|

Drinks:  1. Coffee. It is so much cheaper to brew it at home  1. Water. After drinking water from a tap for much of my formative years, I was gobsmacked when the beverage companies convinced a whole society of people that they should pay for it in a bottle. That was quite a feat of marketing as far as I’m concerned. Guess what folks, it’s still available from your kitchen sink! Get a reusable bottle for when you go out.  1. Soft drinks. Terrible for your teeth and your health and your waistline.  1. Fruit drinks. Might seem like they are healthier than soda but they really aren’t. It is still a sugary liquid. Even the ones made from “100% fruit juice” are just the sugar of the fruit without the benefits of all the fiber that you would be getting from eating that actual fruit. Eat the fruit!  1. Tea. I do drink tea on a daily basis, but made from my own tea bags at home, or sometimes even from herbs (lemon herb) from my garden. And (don’t get all judgy now) I reuse the teabags several times before I am done with them.  Alcoholic beverages. Rather than going to happy hour and spending upwards of $5 per drink (often way upwards), buy the ingredients and have a cocktail hour at each other’s houses. It is way cheaper and just as fun. When you go out to dinner if you must have a drink, at least limit yourself to one.I only drink water (and tea)… from my kitchen tap. It’s free and it’s much healthier.  Oh, well, full disclosure (I am human), I do enjoy an occasional cocktail… at home, or at a friend's house. And, yes I do often order a drink on the (rare) occasion that I go out to dinner (but never more than one). I have never really added it up, but I’m sure I’ve saved a ton of money just by not buying drinks over the course of my lifetime. And I don’t feel like I “missed out” on a thing by living this way. Try it. You may be surprised by how much money you can save with just this one change in your spending habits!  Here's to a bright future!

