People say having kids is expensive and while they are definitely an expense, much of that expenditure can be trimmed up dramatically with a more frugal approach. There are certain times in the child rearing when spending can skyrocket if you are not careful (the holidays for example) and back to school is one of those times. First of all, it should not come as a big surprise that in September the little sweeties will be heading back to the classroom. Therefore, it should not come as a big surprise to your pocketbook. This is an event that should have been included in your budget all along. When I was using the envelope system (see February’s blog) I put in a few bucks (maybe $10) out of each paycheck into the “School Supplies” envelope so that I would be ready when the time came without having to break out the old credit card and go into debt for a perfectly expected event.  But the savings don’t end there. It is also in how and what you go about spending this school supply budget on. Obviously you will need supplies for the classroom. But take a good inventory first. How much can you reuse from last year? Does your child really need a new backpack this year, or might he be able to get by another year (or more) with this one? Take this approach with all supplies. Sometimes there are notebooks that only have a few pages written in. Rip out those pages and you have a brand new notebook for this year. And while it feels good to have that fresh pack of colored pencils at the beginning of the school year, does the old pack still have enough life in it for another year? Once you are sure that you are not buying “wants” for the new school year but actual needs, then it is time to replenish the supply. I am all for back to school sales. Know and watch your prices and comparison shop. Just because it is listed as part of a school sale does not mean the price is actually a bargain. If there is a really good price on something, (loose leaf paper for 17 cents a pack?) then by all means stock up on that item for the rest of the school year and even subsequent school years if there is no limit. And you do not have to give in to the desires of your children that just have to have that particular (insert popular character/name brand here) item. Remember there are other lessons to be taught to kids than the ones they learn at a classroom desk. And you as parents are obligated to teach them.  Now we move onto another category of possible contention. School clothes. And while it is nice and fun to start off the new year with a whole new wardrobe it is not necessarily necessary! Once again take careful stock of actual needs. And once again refrain from giving in to entitled demands. Another point in question, is do these “new” clothes actually have to be new? I shopped for much of my kids clothing needs at thrift shops and yard sales and back to school was no exception. And I can guarantee you that no one could look at my kids’ wardrobes and tell me which items were purchased new and which were “preworn”.   As the kids got a little older and more aware of their “wants”, I would let them make the choice. I would give them each an envelope with a certain amount of money in it for school clothes and off we would go shopping. It was entirely up to them as to whether they wanted to buy a nice “new” wardrobe with that money for a few bucks an item at the thrift shops or whether they wanted to take that same amount of money and just buy a few name brand (or whatever) new items at the stores, or shop a combination of the two. Of course, remember you are still their parent and retain final say on what is appropriate to buy and wear with “their” money, and what items they need to buy (socks and underwear might not be on the #1 “gotta have it” list, but a necessary expenditure never the less). And another non-classroom lesson learned here . . . budgeting their money!  There are also year-long school related expenses to consider, like school lunches. Consider your budget here as well. Is it cheaper for them to bring their own lunch? (hint: Almost always) (another hint: This goes for adults as well). And although the grocery stores are blasting you with back-to-school lunch items at this time of the year, these are usually not the best things for your lunch budget. For instance, do not be tempted by those cute little single serve packs of anything. Buy your own (pretzels, dried fruit, crackers, cookies, cheese, etc. etc.) and prepackage it yourself into Ziploc bags or even better reusable containers (P.S. aside here, I reuse Ziploc bags too). Have the kids participate in the preparing of their school lunches, making as much of it themselves as possible. The more they are involved in the prep the more they will be likely to actually eat it (and bonus, another life skill lesson learned!). I always told my kids to bring home what they didn’t eat rather than throw it away in the garbage. It drives me crazy how much perfectly good food gets thrown into school lunchroom (and all) garbage cans. If they bring it home, they can eat it as part of their after school snack or take it again the next day.  So, I hope you can see that sending the little ones (and not so little ones) back to school does not have to be quite the piggy bank shattering event that it can become if you are not careful. Stretch your frugal muscle and save your dollars. Your piggy bank will thank you for many years to come. And who knows, maybe even your kids will thank you someday for all the (out of school) lessons learned. 😉

