarily take on a second job, but you will also need to come up with a more permanent solution to your income dilemma. Can you ask for a raise? Look for a better job in your field? Should you try a different line of work? Get additional education? You need to come up with a plan of action, and start taking the necessary steps to get there. If you have debt, then paying that off should go right after your basic needs are met. If you do not have debt, then you are in a position to start saving and that savings should be at the top of your line items. Retirement savings being at the top, followed by other savings goals. i.e. a wedding, a house, kids (or your own) education, a car, vacation, home improvements, etc. This is the concept of “Pay yourself first” and it works! This way you have all your life goals covered by the time you get down to the bottom of the budget to those everyday “wants”. I have included some budget worksheets that you can use to create your own Priority Based Budget. One has categories to give you some guidelines (but feel free to change them according to your own priorities). And some samples to help you see how it's done: Sample 1. Sample 2. The other is left blank for you to fill in as you see fit. And more samples: Sample 3. Sample 4 The lefthand column of both of them is for you to start with your monthly income and then subtract as you make your way down your list of spending priorities until you get to zero at the bottom... money gone... budget done! You must of course (if you are sensible and want to get ahead with your money) include your saving goals as part of your monthly budget and also things that you will not necessarily spend money on every month, but that you will do so from time to time (like car or home repairs).  Once you finish with this exercise you will have a clear black and white picture of where your money is going according to your own life’s plan. You are on top of your money. You are in control. And that’s a pretty darn good feeling! Congratulations!   Here’s the biggest mistake almost all people make when it comes to savings: They pay their bills, buy their food, make repairs, buy things for the house, pay for kid’s activities, go shopping for clothes, go to the movies, go out to eat, go shopping for some new clothes, etc., etc., and then save what’s left over at the end of the month. Can you see the problem with this? Is there ever anything left at the end of the month?? Many people will also say that they live paycheck to paycheck, but here is the interesting thing about this; They are saying this no matter what the size of their paycheck. The person who makes $300/wk. is saying it and so is the person who makes $600/wk. and the one who makes $3,000/wk. and on up. Right up to that athlete or rock star who is making several million dollars a year and blowing it all, only to go bankrupt when the income dries up. It seems to be just human nature to live just up to your income level whatever that may be, or even a little above that (accounting for all the debt people tend to find themselves in). But if you want to save money the only way you can do it is by living below your means, whatever they may be. Another way to put this is: You don’t save money by how much you make, but by how much you don’t spend. The great investment “guru” Warren Buffet puts it this way:  This is great advice, but how do you do it? Well the great US of A knows how. You pay taxes every year, right? Does Uncle Sam just let you have your full pay and then ask you to cough up the taxes on April 15th? You bet your sweet bippy he doesn’t, because he knows what would happen. People adjust their lifestyle to however much money is coming in. So he just takes his cut up front and people adjust to living on what’s left. Well you can do the same thing for yourself. Just take it off the top. The U.S. government even gave people a means to do just that by starting the 401K program, giving you a tax advantage and a way for you to save money by skimming it right off your paycheck without even ever seeing the money. If you have this offered at your place of employment you should certainly be taking advantage of it. Some generous companies will even match your contribution dollar for dollar up to a certain amount. Free money! Never pass up this opportunity! But even if you don’t have the opportunity for a 401K (or 403B, TSP, etc.), you can still make the magic of automatic savings work for you. All you have to do is set it up once for yourself and done. Savings skimmed right off the top. Out of sight, out of mind. You will quickly adjust to living on what remains. How you set this up depends on what you are saving for. Your first savings goal should be your retirement. I know this sounds kind of backward or counterintuitive, but because you need such a large amount, and because it makes such a difference when you start compounding that interest early, it is imperative that you start this ASAP! If you don’t have a 401K then you can set up your own retirement account in a Roth IRA. I recommend you do this by opening up a discount brokerage account at a firm such as Fidelity or Vanguard. This gives you many options on what to invest your money in inside of your Roth IRA and gives you complete control over it. Once you have your Roth set up it is quite simple to set up automatic payments of whatever amount you choose monthly going from your checking account into your IRA. Whether you have a 401K in the workplace or your own Roth IRA, you can also set up similar automatic payments going into (online) savings accounts for your other savings goals (wedding, car, house down payment, education, etc.) Once you have your savings goals set up automatically in this way, you no longer have to stress about money. You are all set for your future needs both short and long-term, and you can spend what’s left freely. Won’t that be a nice feeling!   In January and February, we talked about getting organized with your expenses and setting some financial goals for yourself. I discussed the importance of keeping track of your expenses and setting up a monthly budget. Hopefully, you are now getting a better idea of where your money is going and are starting to feel more on top of your financial life. Perhaps this has lead you to make some changes in what you are spending your money on and how much is going out each month. If that is the case, good for you, you are on your way!  