0 Comments

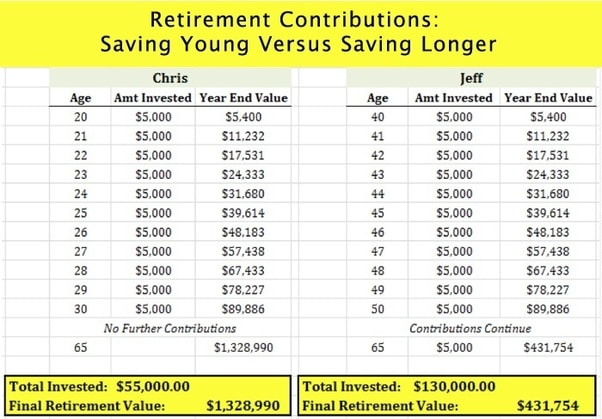

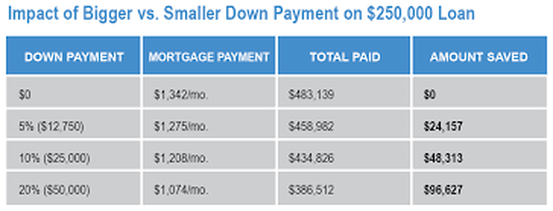

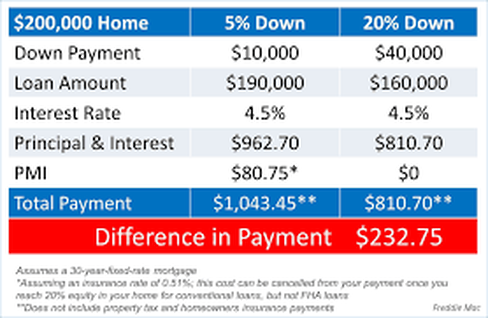

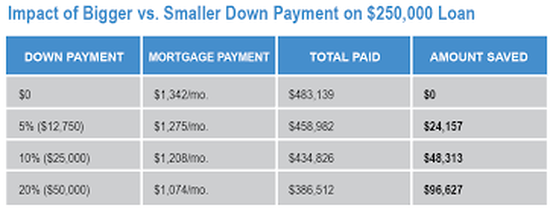

I’ve seen or heard this question posted in many different ways throughout the years, the gist of it being that one needs to make a fundamental decision between enjoying their life or saving for the future. I’ve heard the argument that you must “live” for today because you could be hit by a bus tomorrow. Young people have screamed YOYO! (Did I just coin that?), as in, “You’re Only Young Once”. They maintain that they must spend and “live” for today while they are young enough to enjoy it.  But I don’t see it as a black and white, either/or situation: Save OR have fun. I believe that if you are wise with your money you can do both. Saving your money does not mean that you have to be a miserly scrooge sitting in your lonely attic counting your money and never having any fun. In fact, with a little planning and wise money management you can easily have a very pleasurable life and also save for your future at the same time.  The one equation that people need to let go of is “Spending Money = Fun.” There may be some correlation to that sometimes, but it is certainly not a given. You can spend lots of money on something and have a terrible time, and even more importantly it is very possible to have a great time spending no money at all. I’m sure you can think of several examples of both these facts in your own life. Let’s start with the young (my newly coined YOYO philosophy). Yes, they can certainly save and also have fun. First of all, they have one huge advantage in their favor… the magic of compound interest. The fact is if you start saving (investing) early you will only need to save a fraction of your own money in order to build up a very tidy nest egg for retirement. Most of the money in your IRA at retirement will be growth on the returns you accrued through the years (not the money you actually put in). Pretty neat trick, huh?  With a little prioritizing and forethought young folks can also be saving for their other more near-future needs/wants (a car, a house, a wedding, et.) by putting those savings on automatic pilot and just living on what’s left. The prioritizing comes in as you make the conscious decision to forego (instant pleasure X) which is not really adding a great deal of joy to your life in order to save up for that something that will bring you great pleasure indeed.  The one joy that seems to be mentioned a lot is traveling. And here is where the young have another distinct advantage. They can travel for practically nothing, staying in youth hostels, or other low cost accommodations. There are even many temporary internship/job opportunities overseas that can allow them to see the world while sometimes even making a little money. The possibilities of low-cost travel are only limited by the imagination for the young (or young at heart). Google “traveling on next to nothing” and see what you come up with. I read a great memoir on the subject a while back called “No Baggage – A Minimalist Tale of Love and Wandering” by Clara Bensen.  What about if you are not young? I see people of all ages squandering their money on daily instant gratification pleasures without even realizing that they are doing it. Once, when I was telling some friends about a trip to Singapore that I had just returned from, somebody asked me “I don’t understand. You can’t afford cable TV, but you can afford a trip to Singapore?” My answer to that is you can afford anything (within reason, of course), but you can’t afford everything. I chose to forgo all those channels at $150/month in order to save my money for something better. I even found a way to get TV for free (an old fashioned roof antenna). I also put my frugal skills to use to make the trip possible without breaking the piggybank.   If fun is your priority, then go ahead and have it! Have as much as you want. Live! Take advantage of all that free fun that is out there for the taking. If there is some kind of fun that you must have money for, then just look at your spending habits and give something up that does not bring as much joy and save up for what you want.   I see absolutely no reason why you can’t do both. Save and have fun! After all, you only live once!  Wishing you a happy life today and a bright future tomorrow!   Someone I know recently bought a house and my 24-year-old son was asking me about the details. His number one question being “How do people save up that much for a down payment?” As I answered his questions it got me to thinking that I never addressed this topic in these blogs, so here goes:  How do you know when you are ready to buy a house? Well some people think it’s just a matter of saving up that down payment, but really a lot more preparedness needs to go into it. First of all, how settled are you? Many young people move around quite a lot for job changes or other purposes so even if they are very lucky enough to have that down payment at such a young age, it is not necessarily the best time to be putting down roots into home ownership just yet.   Unless you are sure that you will be staying put for at least the next five years, buying a house is rarely a smart move financially. You will sink a lot of money into the act of buying the house (in closing costs, realtors fees, inspections, lawyer’s fees, etc.)  Then once you buy there is the cost of moving in, and often on top of that people will do some work to the house to make it more to their liking. And there is even the inevitable furnishing and decorating, especially if you are starting from “scratch” with nothing.  And if you have put down a small down payment, you will typically not be gaining much equity in the house for the first few years, at least, as most of these initial payments are going to the interest on the mortgage. It is not until the principle starts to go down a little that the mortgage payments will start to chip away at that principle. And of course it also depends on the housing market. Your house could go up in value, giving you more equity but there is also the possibility that it could go down in value and put you in a situation of being “upside down” on your mortgage. That is actually owing more on it than the house is worth. This is what happened to all those people when the housing bubble burst in 2008.   