0 Comments

Here’s the biggest mistake almost all people make when it comes to savings: They pay their bills, buy their food, make repairs, buy things for the house, pay for kid’s activities, go shopping for clothes, go to the movies, go out to eat, go shopping for some new clothes, etc., etc., and then save what’s left over at the end of the month. Can you see the problem with this? Is there ever anything left at the end of the month?? Many people will also say that they live paycheck to paycheck, but here is the interesting thing about this; They are saying this no matter what the size of their paycheck. The person who makes $300/wk. is saying it and so is the person who makes $600/wk. and the one who makes $3,000/wk. and on up. Right up to that athlete or rock star who is making several million dollars a year and blowing it all, only to go bankrupt when the income dries up. It seems to be just human nature to live just up to your income level whatever that may be, or even a little above that (accounting for all the debt people tend to find themselves in). But if you want to save money the only way you can do it is by living below your means, whatever they may be. Another way to put this is: You don’t save money by how much you make, but by how much you don’t spend. The great investment “guru” Warren Buffet puts it this way:  This is great advice, but how do you do it? Well the great US of A knows how. You pay taxes every year, right? Does Uncle Sam just let you have your full pay and then ask you to cough up the taxes on April 15th? You bet your sweet bippy he doesn’t, because he knows what would happen. People adjust their lifestyle to however much money is coming in. So he just takes his cut up front and people adjust to living on what’s left. Well you can do the same thing for yourself. Just take it off the top. The U.S. government even gave people a means to do just that by starting the 401K program, giving you a tax advantage and a way for you to save money by skimming it right off your paycheck without even ever seeing the money. If you have this offered at your place of employment you should certainly be taking advantage of it. Some generous companies will even match your contribution dollar for dollar up to a certain amount. Free money! Never pass up this opportunity! But even if you don’t have the opportunity for a 401K (or 403B, TSP, etc.), you can still make the magic of automatic savings work for you. All you have to do is set it up once for yourself and done. Savings skimmed right off the top. Out of sight, out of mind. You will quickly adjust to living on what remains. How you set this up depends on what you are saving for. Your first savings goal should be your retirement. I know this sounds kind of backward or counterintuitive, but because you need such a large amount, and because it makes such a difference when you start compounding that interest early, it is imperative that you start this ASAP! If you don’t have a 401K then you can set up your own retirement account in a Roth IRA. I recommend you do this by opening up a discount brokerage account at a firm such as Fidelity or Vanguard. This gives you many options on what to invest your money in inside of your Roth IRA and gives you complete control over it. Once you have your Roth set up it is quite simple to set up automatic payments of whatever amount you choose monthly going from your checking account into your IRA. Whether you have a 401K in the workplace or your own Roth IRA, you can also set up similar automatic payments going into (online) savings accounts for your other savings goals (wedding, car, house down payment, education, etc.) Once you have your savings goals set up automatically in this way, you no longer have to stress about money. You are all set for your future needs both short and long-term, and you can spend what’s left freely. Won’t that be a nice feeling!   Did you spring clean your finances? Were you able to take a good look at your expenditures and trim some of the fat out of your monthly expenses? If you have done this successfully, I bet you are feeling pretty light right now. In fact, you are probably walking around with a spring in your step! It’s amazing how good lightening up your budget can make you feel! Before people start on this process they actually tend to think that putting themselves on a tighter budget will make them feel weighed down and restricted, but once they get started they realize that it actually has quite the opposite effect. And once you have pushed past those first steps, you will find not only does it feel surprisingly good, but it gets easier. And not only does it get easier, but you get better at it. That frugal muscle begins to awaken and gain strength. And, by golly, not only is saving money not a chore, but it begins to become fun! You will start to examine each expenditure in a new light. You will find yourself looking for more ways to save. How can you cut back even further? Once you come out of that fog or never-ending consumerism your brain chemistry will begin to change. You will no longer take your satisfaction from acquiring more and more stuff and making all those daily instant pleasure purchases, but rather in the feeling of pride and contentment that you are living a full life without needing to spend money like that. As you gain control over your finances, get out from under that heavy debt, and begin to see your savings grow, you will delight in the peace of mind that your new frugal lifestyle has brought you. “Stuff” is no match for this joyful feeling of gratification. This will strengthen your resolve to save even more. Once you get the “snowball” going in the right direction there’s no stopping you! Who wants to go back to being buried under that avalanche of debt and stress.? You are free! Now you will stop and think about each purchase with what I call the Super Sliding Scale of Savings. It goes something like this:

