This is the priority based budget. And it is a great tool to use to help you realize just what your priorities are and exactly where you want your money to go (and, maybe even more importantly, not to go). I could look at where your money is going and give you an idea of where you might be able to trim the fat and the things that I would not “waste” my money on, but at the end of the day it is your money to choose to spend as you will. Of course if you are looking to save money you cannot “choose” to keep spending on all the things you have been spending it on. This is where the priority based budget comes in as a tool to help you with that decision making process. The concept is very simple. You start with the most important things that you want your money to go for. And here we are not talking about the things you “want” the most. We are talking about your most basic needs. You also start with the amount of money you bring in for the month. As you list each expenditure you subtract that amount from your monthly income. So you would start with things like housing (rent or mortgage, and property taxes if applicable), food, electricity, water, heat, insurance, and then continue down the list to “lesser” but necessary to your life expenditures. And as you do this you continue to subtract from your monthly income. By the time you get to the bottom, depending on what your income is you should be getting to your “want” items in order of which things you want the most. When you get down to zero on the other side you are done. You can’t (or I guess I should say shouldn’t) spend money that is not coming in, because this is, of course, what leads to debt. Everyone has different priorities and what would be a frivolous expenditure in my eyes may be a very important source of joy and happiness for you. But the bottom line (zero) is the bottom line no matter what your circumstances are. You cannot go beyond that and this is what forces you to examine what your spending priorities are.  If your money is very tight, you may not even get past the “needs” at the top of the budget. There is no room for “wants” at all. If this is the case you will need to examine how you can increase your income. You can temporarily take on a second job, but you will also need to come up with a more permanent solution to your income dilemma. Can you ask for a raise? Look for a better job in your field? Should you try a different line of work? Get additional education? You need to come up with a plan of action, and start taking the necessary steps to get there. If you have debt, then paying that off should go right after your basic needs are met. If you do not have debt, then you are in a position to start saving and that savings should be at the top of your line items. Retirement savings being at the top, followed by other savings goals. i.e. a wedding, a house, kids (or your own) education, a car, vacation, home improvements, etc. This is the concept of “Pay yourself first” and it works! This way you have all your life goals covered by the time you get down to the bottom of the budget to those everyday “wants”. I have included some budget worksheets that you can use to create your own Priority Based Budget. One has categories to give you some guidelines (but feel free to change them according to your own priorities). And some samples to help you see how it's done: Sample 1. Sample 2. The other is left blank for you to fill in as you see fit. And more samples: Sample 3. Sample 4 The lefthand column of both of them is for you to start with your monthly income and then subtract as you make your way down your list of spending priorities until you get to zero at the bottom... money gone... budget done! You must of course (if you are sensible and want to get ahead with your money) include your saving goals as part of your monthly budget and also things that you will not necessarily spend money on every month, but that you will do so from time to time (like car or home repairs).  Once you finish with this exercise you will have a clear black and white picture of where your money is going according to your own life’s plan. You are on top of your money. You are in control. And that’s a pretty darn good feeling! Congratulations!