So with all that said, it will take a while before you will get enough principle back when you sell to offset the costs you put in when buying it. If you sell too soon you will not only not gain any money on the sale you could very well come out in the negative for your years of home ownership. If this is the case you would have actually have been better off to continue renting and saving your money. Next, other than that down payment you have saved up, how is your financial situation? Do you have any debts? If you do, it is very smart to pay them off before embarking on your homeownership journey. Do you have an emergency fund (of three to six month’s expenses) saved aside? I would recommend at least six month’s during this transition into home ownership as you never know what can happen. Is your job secure? You don’t want to take on all this extra monthly expense only to be caught high and dry with a loss of income. This type of scenario sends people scrambling and can result in a disastrous situation.  Even if your job is secure, you have a good down payment saved up and you know you will be staying put, have you crunched the numbers to see of you can afford the cost of homeownership? A common mistake people make is this line of thinking. “I am paying X (say $1,500 per month) on my rent so I might as well be paying that amount on a mortgage and actually owning my own home.” The trouble with that is that you must consider all the other costs of owning. Some things that were covered by your landlord before are now your responsibility. Have you thought about taxes, homeowners insurance, (PMI if you have a small down payment), electricity, heat, TV, internet, water, rubbish removal, etc.?  And in addition to all those fixed expenses, if the house is yours, you are now responsible for the upkeep. And no matter what great shape that house was in when you bought it, something always needs attention. Sometimes it seems barely a month goes by without an unexpected household expense. Even non-household expenses can derail you if you are “living on the edge”, just making all your monthly bills without a penny to spare. This is why it is so important to have that emergency fund set up before you move in.  Now what about that down payment? I just mentioned PMI in the previous paragraph. What is that that? If you put less than a 20% down payment then you have to pay Private Mortgage Insurance. And although you are responsible for these premiums this insurance does nothing to protect you. It is to protect the bank from losing the money they lent you should you default on your payments.    So, this brings us to my son’s question. How much of a down payment should you put down and how do you save up that kind of money? The answer to the first question is as much as possible, at the very least 20% (to avoid that PMI) If it’s home ownership you are after (and not living in a bank-owned house that you are paying dearly for (in interest payments) you should set your sights on the biggest chunk of money you can plop down.  Another way to keep your down payment at a higher percentage of the cost of the house is to buy a less expensive house. This way that same down payment you have saved is now a larger percent of the total cost. You can always move into bigger house (or expand the one you are in) down the line should the need arise and your finances improve. Here’s a dirty little secret the banks don’t want you to know. They will approve you of a mortgage that is really out of a comfortable price range for you. Why? Because they are really not interested in how comfortable you are making the payments. They are just looking to get the biggest mortgage for themselves (the more you borrow, the more interest payments they will get). So buy a house that you are comfortable with (monthly payment wise), not what the bank approves you for, and ideally this monthly payment should be no more that ¼ of your monthly income. And one more thing on the subject of mortgages. The bank will automatically default to a 30-year-mortgage, but you are much better off to get a 15-year. The quicker you can get that house paid off, the less total interest you will pay on it. You can save yourself many thousands of dollars (even hundreds of thousands) by just doing this one thing.  Now to Jesse’s question of how to save up for that mortgage. The same way I recommend you save up for anything else. Make it automatic! Open up an online account and set up automatic monthly payments going into it. Take the total amount you want to save and divide it by the months until you want to have the money. If you want to save up a $75,000 down payment in four years that would mean you need to save about $1,500 per month. *See Easy Peasy Make it Automatic  If your timeline for savings is actually more than five years then you might want to consider investing (all or part of) the money into a low cost (relatively safe) mutual fund (such as an S&P 500). Putting those payments away each month will also help you to be living below your income and able to make all those extra expenses when you do move into that house. Owning your own home is the American Dream. It is a great feeling to live in a house of your very own and can also be a real plus to your total financial picture if you are indeed prepared for it, but please make sure you are fully ready before taking the plunge or it has the potential for turning into a nightmare. Do it right and make it your dream come true!  Best of luck to you if you are looking to embark on this exciting new chapter of your story. Wishing you a bright future in your own home sweet home!   I have been talking in this space for years now with tips about how to save money and especially lately, of course, with so many people feeling the financial pinch of this Covid lockdown, saving money has become crucial. But someone posed the very legitimate question of where exactly they should be putting their savings. Some people just keep it in their regular (everyday) checking or savings account. That is not a good idea, and I will l explain why.  You (should) have more than one savings goal for your money, and keeping it in a lump sum actually tricks the mind into thinking you have more money than you do. And for some people this makes it very tempting to spend it. This is the other reason to keep it separate from your everyday money. Once you break it down into the various needs you have for your money you get a more realistic picture of how much you have and how much you still need to save.  Here is a breakdown of some goals you might have and where you should be putting the money for them: #1 Retirement: This can be a 401k or other workplace IRA account, or an IRA you have set up for yourself. At least 15–20% of your income should be going into that. Within that 401k or IRA, the money should be invested, of course. Low cost (index fund) mutual funds are fine. If you want to get fancier than that it is entirely up to you.  #2 An emergency fund: This is especially important in these uncertain times we are going through. If you don’t have a fully-funded emergency fund (at least 3–6 months-worth of expenses), money should be going into this each month. In fact, during this time you might want to beef this up even more. When you reach the 3–6-month goal (or more) then just leave that sitting in a separate account for when you need it. This should be a liquid readily accessible account (not invested).  ,#3 A car fund: Most people own a car and should always be saving towards the next one (paying car payments to yourself) so that you never have to finance one. Get off that car payment carousel! This will save you untold amounts of interest payments thrown away to the bank during the course of your lifetime. If you have no need for a car, then obviously this one does not apply to you,  #4 Other savings goals: I recommend you separate them out into separate accounts. This is anything else you are saving for, a wedding, down-payment on a house, home repairs, trip, kids college, etc.  For most of these savings I recommend you open up an online bank account (or more than one) and then set up automatic payments going into them (from your regular checking/saving account), calculating how much you will need for that goal and the amount of time you have to save for it. I suggest this for two reasons. One, the online banks have a slightly higher interest rate than brick and mortar’s do, and two, they are (at least psychologically) less accessible (out of sight/out of mind), so you will be less tempted to dip into them. And labeling them with a certain goal makes them more “off limits” to impulse spending too.  One more thing. If any of these goals is on a long-range timeline (you will not be needing this money for at least five years or longer), then you might consider buying a (low-cost index fund) mutual fund to be putting that money into for better returns. Since the market is volatile by nature, I would not recommend doing this for any shorter range goals as you risk losing (some of) your money. But for longer range goals, it is a pretty safe bet that, with the usual returns on the stock market, you are likely to do better with this money than putting it into a savings account.  So now you have an exact blueprint of where and how to save your money. Just plug in your particular goals and you can have the whole thing set up in one afternoon. And the beauty of this automatic savings is once it’s done you never have to think about it again. All you have to do is tweak it from time to time as your goals change (and/or are met). You can just get on with your life and stop stressing about money. And that’s what this whole money saving business that I’ve been teaching you is all about! 😀 A peaceful stress-free life!  Wishing you a bright, stress-free, peaceful life of savings!   This strange lockdown we have found ourselves in and the resultant loss or decrease in income has left many people to ponder their financial situation and ways they have been managing their money up until this point. As I mentioned in the previous blogs, some people are just now waking up to the need for setting money aside for times such as this. The idea of the emergency fund has resurfaced into people’s consciousness, and the term is being batted around quite a bit of late. So I thought I would dedicate this space to the topic.  First of all, what is an emergency fund, and why do we need one? The general consensus is that we should have about 3-6-months-worth of living expenses put aside, that is there to be used strictly for emergencies only. This money is best kept in an online bank account (slightly better interest rate) and completely separate from your everyday checking/savings accounts. The exact amount in there is up to you. If your income is very variable or otherwise unstable, then the larger amount (6 months) would be advised. Some people prefer to have even more than 6-months-worth if their income is very unstable, or they are very risk averse, or prefer more of a cushion. Everyone, no matter how stable they think their income is, should have at least 3 months at the bare minimum, because no matter how good things are going for you right now, “s#@t” happens!  The purpose of having that fund is to keep your finances from being derailed when the unexpected happens. If you have that cushion put aside you can just dip in, pay that medical bill, or home repair or live on it through a job loss and get right back on track where you left off without throwing your whole finances into a tizzy. And even more importantly you won’t be forced to reach into your wallet for the credit card and put yourself into debt over the situation.  Someone posed the question to me recently: “How do I determine when to take money out of my emergency fund?.” An excellent question, and that is why I chose to address it in this month’s blog. The bottom line is this, the more you budget for the unexpected, the less you will ever have to dip into your emergency fund. It’s as simple as that. So how do you determine when you really do need to break that piggy bank?  Before dipping into the emergency fund you should ask yourself: “Do I really need to use this money right now?” Do you have some time to save up the money that you need, and get by without it for a while. Can you get by without whatever the expenditure is altogether? “Is this something I really need to buy?” Can you borrow something (at least while you save up)? Can you make do without it in some other way? “Is buying this thing right now really necessary?” Maybe it’s not the “need” you think it is, but more of a “want”. “Is this purchase right now really worth the sacrifice it will take to replenish my emergency account?” “If I don’t spend the money right now on this emergency will this situation cost me more money in the long run?” (i.e. a car or house repair that will get worse if left unfixed). In that case, by all means, do it.  And after you have dipped into your emergency fund consider if this expense is something you should be adding to your monthly budget so that you are prepared for this type of emergency in the future (I.e. beefing up your “car repair” or “home repair” fund, or adding a new category to cover whatever the expense was).  Ideally, if you have budgeted for every possible “unexpected” expense that may come your way, your emergency fund becomes just a big fat luxurious cushion for you to sit on and enjoy the security of. Wouldn’t that be a nice feeling!  Wishing you a bright secure future!