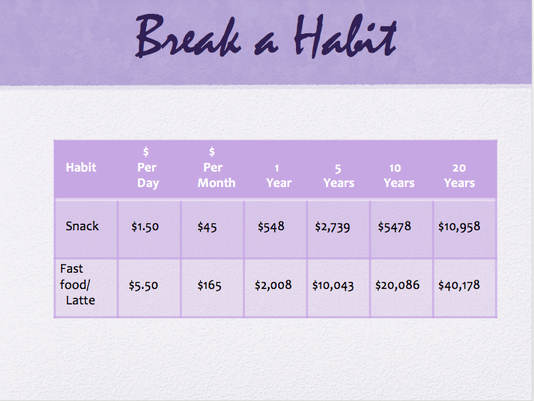

The more times you can make it all the way to step 6, the better off you will be and the happier and more content you will become. So keep on flexing that frugal muscle! You will continue to grow stronger financially and lighter in your outlook and step. Here’s to financial fitness!   In January and February, we talked about getting organized with your expenses and setting some financial goals for yourself. I discussed the importance of keeping track of your expenses and setting up a monthly budget. Hopefully, you are now getting a better idea of where your money is going and are starting to feel more on top of your financial life. Perhaps this has lead you to make some changes in what you are spending your money on and how much is going out each month. If that is the case, good for you, you are on your way!  Now that winter is over and you are feeling more energetic and ready to give your house a good cleaning and get out there and clean up your yard to make way for the beautiful spring growth and flowers, you can also do some spring cleaning of your finances. Just as you declutter your house of unwanted extra stuff for a more peaceful environment and clean up all that yard debris for a tidier look, you can also take a look at your finances to clear out those unnecessary expenses that are keeping you from reaching your savings goals and from the peace of mind of living below your means. Once you are organized and are keeping track of your expenses, then you can begin to go over them with a fine tooth comb and start eliminating the financial clutter. Simplify your spending! There are probably at least a few things that you have gotten into the habit of buying that you can do without. And there are probably a few things that you are spending more money on than is necessary. How quickly or gradually you go about this financial downsizing is entirely up to you. Maybe you are the type that likes to get used to things slowly, and form new habits one at a time before making the next change, or maybe you like to see the rapid results of all that “found” money you can have (to pay off debts or start saving money more quickly) when you really pare down your budget all at once. Proceed at your own style and pace. Eliminating a few (or more than a few) daily or weekly expenses can really add up to big savings. Here are a few examples of how small savings can add up:  But don’t overlook those big (typically monthly) expenses too. Take a look at your phone plan, your utility usage and company, TV and internet providers, car/homeowners insurance. Shop around to see if you can get a better deal. Sometimes all it takes is the threat of moving on to spur your present company to offer you a sweeter deal. Even think about your mortgage or rent payments. Can you downsize? Refinance? Get a roommate? Once you eliminate a lot of that spending clutter your psyche will feel lighter, and your wallet and bank account will now be able to grow and thrive like those beautiful spring flowers. It’s a good deal all around. Give it a try!   If you are of a normal weight like I am, people will sometimes say to you “Oh, you are so lucky you don’t have to worry about your weight.” Or even more erroneously, “You are so lucky you can eat whatever you want.” Neither of these statements can be further from the truth. In fact, the only reason I am a normal weight is because I do worry about my weight, every day. And I do watch what I eat, every meal. It is just as much a struggle for me as for them. In fact, probably more so, given the fact that I am only 4’10” making every calorie count!