Now that winter is over and you are feeling more energetic and ready to give your house a good cleaning and get out there and clean up your yard to make way for the beautiful spring growth and flowers, you can also do some spring cleaning of your finances. Just as you declutter your house of unwanted extra stuff for a more peaceful environment and clean up all that yard debris for a tidier look, you can also take a look at your finances to clear out those unnecessary expenses that are keeping you from reaching your savings goals and from the peace of mind of living below your means. Once you are organized and are keeping track of your expenses, then you can begin to go over them with a fine tooth comb and start eliminating the financial clutter. Simplify your spending! There are probably at least a few things that you have gotten into the habit of buying that you can do without. And there are probably a few things that you are spending more money on than is necessary. How quickly or gradually you go about this financial downsizing is entirely up to you. Maybe you are the type that likes to get used to things slowly, and form new habits one at a time before making the next change, or maybe you like to see the rapid results of all that “found” money you can have (to pay off debts or start saving money more quickly) when you really pare down your budget all at once. Proceed at your own style and pace. Eliminating a few (or more than a few) daily or weekly expenses can really add up to big savings. Here are a few examples of how small savings can add up:  But don’t overlook those big (typically monthly) expenses too. Take a look at your phone plan, your utility usage and company, TV and internet providers, car/homeowners insurance. Shop around to see if you can get a better deal. Sometimes all it takes is the threat of moving on to spur your present company to offer you a sweeter deal. Even think about your mortgage or rent payments. Can you downsize? Refinance? Get a roommate? Once you eliminate a lot of that spending clutter your psyche will feel lighter, and your wallet and bank account will now be able to grow and thrive like those beautiful spring flowers. It’s a good deal all around. Give it a try!   I am so excited to welcome you to my new webpage and get started on a money saving journey with my readers. This blog will be chock full of tips and strategies each month that you can use to set and achieve any and all of your financial goals from the short term to long term to the ultimate of a secure, happy, well-funded retirement and even a legacy to leave to your heirs. The new year is traditionally a time of getting started so this is the perfect time to take a look at where you stand right now with your finances and what goals you would like to achieve this year and beyond. No matter where you are at present the best time to get started on improving your financial status is right now! Before you can begin to set goals it is important to know where you are right now. Set aside some time to take a look at where your money is going. Write out an expense sheet. Include all your expenses big and small, from your fixed expenses (rent/mortgage, insurance, cable, phone, etc.) to your more variable expenses (food, heat, gas, clothing, entertainment, etc.). And don’t forget the occasional expenses (school supplies, Christmas, vacations, car repairs, etc.), as well as all those little expenses that you hardly think about (your morning coffee to-go, vending machine treats, lunches out, beauty products, etc.). If you are not in the habit of noting all your expenses, it may take some time to remember them all. I suggest getting a little notebook to record what you spend money on each day at least for a month. (Even I still do this on a daily basis.) You can use this worksheet I've made to complete this step.  In the meantime, take stock of any debt you have. Write down all of your debts including the full amount owed and the interest rates. Add them up to get your total owed. If you have assets, good for you! Take note of them too. Money in the bank? 401k (403b)?, Any investments? And write down what your income is, including all sources; Your (and your spouse’s) salary, child support, SS payments, rental income, extra side jobs, etc. Now that you have a clear picture of where you stand, you can plan your goals. Let me give you a little hint here. Your first goal should be to pay those debts down! No debts? Great! Is there something you want to save up for to buy this year? Do you have a bigger purchase in mind that might take a few years to save up for? (a new car or down payment on a house?) Do you want to save up for education? (yours or your kids). And then of course there is the ultimate goal, that nice comfortable retirement nest-egg! For the smaller goals it is simply a matter of dividing the total needed by the months you have until you need the money. Then you know the exact amount you need to put away each month to achieve it. For that ultimate big retirement reward, slow and steady wins the race. The earlier you start the better off you will be. This should be an automatic amount taken right off the top, before you even see it. Of course a job 401k will do this for you, but if you don’t have access to one you can set up your own retirement account and have automatic deductions going straight into it from your checking or savings account each month. I know this is a lot to contemplate all at once, but for now just take this month to take stock of your expenses and debts, and think about what goals you might have for your money and I will lead you through the rest of it step by step as the year progresses. When you do it step by step you will see how easy it can actually be to turn your finances around. We will start to talk next month about just how to budget your expenses and find the money to put aside for all those goals. ` Stick with me and you too can have a bright future!  |

Archives

June 2022

Categories

All

|

RSS Feed

RSS Feed