It’s May Flowers month, so I would like to take this month’s blog to look on the brighter side. We began this quarantine journey during the raw March winds when we too were raw and reeling from the shock of what was happening. Many people experienced a job loss or at least a reduction in pay. We could barely wrap our brains around what was happening. All we could do was retreat to our homes, as we were told to do, and try to make sense of it all.  We remained hunkered down through the rains of April, for the most part even unable to get outside much in the soggy world out there. As the temperatures plummeted out there so did our investments, and often our spirits. Things looked pretty bleak. All we could do was take stock of where we were financially and in every other way. For those of us who still had jobs it was just a matter of staying afloat and ignoring the stock market plunge (as we are always told to do), and stay the course. For those struggling with income loss it was a matter of prioritizing and taking care of the most pressing needs (shelter and food). The rest would have to be figured out eventually.  “But Victoria”, I can hear you saying now, “I thought this was going to be a silver linings message?” Ok, well now it’s May. The month of flowers. We are still home, but the initial shock has worn off a little. Those that have lost income have hopefully figured out a way to get their most important needs met. Maybe they are getting unemployment, SNAP benefits, food from a food bank, their stimulus check, or help from other sources. The rest of us are learning to live at home, creating new routines, keeping ourselves busy and occupied.  But the real May flowers are going to be what we take away for having gone through this. For many this time has given us somewhat of a wake-up call. We were hurrying along through life without even thinking about where all our money and time were going. This has given us time to pause, and think, and live a different way, whether we wanted to or not. Many are surprised to see how little they are spending now that they are forced to stay home, unable to go to restaurants, coffee shops, stores, bars, movies, concerts, etc., etc. Some never paid attention to how much all that was really costing them. And some are finding that they actually can lead a pretty good life without all that spending. Perhaps they will rethink it when life returns to normal. So that’s a silver lining. Forced savings helps you discover a different way.  Some people were caught short with no savings to help get them through a time of no income. It’s a hard lesson to learn for sure, but a lesson learned nonetheless. In either case being at home gives you the time to step back and examine the way you have been living, where your money has been going and to make some changes moving forward. What was once an abstract notion “I know I should be saving up for an emergency fund” becomes stark reality, and hopefully, brings about positive change for the future. A silver lining!  The silver linings go beyond all that though. As usual when we go through tough times, it brings out the goodness in people. Acts of kindness and generosity abound. It is heartwarming to hear the stories of people going above and beyond for their neighbors, friends and people they don’t even know.  And staying at home has given us a chance to live at a different pace, to stop all the rushing about and really spend time with each other in ways we rarely do when life is going full tilt. We have been playing board games, making meals and baking together, even just talking and going for long walks together. Some people have reconnected with old hobbies that they never had time for when life was in full swing. Knitting, gardening, painting, playing an instrument... All that is the best silver lining of all as far as I am concerned. If you know me at all, in person or from my writing, you know that I have long championed the slower, simpler, frugal lifestyle that has now become a forced reality for many.     I would like to think that some of this will stick, that at least some people will come away from all this with a new perspective. Priorities will shift. People will slow down just a little. Spend more time home with their families and less money on needless frivolities. I think that would be the biggest silver lining of all. A beautiful May flower indeed!   Now if only something would come along to force us to reduce our screen time… Wishing you all a bright and beautiful flowery future!    Have you been caught short with a sudden loss of income? Or even a reduction of income, at least temporarily? Times like this can turn your world upside down. Your priorities become putting food on the table and keeping a roof over your head. It’s hard to think beyond that and you may never have experienced anything like this before. It’s hard to believe but not so long ago, historically, this was how most people lived throughout most of their lives on a daily basis. In the 1800’s this was how many people struggled through life. They lived a very frugal existence without even thinking about it. It’s just what they had to do to survive, but then came industrialization and things began to change. People could feel more secure in their daily lives.  The Great Depression brought it all back. Food insecurity and the daily scramble just to survive. Frugal living was once again the norm. There have been a few more lean times, WW II, and a few lesser stock market downfalls that have shaken people’s financial worlds… but with no real lasting effect (on people's behavior), and now this...  Most people who came through the Great Depression tended to continue to feel that insecurity and lived the rest of their lives in a frugal manner. Their children were raised in that manner, and learned frugality to some extent. But now we have gotten too far away for it to have any real impact on the way we live now, and we all live a much richer lifestyle than those people of yore.  