0 Comments

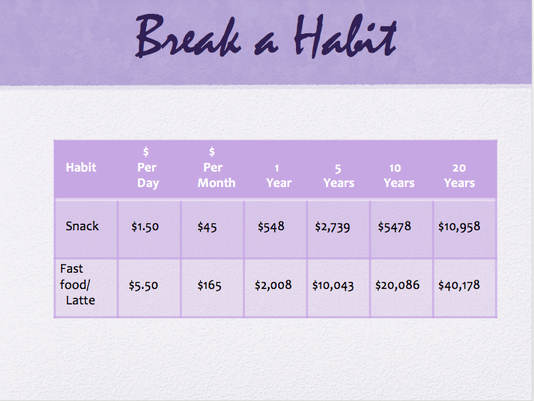

Ah Amore! The month of love. Hallmark, Brachs, Godiva, florists, and all fine jewelry stores, even those romantic getaways and restaurants are eagerly awaiting it! How much do you love your sweetie? Open up your wallet and show them! The ads make it abundantly clear. As James Taylor crooned, “Shower the people you love with love. Show them the way that you feel.” In our society of commercialism, stuff and abundance, it’s just another occasion to sucker you in to buy even more. This one carries a particular guilt trip. If you love your honey how can you not show them through valuable merchandise? What kind of a heartless cad are you?  And, of course, Hallmark, et al, went beyond just your particular heartthrob to include the whole dang family in the celebration. From the kiddies all exchanging valentines in school (which, through the years, went from homemade hearts to purchased cards to candy and treats), to cards and gifts made for every one of your beloved family members. Don’t leave anyone out! And just a card (which now can run upwards of $7)? No way! What about the candy? The flowers? The stuffed animals? The jewelry? Showing everyone in your family that you love them can run a pretty good chunk of change! So … my challenge to you is this: Why do we have to spend all this money (mostly on crap that will someday become part of the landfill) to “prove” to our families that we love them? Just because Hallmark told us to? Because companies want to make money selling us their products?  Where does it all end? It escalates year after year, holiday after holiday. The only place it can end is with you and me. We must all realize that how much you spend on a person does not equal how much you love them, especially when what you spend on them is for meaningless junk. If you are married or in a committed relationship with someone, you should be working together to make the most of your money, live below your means and save. Work together to make the holiday special. Make a special meal together, go on a sunset stroll somewhere, watch a romantic movie at home (free from the library!) Surprise your spouse with a heart-shaped cake you baked. A heartfelt letter written to them about how much you love them and why would certainly be more appreciated than something some greeting card writer came up with.    And as for the kiddos, yes you can shower them with gifts. In fact, you can shower them with gifts for all of the many Hallmark gift giving occasions that have sprung up throughout the calendar year, but what exactly are you teaching them? What are you creating? Perhaps you might want to think about what kind of adults you would like to raise them to be. What kind of expectations are you setting up for them? If you really feel you must note the occasion, how about making some heart shaped cookies and having fun frosting them together? Keep it simple. Resist the impulse to go overboard. That impulse is what got us into this overspending mode in the first place.  Yes, Amore! Love is a many splendored thing. We should tell our love ones that we love them, not just in February but always. And finding special ways to show them that we love them is a very sweet thing to do. Little love notes and special surprises are always cherished and appreciated, and go a long way towards keeping the love alive. But the danger comes in equating how much we spend, especially on things dictated to us by outside forces and advertising, with how much we love them. Make love, not debt!   If you’re still with me as I lead you on this years-long journey toward getting on the road to financial solvency and freedom, then you are well on your way. Congratulations for sticking with it! If you are just joining me and are new to this blog, it would be a good idea to go back and read the monthly posts for 2018. They will give you a good foundation for learning how to gain control of your own financial journey, alleviating debt if you have it, and how to start saving for your own bright future. It’s not as hard as you might imagine and I hope you will come to find the frugal life to be as fun and satisfying as I do. I know you will enjoy seeing your savings grow as a result of the lifestyle changes I am recommending. This month the holidays are behind us. Hopefully you had a frugal celebration and did not overspend. If you have, then your best bet is to concentrate on getting out from any debt you have incurred as quickly as you can! This may sound counterintuitive, but if you have gotten a good handle on your spending, and are staying out of debt… January is a good month to SHOP the sales! There are the after-Christmas sales of course, if you need any of that (I rarely buy any of that stuff anymore, as you will read about next December). But there are many other reduced ticket items to be had in January.  First of all, this is when the winter clothes (and other winter items) start hitting the clearance racks. NOW is the time to buy these items for next Christmas! You can get half your shopping done at a fraction of the cost of waiting until next December. And if there are any winter clothing items you need, keep an eye out on the clearance racks for that too. The operative word here is “need”, of course. This is not a time for recreational spending. In fact, no time is a time for recreational spending. It should not even be a thing. Certainly not if you want to live below your means and get ahead.  Other things that go on sale in January are bedding and towels. If yours are getting threadbare, now is the time to think about replacing them. (They're also another holiday gift possibility.) Again, not just because you’re tired of the color of your perfectly good sheets, towels, etc. And don’t forget to keep the old ones as rags (eliminating the need for buying paper towels).  If you having been saving up to replace some big ticket items (think furniture and appliances) there are often sales in those departments too at this time of year. But if you don’t have the money saved, a sale is not an excuse to put it on a credit card! One year our fridge went on the fritz in October or November, but the freezer was still working, so we patched together a system of using coolers in the cold outdoors, and froze water bottles to put in the defunct fridge to use as a giant indoor cooler. And this system got us through the holiday (spending) season, until the appliances went on sale in January and we got ourselves a sweet deal on a new refrigerator (which we paid cash for, of course!)  So there you have a few examples of spending money to save money. There are times when careful spending will actually save you money in the long run. And I am not talking here about telling people that you “saved” $100 by buying your new ($500) wardrobe on “sale”. I am talking about some well- spent money now that will save you from going into a shopping frenzy next Christmas and buying those same items at three or four times the clearance price you are getting them at now. Wishing you all a Happy New Year and (rare to hear from me) happy shopping!   