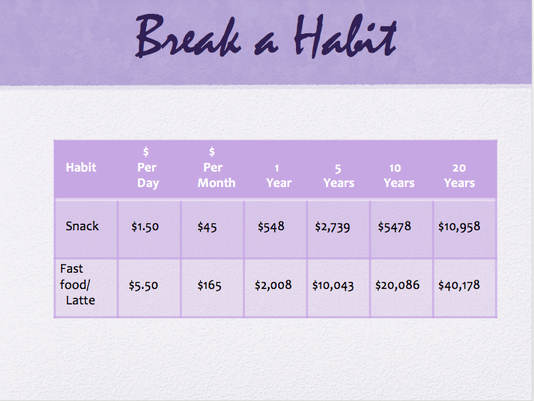

In January and February, we talked about getting organized with your expenses and setting some financial goals for yourself. I discussed the importance of keeping track of your expenses and setting up a monthly budget. Hopefully, you are now getting a better idea of where your money is going and are starting to feel more on top of your financial life. Perhaps this has lead you to make some changes in what you are spending your money on and how much is going out each month. If that is the case, good for you, you are on your way!  Now that winter is over and you are feeling more energetic and ready to give your house a good cleaning and get out there and clean up your yard to make way for the beautiful spring growth and flowers, you can also do some spring cleaning of your finances. Just as you declutter your house of unwanted extra stuff for a more peaceful environment and clean up all that yard debris for a tidier look, you can also take a look at your finances to clear out those unnecessary expenses that are keeping you from reaching your savings goals and from the peace of mind of living below your means. Once you are organized and are keeping track of your expenses, then you can begin to go over them with a fine tooth comb and start eliminating the financial clutter. Simplify your spending! There are probably at least a few things that you have gotten into the habit of buying that you can do without. And there are probably a few things that you are spending more money on than is necessary. How quickly or gradually you go about this financial downsizing is entirely up to you. Maybe you are the type that likes to get used to things slowly, and form new habits one at a time before making the next change, or maybe you like to see the rapid results of all that “found” money you can have (to pay off debts or start saving money more quickly) when you really pare down your budget all at once. Proceed at your own style and pace. Eliminating a few (or more than a few) daily or weekly expenses can really add up to big savings. Here are a few examples of how small savings can add up:  But don’t overlook those big (typically monthly) expenses too. Take a look at your phone plan, your utility usage and company, TV and internet providers, car/homeowners insurance. Shop around to see if you can get a better deal. Sometimes all it takes is the threat of moving on to spur your present company to offer you a sweeter deal. Even think about your mortgage or rent payments. Can you downsize? Refinance? Get a roommate? Once you eliminate a lot of that spending clutter your psyche will feel lighter, and your wallet and bank account will now be able to grow and thrive like those beautiful spring flowers. It’s a good deal all around. Give it a try!

0 Comments

If you are of a normal weight like I am, people will sometimes say to you “Oh, you are so lucky you don’t have to worry about your weight.” Or even more erroneously, “You are so lucky you can eat whatever you want.” Neither of these statements can be further from the truth. In fact, the only reason I am a normal weight is because I do worry about my weight, every day. And I do watch what I eat, every meal. It is just as much a struggle for me as for them. In fact, probably more so, given the fact that I am only 4’10” making every calorie count!

So what does that have to do with money, you ask? Well, I have also had people say to me, "Oh you are lucky that you were able to stay home with your kids and did not have to go out and work." And once again, luck had very little to do with it. Many of the women who said this to me had husbands who were making more money than mine did. These women also had cable TV, big new SUV’s or minivans, new clothes and shoes, maybe a Coach bag, and (back in the day when I had dial-up) high-speed internet. I would wager a bet that they also thought nothing of going out to lunch, buying coffee and drinks out, getting their nails and hair done, and picking up take-out for dinner. And yes, before you start yelling at me, I know there are single moms or other circumstances when women need to work, but my point is that often what people perceive as luck may actually be a result of the many choices made every day in life. Luck can also be a matter of perception in another way. Let’s say you get in a car accident and break your arm. Are you lucky or unlucky? Well, some might say of course you are unlucky! You got into a car accident and broke your arm for goodness sake! How can that be lucky? But then there is the person who says, “I am so lucky that all I got was a broken arm! I am still alive!!” Same scenario. Completely different perspective. So what is luck then? It is a matter of the results of your actions, and a matter of perception. So, the question is can you create your own “luck”? You absolutely can! Let me create a little story for you to illustrate my point even further: Let’s say Dick and Jane make the exact same amount of money. OK, scratch that, since Dick probably makes more. Let’s say Dixie and Jane make the exact same amount of money and through some cosmic fate have the exact same bills and expenditures every month. Each is able to save up exactly $100 per month after everything is paid, giving them each an extra $1,200 per year. At the end of Year One, Dixie takes that money and goes on a much-deserved vacation. Jane puts it in a one-year CD. At the end of Year Two, Dixie needs some new living room furniture, so she spends her $1,000 on that plus $200 on a hot new outfit. Jane now has $2,424 (her yearly savings of $1,200 plus $1,242 in her CD). She puts $2,200 of it into another CD, and spends $30 on a water filter for her tap, so she can stop buying bottled water, and spends $70 on an indoor antenna for her TV and cancels her $110 per month cable service. With the remaining $124 she has a great time at the thrift shop buying a new wardrobe for the coming year. Year Three: Dixie has her usual $1,200 at the end of the year. She splurges on buying herself the latest iPhone, which is just out, plus a nice case for it. Jane now has $2,244 from her CD, plus $350 saved by not buying bottled water, plus $1,320 saved by not paying for cable every month, plus her usual $1,200 for the year. A total of $5144. She spends $800 buying a washer and dryer so that she can stop going to the laundromat. She decides to invest the remaining $4,344 into a low-cost index mutual fund. At the end of Year Four, Dixie has her usual $1,200. Jane has her usual $1,200 plus $350 saved on water, plus $1320 saved on cable, plus $180 saved on laundry. And her mutual fund did pretty well to earn her 8%, so she now has $4,691 in that for a total of $7,741 … I could go on and on, but I hope you are starting to get the picture. One night Dixie meets Jane at a party. When the topic turns to finances, Jane happens to mention that she currently has about $3,000 in her savings account plus a mutual fund with over $4,500. Dixie is impressed and amazed and comments on how “lucky” Jane is to be so far ahead of her, while she, herself struggles living paycheck to paycheck. Does this sound familiar? Is Jane “lucky”? So how about starting to turn your own “luck” around. And one day in the future maybe you will chuckle inwardly when someone at a party tells you how lucky you are to have such a nice healthy nest-egg for your retirement and a nice bright future to look forward to. |

Archives

June 2022

Categories

All

|

RSS Feed

RSS Feed