So, this coronavirus situation and the financial repercussions has really come as quite a shock, and is leaving many people at a loss as to how to proceed from here. It all depends on your own personal situation. If you still have a paycheck coming in, then the worst of it is psychological, the fear, and stress of dealing with our new upside down world. But if you can stay calm and just hunker down and get through this it will all be ok in the end. If you have investments you have obviously seen them drop, but don’t panic. Sit tight and they will rise again. That is just how the stock market works  If you have experienced loss of income and you don’t have an emergency fund, then just concentrate on your most pressing needs at the moment to get through this. You need a roof over your head (and the recent rent/mortgage freeze will take care of that for the time being) and you need food. If you really can’t afford even that then there are charities and agencies to help you with free food right now. And you can apply for food stamps as well (unemployment too). Beyond that don’t worry about your monthly bills. Contact your loan and credit card companies. They all know the situation and will hopefully defer them for now. The same for any medical bills you are paying. Luckily heat season is over, so that's one less thing to worry about. If you can’t pay your electric bill contact the company. Insurance companies must give you a grace period right now as per the CARE act. That takes care of your monthly bills for the time being.  When your stimulus check comes in, prioritize it for the best possible use. If you need it to live on, then put it in your checking account and use it for your most dire immediate needs. If you are not going to need the money for your current emergency situation, then it is a good idea to use it to pay down your debt and/or put it aside for an emergency fund if you don’t have one. Put this in a separate bank account that you don’t ordinarily access, such as setting up an account in an online bank.  And finally, now that you are stuck at home, if you never want to feel the bottom drop out from you again (financially), it is a good time to re-examine your spending habits. Take a good look at what you have been spending money on. Write down some savings goals. (Hint: one of them should be to save up an emergency fund.) Is your spending keeping you from your future goals? Are you robbing yourself of financial security and a decent future by giving in to reckless, unnecessary spending today? Do you ever want to find yourself in a scary financial situation like this again?  Now is the time, while you have the time, to think about what your priorities are and make a budget to reflect them. Now you have time together at home to discuss your goals and dreams for the future with your loved ones. This could be a turning point in your life. Make the most of a bad situation and turn it around to work for you. You can do it!  Wishing you all safety and good health! And a bright Future!   There is panic all around us. What should we be doing to keep ourselves and our loved ones safe? How long will this last? What supplies do we need? Do we have enough toilet paper? Sometimes we can be blindsided by what life throws at us. The best way to be prepared for the unexpected is to, well, be prepared.  In the case of a new disease coming your way, you are in a much better position to deal with it if you have been living a good healthy life up until that point, eating good fresh whole foods, getting proper rest and exercise, maintaining a healthy weight, etc.. If you have been living this way, chances are you have a much better immune system to fight off the infection. But if you have been eating a poor diet, are out of shape and overweight, leading to possible chronic conditions, can you suddenly start living a healthy lifestyle and expect to have the same healthy immunity as the infection invades your community?  Obviously you would have had to been building up that immunity and living a healthy lifestyle for quite some time for it to be effective for you now. I guess you are getting the idea of where this is leading to. The way we live our everyday financial lives also has a big impact on how well we are prepared for whatever life may throw our way.   Perhaps this coronavirus has directly (or even indirectly) affected your income. Are you financially prepared to weather the storm? Times like this bring home just how important it is to live below your means (when you have means) and constantly be putting money away for the lean times (or that big “lean time” in your future, otherwise known as retirement).  If your ordinary life includes having no debt, having a good emergency fund put aside, and saving on a regular basis, then you are much less likely to feel panic and upheaval when you come to a bump in the road. The more “padding” you have the less you will feel those bumps. Things that are a (financial) crisis to the ill prepared are merely blips to those that have the money to deal with them and move on.    If you see the sense in this and would like to shift from a living-on-the-edge (paycheck to paycheck) lifestyle there are many actions that you can begin to take to shift to a saving way of life. If you don’t know where to start I have many blogs on various aspects of money saving strategies that you can implement. Right now, while you are likely sequestered at home, might be the best time to finally sit down and take a good look at your financial situation and take control. Here are just a few that you might find particularly helpful: New Year Savings Resolutions Would You Love to Save More Money? Spring Clean Your Finances Strengthen Your Frugal Muscle, Lighten Your Stress Easy Peasy Savings, Make it Automatic Saving Money Every Day The Perks, Pluses, and Payoffs of Prioritizing My Message to Millennials Ready, Set, Goal! Money Saving Grocery tips from your “Auntie” Victoria And if you scroll through the rest of the blogs, you may find some more that apply to your particular situation and needs. If you need further individual help feel free to contact me at (845) 758-0250, or brightfuture2budgt4.gmail.com for a personal appointment.  Wishing you all the best for staying healthy now and moving toward a healthy financial future.