Tis the season …for exuberance, generosity and joyful abandonment. It’s so very festive and fun, but oh so easy to get carried away with it all. And temptations to spend are everywhere you look. Deep discounts! Drastically reduced! Prices slashed! The more you buy the more you save! …. Or do you? It certainly doesn’t seem like it when the bills roll in come January … right around the time when you’re making those New Year’s resolutions, it seems. You know, the ones about getting on a budget and stopping the overspending? So, what are some strategies that you can employ to obtain that simple peaceful holiday season and reign in the excess spending? The first thing you can do is pare down those lists. Of people to buy for, indulgences, activities, and, of course, presents to buy. Well, now is the time to stop and think about that. Take a deep breath, have a cup of tea and sit down and contemplate a quieter, simpler, less hectic holiday season. One that you won’t regret when the new year rolls around. One that you’re not paying for until next August. Does that thought bring you joy? Do you feel your blood pressure dropping already?  Sometimes the amount of people we exchange with can become out of hand. What starts out as a nice gesture one year, exchanging with this friend or that relative eventually morphs into a yearly obligation. You may be surprised to find that the other person in this exchange feels the same way and is more than happy to drop the yearly gift swap. Talk to them. Often we also have auxiliary people in our lives to favor with a gift, from teachers to work-related people to babysitters and hairdressers, etc. Many times these people are also swamped with all those many little gifts at holiday time, and though the thought is appreciated they would rather not deal with the deluge. Sometimes a kind and heartfelt note of appreciation is most welcome. If you feel you must give something, make up a big batch of your holiday specialty (cookies, candy, fudge, whatever) and parcel a little out to each of the people in your life that you need to thank. One and done. And edibles are often more appreciated than extra objects to clutter up their lives. Besides paring down the list of people that you exchange with, it is also a good idea to pare down the amount of gifts exchanged. This especially applies our beloved and cherished little offspring. I know it can be so fun to spoil them and see their happy faces when they open that pile of gifts, but is it worth going into debt for? And is it really good for them in the grand scheme of things?  ‘ Have you ever noticed that the more gifts children get the less they are actually appreciated? If they open, open, open more and more gifts the presents themselves become secondary to the act of tearing into the innumerable presents. Is this greedy abandonment really the kind of “happiness” you want for your child? Just a few thoughtful gifts might instill a more genuine thankfulness in your child. My last gift giving tip comes too late for this Christmas, but is certainly something you can start for next Christmas. That is to prepare for the holidays all year, both in your spending and your buying. The old fashioned “envelope system” works great here. Just deposit a little bit out of each paycheck and let that be your holiday budget for next year. Pay cash for your presents and other holiday expenses, and when the money’s gone it’s gone. No more spending. And no credit card bills to fret over in January. You can also spread out your buying for the entire year. Look for those after-Christmas sales. Take advantage of clearance sales throughput the year. And one of my favorites, yard sales and thrift shops. I used to pick up gifts for my kids (often still in the box or with tags on) all summer at yard sales and my Christmas shopping was almost done (for dirt cheap) by October except for a few requested items to round out the list. This works especially well with smaller kids who are not as particular as older kids can get. You can sometimes score presents for the adults on your list this way too (keep them in mind when you look around). So, yes, Virginia (or whatever your name is), you can have a joyous holiday season without going into debt for it. In fact, I might venture to say that you can have an even more joyous and peaceful holiday when you keep it simple and take this time to relax and enjoy yourself with your family and friends without all that frenzied spending. Give it a try. You have nothing to lose and lots to gain! Wishing you all a warm and wonderful holiday and a peaceful and prosperous new year!   In January and February, we talked about getting organized with your expenses and setting some financial goals for yourself. I discussed the importance of keeping track of your expenses and setting up a monthly budget. Hopefully, you are now getting a better idea of where your money is going and are starting to feel more on top of your financial life. Perhaps this has lead you to make some changes in what you are spending your money on and how much is going out each month. If that is the case, good for you, you are on your way!  Now that winter is over and you are feeling more energetic and ready to give your house a good cleaning and get out there and clean up your yard to make way for the beautiful spring growth and flowers, you can also do some spring cleaning of your finances. Just as you declutter your house of unwanted extra stuff for a more peaceful environment and clean up all that yard debris for a tidier look, you can also take a look at your finances to clear out those unnecessary expenses that are keeping you from reaching your savings goals and from the peace of mind of living below your means. Once you are organized and are keeping track of your expenses, then you can begin to go over them with a fine tooth comb and start eliminating the financial clutter. Simplify your spending! There are probably at least a few things that you have gotten into the habit of buying that you can do without. And there are probably a few things that you are spending more money on than is necessary. How quickly or gradually you go about this financial downsizing is entirely up to you. Maybe you are the type that likes to get used to things slowly, and form new habits one at a time before making the next change, or maybe you like to see the rapid results of all that “found” money you can have (to pay off debts or start saving money more quickly) when you really pare down your budget all at once. Proceed at your own style and pace. Eliminating a few (or more than a few) daily or weekly expenses can really add up to big savings. Here are a few examples of how small savings can add up:  But don’t overlook those big (typically monthly) expenses too. Take a look at your phone plan, your utility usage and company, TV and internet providers, car/homeowners insurance. Shop around to see if you can get a better deal. Sometimes all it takes is the threat of moving on to spur your present company to offer you a sweeter deal. Even think about your mortgage or rent payments. Can you downsize? Refinance? Get a roommate? Once you eliminate a lot of that spending clutter your psyche will feel lighter, and your wallet and bank account will now be able to grow and thrive like those beautiful spring flowers. It’s a good deal all around. Give it a try!   If you are of a normal weight like I am, people will sometimes say to you “Oh, you are so lucky you don’t have to worry about your weight.” Or even more erroneously, “You are so lucky you can eat whatever you want.” Neither of these statements can be further from the truth. In fact, the only reason I am a normal weight is because I do worry about my weight, every day. And I do watch what I eat, every meal. It is just as much a struggle for me as for them. In fact, probably more so, given the fact that I am only 4’10” making every calorie count!