So what does that have to do with money, you ask? Well, I have also had people say to me, "Oh you are lucky that you were able to stay home with your kids and did not have to go out and work." And once again, luck had very little to do with it. Many of the women who said this to me had husbands who were making more money than mine did. These women also had cable TV, big new SUV’s or minivans, new clothes and shoes, maybe a Coach bag, and (back in the day when I had dial-up) high-speed internet. I would wager a bet that they also thought nothing of going out to lunch, buying coffee and drinks out, getting their nails and hair done, and picking up take-out for dinner. And yes, before you start yelling at me, I know there are single moms or other circumstances when women need to work, but my point is that often what people perceive as luck may actually be a result of the many choices made every day in life. Luck can also be a matter of perception in another way. Let’s say you get in a car accident and break your arm. Are you lucky or unlucky? Well, some might say of course you are unlucky! You got into a car accident and broke your arm for goodness sake! How can that be lucky? But then there is the person who says, “I am so lucky that all I got was a broken arm! I am still alive!!” Same scenario. Completely different perspective. So what is luck then? It is a matter of the results of your actions, and a matter of perception. So, the question is can you create your own “luck”? You absolutely can! Let me create a little story for you to illustrate my point even further: Let’s say Dick and Jane make the exact same amount of money. OK, scratch that, since Dick probably makes more. Let’s say Dixie and Jane make the exact same amount of money and through some cosmic fate have the exact same bills and expenditures every month. Each is able to save up exactly $100 per month after everything is paid, giving them each an extra $1,200 per year. At the end of Year One, Dixie takes that money and goes on a much-deserved vacation. Jane puts it in a one-year CD. At the end of Year Two, Dixie needs some new living room furniture, so she spends her $1,000 on that plus $200 on a hot new outfit. Jane now has $2,424 (her yearly savings of $1,200 plus $1,242 in her CD). She puts $2,200 of it into another CD, and spends $30 on a water filter for her tap, so she can stop buying bottled water, and spends $70 on an indoor antenna for her TV and cancels her $110 per month cable service. With the remaining $124 she has a great time at the thrift shop buying a new wardrobe for the coming year. Year Three: Dixie has her usual $1,200 at the end of the year. She splurges on buying herself the latest iPhone, which is just out, plus a nice case for it. Jane now has $2,244 from her CD, plus $350 saved by not buying bottled water, plus $1,320 saved by not paying for cable every month, plus her usual $1,200 for the year. A total of $5144. She spends $800 buying a washer and dryer so that she can stop going to the laundromat. She decides to invest the remaining $4,344 into a low-cost index mutual fund. At the end of Year Four, Dixie has her usual $1,200. Jane has her usual $1,200 plus $350 saved on water, plus $1320 saved on cable, plus $180 saved on laundry. And her mutual fund did pretty well to earn her 8%, so she now has $4,691 in that for a total of $7,741 … I could go on and on, but I hope you are starting to get the picture. One night Dixie meets Jane at a party. When the topic turns to finances, Jane happens to mention that she currently has about $3,000 in her savings account plus a mutual fund with over $4,500. Dixie is impressed and amazed and comments on how “lucky” Jane is to be so far ahead of her, while she, herself struggles living paycheck to paycheck. Does this sound familiar? Is Jane “lucky”? So how about starting to turn your own “luck” around. And one day in the future maybe you will chuckle inwardly when someone at a party tells you how lucky you are to have such a nice healthy nest-egg for your retirement and a nice bright future to look forward to.  Welcome back! I hope you have been working diligently at paying attention and keeping a record of your daily expenses. Have you had any surprises? Were there things that you found yourself spending money on that you never even gave a thought to? It’s all these little dribs and drabs of money sifting through your fingers that add up. It doesn’t seem like a lot when you are buying one little thing at a time, but when you tally it all up at the end of the month and multiply that by 12 for what you are spending on all these frivolities per year .... Yikes! In this day and age, it is often not actual money that we are parting with. Most people today have become even one more step removed from their spending awareness. Just pull a little piece of plastic out of your wallet, plunk it down and, voila, you have whatever you want. It barely seems that you’ve “lost” a thing. It’s just so easy to be unaware of how much is going out. This first step in stemming the constant flow of too much money going out is to become mindful of your daily spending habits and just where your money is going. If you have done your “homework” from my January blog, then you now have a better idea of that. The next step is to write yourself a budget. This is where you can begin to trim some of that fat. Do you really want to keep spending all that money or are there some things you can forgo in the interest of saving money? Once you have a clear picture of where your money is going and how much you no longer want to spend (aka waste), you can allocate a certain amount to each line item of spending every month. Now you will have an accurate outline in black and white of where your money is going (and where you don’t want it to go!) Here is a budget form that I created to help you plug your expenses into as many categories as I could think of. I have also left some spaces for those that you may have that I haven’t come up with. Now I would like to introduce you to an old timey but timeless way to keep your spending in line and on budget each month. It is based on going back to using good old American cash money for your daily expenses. This is what I did throughout most of my years of raising my family. I did not know it at the time, but since the magic of the internet I have learned that other people do this too and they call it quite simply and accurately “The Envelope System.” It is very inexpensive to get started and implement as all you will need is a $1 box of plain white envelopes. Then you simply divide your budget into spending categories and label the envelopes accordingly (e.g. food, gas, clothes, entertainment, health and beauty, household needs, etc.), and place the amount of money that you have allocated for the month into the appropriate envelopes. This gives you a great visualization of how you are doing. You can actually see how much money you have left to last you until the end of the month. When the money is gone it’s gone. No more spending for the month. Can you “cheat” and take money from another envelope if one of them is empty too soon? Sure! But just who are you cheating? Yourself, of course! And, if you want to stay on budget, now you have less to spend in the category of the envelope you “stole” the money from. You will get better at knowing how much to put in each envelope for the month as you become more practiced at it. And hopefully you will also get better at finding ways you can save more money in each category too! As I continue these blogs I will delve more deeply into just how to find those ways of saving more money in each of those categories. You can also attend my monthly meetings at the Red Hook Community Center for more tips and tricks on saving money through the magic of frugal living. (See the Events and Classes page). So until we meet back here next month, I bid you adieu and happy savings! |

Archives

June 2022

Categories

All

|

RSS Feed

RSS Feed