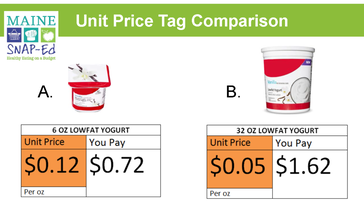

A while back when my niece was moving out on her own, I made this guide for her to help her save on grocery shopping. And now I thought it would be a good idea to share it with the rest of you. So just consider me your "Auntie" Victoria, as I present you with some of my sage tips on getting the most from your food shopping dollar.  #1 – Do not start with a menu list for the week! #2 – Look at the circulars every week, and make your list from the sale items (you have to know your prices, just because it says it’s “on sale” doesn’t mean it’s a good price). Learn your prices. You can keep a book/ list of them if you want to.   #3 – Then plan your meals for the week, based on what you have. #4 – Stock up on items when the sale is super good. #5 – Buy store brand / generic. It is almost always just as good (and, in fact, the same exact product) as the name brand. And you will pay much less.  #6 – Keep a running list of what you are getting low on (to replenish), and keep a well stocked pantry. This eliminates the need to go out shopping for a few needed items between (weekly) shopping trips. # 7 – Which brings us to: Shop only once a week! (In fact, some savvy shoppers shop only once every other week), This saves time, gas, and the temptation to impulse buy! #8 – Plan meals based on inexpensive ingredients! Rice, pasta, eggs, etc. Eat less expensive meat. Chicken, ground beef, stew meat, things like that. Eat meatless as much as possible, See my blog on how eating healthy (vegan) is cheaper. #9 – Don’t buy prepackaged food (i.e. boxed “mixes”, frozen “meals”) Make things from scratch. It's cheaper and healthier too! #10– Don’t buy things in single portion sizes. Portion out your individual size snacks yourself into baggies, little containers, etc. #11 – Use reusable containers as much as possible. Not “throwaways” (such as tin foil and plastic wrap,) Always ask yourself if a reusable container would do for this purpose. (Baggies can be washed out and reused, but even better to use an actual reusable container).  #12 – This goes for cleaning products too. Use rags instead of paper towels (you can wash them, and reuse).  #13 - Don’t buy bottled water! Tap water is fine. In fact most bottled water comes from a tap somewhere! If you are worried about your tap water, you can buy a filter for your tap, or a filtered pitcher for your fridge. Buy reusable water bottles to fill yourself when going out. If you absolutely must buy bottled water (which you don’t), buy the gallon size (of store brand), and fill your water bottles (or glasses) from that. This also saves the environment from all that plastic!  #14 – In fact don’t buy drinks! They are a super expensive, and unnecessary product, and usually just glorified sugar water. Not good for your budget or your health! Stick to water, or non-dairy milk drinks, or maybe orange juice (which you can buy from frozen concentrate, and make yourself). I know they sell “100% juice drinks”, but they are even more expensive, and even though it is “fruit” sugar, it is still just sugar. If you must buy juice (which you don’t), then at least water them down (a lot!) when you drink (serve) them. And don’t even get me started on soda!  #15 – Use the smallest amount of product necessary to get the job done. Experiment to to see what this would be (by using smaller and smaller amounts – or starting with a tiny amount, and working your way up. For instance, shampoo, conditioner, lotion, toothpaste, laundry detergent, dish soap, cleaning products, and also expensive ingredients in recipes (if you can’t eliminate them altogether). Make a game out of it. “Waste not want not!”  Does anybody even know what this expression means anymore? (#16– And now for the subject of coupons. I know you would think being frugal, I would be one of those crazy coupon ladies, but actually I’m not. The problem is they are mostly for expensive, prepackaged, processed junk food. And it is way too expensive (and unhealthy) to buy that crap anyway. If you do come across a coupon for something other than that (usually for health and beauty products), it is still usually cheaper to just buy the store brand. The only time it is usually worthwhile, is if the store is having a sale, and you have a coupon (especially if the store has a double coupon policy). But, of course you have to know your prices (what that item usually sells for, and if store brand is cheaper). #17– You also have to know your prices, when it comes to Bulk Buying. I often find that the prices on those giant bulk packages (i.e. Sam’s Club) are not better than you can get when that item goes on sale in the grocery store. So, if you are going to bulk buy, make sure you check the unit price (you should always be comparing unit prices anyway!) and know what it typically goes on sale for. And make sure you will be using that item up, before, say, 2 years past the expiration date or (if it is perishable) it turns into a science project. It’s not a bargain if you end up throwing half of it away.  #18 – Speaking of Expiration Dates, they are not that magical. The item is not made to self destruct, or go suddenly bad, on that very date on the packaging. And the companies give themselves plenty of leeway on that (better to be safe than sorry on their end) – it also keeps you buying more of their product as the one in your pantry “expires” and you have to replace it. Take them with a grain of salt (so to speak). I have eaten things long past the expiration date, and am still here to tell about it.  #19 – Don’t throw any food away!! Save even the tiniest amounts. You can use them for your lunch the next day, or incorporate them into dinner, or whatever. Learn to be creative with leftovers! #20 – Always start your dinner plans with “What has to be used up first?” (vegetables or meat “on their way out”, leftovers that have been in there a while, etc.). (Things in your pantry past the expiration date!). In other words: Don’t waste food!! You should never be throwing out food that you spent good money on!  #21– You can also take advantage of this concept at the supermarket. They will usually have a ‘bargain rack” of bread, etc., just at it’s expiration date, or fruits veggies that have to be used up in the next day or two, at very reduced prices. Take advantage of this. Buy them and use them right away.  Well I guess 21 tips are good to start with. LOL!! I could go on and on . . . . Not only with food shopping tips, but ways to save money on everything!! If you ever want help on budgeting to raise a family and “get by on less”, you know who to come to! Your “Auntie” Victoria, of course! Happy Saving!  Bonus tip! (Since you read all the way to the end)... If you really want to save money go Vegan! Meats and dairy are the most expensive items in your shopping cart. If you eliminate them from your diet you will save even more. It's cheaper AND healthier to eat this way. I did it! It's easier then you think! And you will feel great too!