So what does that have to do with money, you ask? Well, I have also had people say to me, "Oh you are lucky that you were able to stay home with your kids and did not have to go out and work." And once again, luck had very little to do with it. Many of the women who said this to me had husbands who were making more money than mine did. These women also had cable TV, big new SUV’s or minivans, new clothes and shoes, maybe a Coach bag, and (back in the day when I had dial-up) high-speed internet. I would wager a bet that they also thought nothing of going out to lunch, buying coffee and drinks out, getting their nails and hair done, and picking up take-out for dinner. And yes, before you start yelling at me, I know there are single moms or other circumstances when women need to work, but my point is that often what people perceive as luck may actually be a result of the many choices made every day in life. Luck can also be a matter of perception in another way. Let’s say you get in a car accident and break your arm. Are you lucky or unlucky? Well, some might say of course you are unlucky! You got into a car accident and broke your arm for goodness sake! How can that be lucky? But then there is the person who says, “I am so lucky that all I got was a broken arm! I am still alive!!” Same scenario. Completely different perspective. So what is luck then? It is a matter of the results of your actions, and a matter of perception. So, the question is can you create your own “luck”? You absolutely can! Let me create a little story for you to illustrate my point even further: Let’s say Dick and Jane make the exact same amount of money. OK, scratch that, since Dick probably makes more. Let’s say Dixie and Jane make the exact same amount of money and through some cosmic fate have the exact same bills and expenditures every month. Each is able to save up exactly $100 per month after everything is paid, giving them each an extra $1,200 per year. At the end of Year One, Dixie takes that money and goes on a much-deserved vacation. Jane puts it in a one-year CD. At the end of Year Two, Dixie needs some new living room furniture, so she spends her $1,000 on that plus $200 on a hot new outfit. Jane now has $2,424 (her yearly savings of $1,200 plus $1,242 in her CD). She puts $2,200 of it into another CD, and spends $30 on a water filter for her tap, so she can stop buying bottled water, and spends $70 on an indoor antenna for her TV and cancels her $110 per month cable service. With the remaining $124 she has a great time at the thrift shop buying a new wardrobe for the coming year. Year Three: Dixie has her usual $1,200 at the end of the year. She splurges on buying herself the latest iPhone, which is just out, plus a nice case for it. Jane now has $2,244 from her CD, plus $350 saved by not buying bottled water, plus $1,320 saved by not paying for cable every month, plus her usual $1,200 for the year. A total of $5144. She spends $800 buying a washer and dryer so that she can stop going to the laundromat. She decides to invest the remaining $4,344 into a low-cost index mutual fund. At the end of Year Four, Dixie has her usual $1,200. Jane has her usual $1,200 plus $350 saved on water, plus $1320 saved on cable, plus $180 saved on laundry. And her mutual fund did pretty well to earn her 8%, so she now has $4,691 in that for a total of $7,741 … I could go on and on, but I hope you are starting to get the picture. One night Dixie meets Jane at a party. When the topic turns to finances, Jane happens to mention that she currently has about $3,000 in her savings account plus a mutual fund with over $4,500. Dixie is impressed and amazed and comments on how “lucky” Jane is to be so far ahead of her, while she, herself struggles living paycheck to paycheck. Does this sound familiar? Is Jane “lucky”? So how about starting to turn your own “luck” around. And one day in the future maybe you will chuckle inwardly when someone at a party tells you how lucky you are to have such a nice healthy nest-egg for your retirement and a nice bright future to look forward to. |

Archives

June 2022

Categories

All

|

RSS Feed

RSS Feed