It’s resolution time again! Want to lose weight? Get healthier? Will this be the year you buy that new car? Declutter the house? Ditch the spouse? So many possibilities! We always start each fresh new year with such high hopes and expectations. And often high on the list is finally getting those finances in order, paying off debt if you have it, and getting started on that savings plan. Then the year rolls along, and what goes wrong? Well, generally the optimum word here is plan. Do you have one? This quote says It all:  So whatever your financial goals are, you need to actually devise a strategy to achieve them. And you need to be as specific as possible. You first need to take stock of where you are. You can read about how to do that in my very first blog "New Year Savings Resolutions"  When you are writing your goals (and yes, you should be writing them down) you should be as specific as possible. No vague “wishes” here, but very concrete plans for what you are saving for, how much you need to save and when you want it saved by. With this down in black and white you can now devise a plan of action to achieve your goal(s). Here is an acronym that you can use to help you with this:  ."Specific: Exactly what are you saving for? (or what debt do you want to pay off? Measurable: Put a very specific dollar amount on your goal (i.e. I want to save $10,000 for a car by next fall). Achievable: Do not state goals that you cannot possibly reach. You will only frustrate yourself. But by the same token, you don’t want to make them so easy that you’re not really accomplishing anything (and still frittering most of your money away). Relevant: Is this an appropriate goal for you at this time, that you want to achieve? (Not saving for a house or a big wedding because everyone else is telling you it’s time.) (Not saving for a big boat when you have credit card or school loan debt to pay off.) Timely: Give your goal a deadline. "I want to save up a down payment for a house ($50,000) by spring of 2022." This way you can break it down as to how much you will need to save monthly to achieve this goal.  Once you have a firm grasp of your goals and how much you will need to save each month to attain them, you can do what you need to do to get there. The first thing you should do is make the savings automatic. Set up an online bank account and have the amount you have decided upon deposited into that account each month, right off the top. Out of sight, out of mind. It’s amazing how you can learn to live on a reduced amount when you never see the money in the first place.  If you need to pay off debts before you move on to savings, pay the minimums on all debts except one and throw as much as you can into the debt you are paying off. Once that one is paid off, move onto the next one. It will get easier and easier as you pay them off as you will have less minimums to pay as you knock off each one.  The other bonus of having these very specific, measurable, and methodical goals is that it makes it easier to sacrifice where you need to as you see your money going towards a higher priority. It feels good to forgo a few immediate pleasures for the sake of your future goals when you can watch your steady progress towards your own financial bright future!  |

Archives

June 2022

Categories

All

|

RSS Feed

RSS Feed